10 Key Commercial Bridge Loan Terms Every Investor Must Know

A giant financial wall is coming. Right now, a massive $875 billion in commercial mortgages is set to mature this year. It is a terrifying number. Banks are closing their vaults. They are saying no to good borrowers. If you own commercial property, your time is running out. You might be facing a sudden default. Finding the right commercial bridge loan terms is no longer just a financial choice. It is a survival skill.

Imagine Marcus. Marcus spent ten years building his real estate dream. He owns a beautiful mixed-use property in Dallas. It has apartments on top and retail shops on the bottom. A few months ago, his main retail tenant moved out. His cash flow dropped.

His local bank did not care about his past success. His loan was coming due. The bank officer gave him a cold look and said, "We cannot refinance you." Marcus felt a cold sweat. He had fourteen days to pay back $2 million. If he failed, the bank would take his building. He was about to lose everything.

Then, Marcus found Commercial Lending USA. They are a national correspondent and table-lender. They have thirty years of underwriting skills. They did not judge his temporary empty space. Instead, they looked at the future of his property. They helped Marcus find a temporary financial bridge.

This is the power of a bridge loan. It saves your deals when traditional banks run away. Let us learn how these loans work so you can protect your wealth.

Why Is Everyone Talking About Commercial Real Estate Bridge Financing Trends 2026?

The market is shifting fast. You must look at the latest commercial real estate bridge financing trends for 2026 to understand your options. Private lending is growing rapidly. The Mortgage Bankers Association predicts that commercial mortgage lending will jump to $805.5 billion this year. That is a huge 27% increase from last year.

Why is this happening? It is because banks are terrified of the economic outlook. The impact of the economic forecast on commercial bridge loans in 2026 is very clear. Inflation is staying high. The Federal Reserve kept its main interest rate at 3.50% to 3.75%. This means long-term interest rates are staying elevated.

Harvard economics professor Kenneth Rogoff's warnings are coming true. He says cheap bank loans have been gone for a long time. Many properties have loans that were written when rates were very low. Now, those loans are maturing. Borrowers cannot get new bank loans because their properties do not have cash flow at today's high rates.

Private bridge loans are stepping in to fill this gap. Investors are using them to buy time. They use the money to fix their buildings, find new tenants, and refinance later when rates drop.

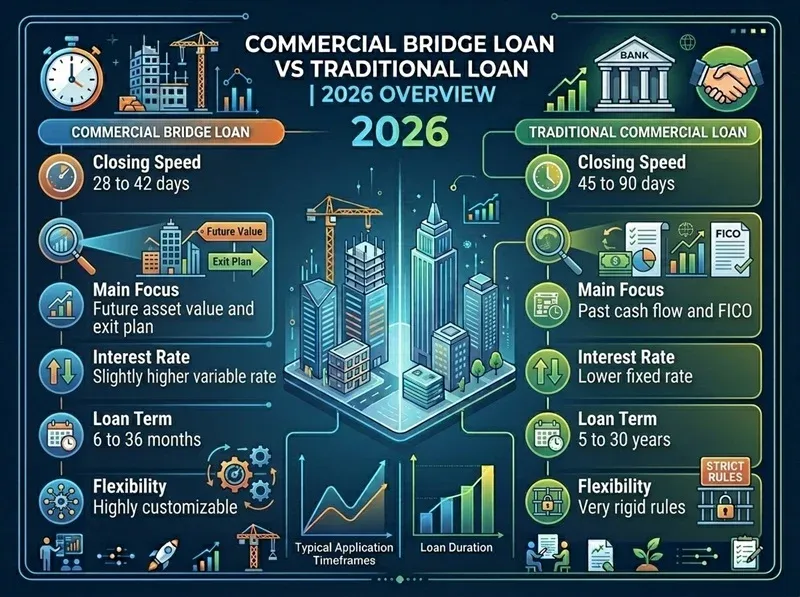

Commercial Bridge Loan vs Traditional Loan 2026: Which Is Best for Your Deal?

You need to know the difference between your options. The commercial bridge loan vs. traditional loan 2026 matchup is about speed versus cost.

Traditional bank loans are slow. They require piles of paperwork. They want to see two years of perfect tax returns and stable cash flow. If your building has vacant spaces, a bank will say no.

A bridge loan is different. It is an asset-backed loan. Lenders focus on the property value and your exit plan. They can fund your deal in days.

Feature | Bridge Loans | Traditional Loans |

Closing Speed | 28 to 42 days | 45 to 90 days |

Main Focus | Future asset value and exit plan | Past cash flow and FICO |

Interest Rate | Slightly higher variable rate | Lower fixed rate |

Loan Term | 6 to 36 months | 5 to 30 years |

Flexibility | Highly customizable | Very rigid rules |

Marcus realized he could not wait ninety days for a traditional bank. He would lose his property before the bank even finished reading his tax returns. He chose a bridge loan because he needed speed.

What Are the True Commercial Bridge Loan Terms?

To use these loans, you must understand how they are built. If you ask what the typical commercial bridge loan terms are in 2026, the answer is simple. They are short-term safety nets. They typically last between twelve and thirty-six months.

These loans are made for properties going through a change. This is called a value-add strategy. You buy a property that has physical or financial problems. You invest money to fix it up.

This initial active period is the value-add phase. During this time, you raise the net operating income. Let us write down the formula for net operating income:

NOI = {Gross Operating Income} - {Operating Expenses}

By raising net operating income, you force the property value to increase. You calculate the property value using the cap rate:

Property Value = {{NOI}/{Cap Rate}}

Once the renovations are finished and new tenants are paying rent, the property enters the stabilization phase. Now, the property is safe and predictable. This is when you pay off the bridge loan with a permanent loan.

Can You Meet the Short-Term Commercial Bridge Loan Requirements 2026?

Qualifying for a bridge loan is much easier than qualifying for bank debt. The short-term commercial bridge loan requirements for 2026 focus on your asset.

Here is what you need to show your lender:

- A Real Appraisal: An independent appraiser must visit your property. They will check its current value and its future value after renovations.

- A CapEx Plan: This is your construction budget. You must show exactly how much money you will spend on repairs and upgrades.

- Your Track Record: Lenders want to see that you have done this before. If you are new, you can partner with an experienced team.

- A Clear Exit Plan: This is the most important part. You must show exactly how you will pay back the loan. Will you sell the property? Will you refinance with a bank?

Lenders are comfortable with high vacancy rates because they know you will fix the property. They focus on what the property will become.

The Decisive Playbook: 10 Key Terms Every Investor Must Master

To protect your equity, you must master these ten key terms. They are the building blocks of your loan.

1. Cost of Capital: Commercial Bridge Loan Interest Rates 2026

The interest rate is your main cost. Today, commercial bridge loan interest rates in 2026 typically range from 5.75% to 12.75%. If you use private hard-money lenders, your rate could be 15% or higher.

Choosing Your Path: Fixed vs Adjustable Commercial Bridge Loan Rates 2026

You must choose between fixed and adjustable rates for commercial bridge loans in 2026.

Adjustable rates are tied to short-term indexes. If the Federal Reserve cuts rates, your monthly payment will drop.

Fixed rates stay the same. This gives you peace of mind. Marcus chose a fixed rate because he did not want any surprises while renovating his building.

2. Loan-to-Value (LTV) and Loan-to-Cost (LTC) Dynamics

Lenders use LTV and LTC to decide how much money they will give you.

The loan-to-value ratio compares your loan amount to the appraised value of the property:

LTV = {{Loan Amount}\{Appraised Value}} * 100

Most bridge lenders will fund up to 80% LTV.

The loan-to-cost ratio compares your loan to the total cost of buying and fixing the property:

LTC = {{Loan Amount}/{Total Project Cost}}* 100

Lenders want you to put your own money into the deal. This is called having "skin in the game." It makes you less likely to walk away if things get tough.

3. Structural Commitments: Commercial Bridge Loan Repayment Schedule 2026

Your monthly payments differ from those of a normal home mortgage. The commercial bridge loan repayment schedule 2026 does not include principal amortization. You do not pay down the loan balance each month.

Instead, you make interest-only payments. You calculate your interest payment like this:

Monthly Interest = {{Loan Amount}*{Annual Rate}}?{12}}

At the very end of the loan, you must pay back the entire principal balance in one large balloon payment. This interest-only structure keeps your monthly payments low. It allows you to spend your cash on fixing the property.

4. Protecting Cash Flow: Understanding Commercial Bridge Loan Covenants 2026

Covenants are rules you must follow during the loan. If you violate a covenant, the lender can call the loan due. Understanding commercial bridge loan covenants in 2026 is vital.

A common rule is the Debt Service Coverage Ratio:

DSCR = {{NOI}/{Annual Debt Service}}

If your DSCR drops too low, you are in default.

To protect themselves, many bridge lenders use a debt yield covenant instead:

Debt Yield = {{NOI}/{Total Loan Amount}} *100

A Yale University study shows how fast these risks can appear. Researchers Cameron LaPoint and his team looked at what happened when the Department of Government Efficiency canceled federal office leases.

Properties lost 5.6% of their net operating income overnight. This caused their DSCR ratios to drop. Covenant violations spiked. This proves that even stable government tenants can carry unexpected risks.

5. Upfront Frictional Drag: Commercial Bridge Loan Closing Costs 2026

You must prepare for upfront fees. The commercial bridge loan closing costs in 2026 typically range from 1.5% to 3% of the total loan amount.

Cost Item | Typical Percentage or Fee |

Origination Fee | 1.0% to 3.0% of the loan |

Independent Appraisal | $3,000 to $7,500 |

Title and Escrow Fees | Varies by transaction size |

Extension Fees | 0.25% to 1.00% |

These friction costs impact your bottom line. Since bridge loans are short-term, these fees raise the overall cost of capital. You must budget for them carefully.

6. The Ultimate Resolution: Commercial Bridge Loan Exit Strategies 2026

A bridge loan is a temporary path. You must have a clear map to get off it. Your 2026 commercial bridge loan exit strategies are your way out.

The most common exit strategies are:

- Permanent Refinance: You transition to a long-term loan. This could be an agency loan from Fannie Mae or Freddie Mac. It could also be an SBA loan or CMBS loan.

- Property Sale: You sell the fixed-up building to a long-term buyer. The sale proceeds pay off the bridge lender.

- Portfolio Aggregation: You bundle several properties together and refinance them under one large loan.

7. Extension Rights and Rollover Provisions

What if your construction takes longer than you planned? What if a city permit is delayed? You will need more time.

Extension provisions allow you to extend the loan term. Most lenders will grant a six-month extension if you pay an extension fee and show that you are making progress. This keeps your project alive.

8. Recourse Carve-outs and Non-Recourse Protections

Many commercial bridge loans are non-recourse. This is a massive benefit. It means the lender cannot seize your personal home, your bank accounts, or your cars if you default. They can only take the property itself.

But there are exceptions called "bad-boy" carve-outs. If you commit fraud, steal insurance money, or file a fake bankruptcy, the loan becomes recourse. Your personal assets will be at risk. Always play by the rules.

9. Interest Reserves and Construction Draw Hurdles

Lenders want to make sure your monthly payments are made on time. To do this, they often set up an interest reserve. They hold back a portion of your loan proceeds to pay your monthly interest.

They also withhold your construction funds. They release this cash in draws as you finish specific repair steps. An inspector will visit the property to verify the work before each draw is paid.

10. The Referral Catalyst: Exclusive and Non-Exclusive Realtor Programs

Brokers and realtors are the lifeblood of the commercial real estate world. Commercial Lending USA rewards these partners. They offer both exclusive and non-exclusive referral programs.

- Exclusive Programs: Best for dedicated partners who want top-tier commissions and structured deal support.

- Non-Exclusive Programs: Perfect for independent brokers who want to keep their options open while getting fast funding for their clients.

These programs help brokers find the perfect cash solution for their clients. It keeps deals moving forward.

Adaptation Guide: Tailoring Bridge Financing to Your Project Type

Different properties need different loan structures. A self-storage building does not work the same way as an apartment complex.

Property Type | Typical LTC | Key Project Risk | Core Structural Feature |

Multifamily | Up to 85% | Lease-up speed | Interest reserve with agency exit plans |

Self-Storage | Up to 75% | Local competition | Draw schedules based on units finished. |

Assisted Living | Up to 80% | State licensing speed | Longer interest reserve pools |

Mixed-Use | Up to 75% | Retail tenant turnover | Debt yield covenants |

Construction | Up to 75% | Cost overruns | Direct builder draw monitoring |

Commercial Lending USA understands these differences. They work on ground-up construction, fix-and-flip, and fix-and-rent deals. They know how to tailor the loan terms to your specific project.

Do You Know How to Qualify for a Commercial Bridge Loan in 2026?

Let us walk through the steps. Knowing how to qualify for a commercial bridge loan in 2026 will save you weeks of stress.

Here is how the process works:

Prepare Property Info ──> Consult with Experts ──> [Appraisal & Underwriting] ──> Quick Closing

First, you gather your property info. This includes your lease roll, your tax bills, and your renovation plans.

Second, you consult with the team at Commercial Lending USA. They offer seventy-five loan options. They do not do direct underwriting, but they have thirty years of underwriting abilities. They will structure your deal to make sure lenders love it.

Next, the team guides you through the process of applying for a commercial bridge loan in 2026. They order the appraisal and review your business plan. Finally, the loan closes. The cash is sent to your escrow account, and you can start construction.

What Are the Real Pros and Cons of Commercial Bridge Loans 2026?

You must weigh both sides before signing. The pros and cons of commercial bridge loans in 2026 are clear.

The Good

- Insane Speed: You can get cash in 5 to 14 days. This lets you win competitive deals.

- Total Flexibility: Underwriters look at future value, not past history.

- Personal Protection: Most options are non-recourse. Your family wealth is safe.

- Renovation Cash: The loan provides the cash you need to add real value.

The Bad

- Higher Rates: The interest rate is higher than that of a long-term bank mortgage.

- High Fees: Upfront fees can add up quickly.

- Maturity Clock: You must move fast to finish your repairs before the balloon payment is due.

Market Leadership: Selecting the Best Commercial Bridge Loan Lenders 2026

Do not work with just anyone. Finding the best commercial bridge loan lenders in 2026 requires careful checking.

Some lenders sell their loans to secondary buyers right after closing. This can cause your terms to change unexpectedly. You want to work with a direct correspondent and table lender.

Commercial Lending USA stands by your side. They act as a super broker when needed. They guide you through the process, protect your interests, and help you transition to permanent debt when the bridge term ends.

Securing Your Real Estate Future

Marcus got his bridge loan through Commercial Lending USA. The cash arrived in ten days. He hired contractors, renovated his retail space, and signed a new national anchor tenant.

His net operating income jumped. A year later, he refinanced his bridge debt into a beautiful, low-rate permanent loan. He did not lose his equity. He saved his building and grew his wealth.

Do not let the maturity wall destroy your portfolio. Partner with an experienced team. Securing the right commercial bridge loan terms is how you survive and win in today's market. Contact Commercial Lending USA today to build your financial runway.

FAQs

Can you get a bridge loan with bad credit?

Yes. Private lenders focus more on your property value than your personal credit score. But you must prove a clear exit strategy. A solid plan shows how you will pay off the loan when it matures.

Can I buy auction properties with a bridge loan?

Yes. You can use these short-term loans to secure auction deals quickly. But the auction rules must allow for escrow accounts. You also need to make sure you can easily obtain standard property title insurance.

Can you get two bridge loans at once?

Yes. You can secure a loan against your current property to raise the down payment. Then, you can take a second loan against the new commercial property. This double strategy works well for fast property purchases.

Can new startups qualify for bridge loans?

Yes. Startups can qualify if they have valuable real estate to pledge as collateral. Private lenders focus on the physical asset's value. This is different from banks that require years of profitable business tax returns.

Do commercial bridge loans trigger specific taxes?

No. The loan itself is not taxed as income. But if you use the funds to flip a property for profit, your capital gains may be taxed. Always consult a certified accountant to check your local rules.

0 Comments

Leave A Comment