-1779383399.webp)

Fannie Mae Loan 2026: Complete Guide to Rates, Requirements & Multifamily Financing

Fannie Mae loans (also known as agency loans or FNMA loans) are one of the most powerful financing tools for commercial real estate investors and multifamily property owners in 2026. Backed by Fannie Mae’s secondary market liquidity, these loans deliver low rates, long amortizations, non-recourse options, and high loan-to-value (LTV) ratios that beat most bank and SBA alternatives.

At Commercial Lending USA, we close Fannie Mae / Freddie Mac loans every week for apartment buildings, senior housing, student housing, and mixed-use properties. This definitive 2026 guide breaks down everything you need to know, including rates, eligibility, documentation, pros/cons, and exactly when a Fannie Mae loan beats every other option on the market.

What Is a Fannie Mae Loan?

_1779384523.webp)

Fannie Mae (Federal National Mortgage Association) does not lend money directly to borrowers. Instead, it buys qualifying commercial and multifamily mortgages from approved lenders like Commercial Lending USA, packages them into mortgage-backed securities, and sells them to investors. This massive liquidity allows us to offer the following:

- Fixed rates as low as 5.5–6.5% (as of May 2026)

- Terms up to 30 years

- Amortization up to 30 years

- LTV up to 70–80% (per our current product summary)

- Non-recourse financing with standard “bad boy” carve-outs

These loans are ideal for stabilized multifamily properties (5+ units) with strong cash flow.

Fannie Mae Loan vs Freddie Mac Loan – Quick Comparison

Feature | Fannie Mae Loan | Freddie Mac Loan | Winner for Most Investors |

Max LTV | Up to 70–80% | Up to 75–80% | Tie |

Min DSCR | 1.25x+ | 1.25x+ | Tie |

Rate Range (2026) | 5.5–6.5% | 5.5–6.5% | Tie |

Property Types | Broader (Seniors, Student, MHC) | Strong on conventional multifamily | Fannie Mae |

Prepayment Flexibility | Excellent | Slightly more flexible | |

Closing Speed | 30–45 days | 30–45 days | Tie |

Bottom line: Most borrowers qualify for both. We shop both agencies simultaneously to get you the best execution.

Current Fannie Mae Loan Terms & Requirements (2026)

From our latest Loan Products and Terms Summary (updated May 2026):

Loan Program | Interest Rate Range | LTV (Max) | LTC % | ARV | Down Payment (Min) | Loan Term | Credit Score (Min) | Bank Statement | Tax Return |

Fannie Mae / Freddie Mac | 5.5–6.5% | Up to 70% | 70% | 65% | 25% | Up to 30 years | 680+ | Required | Yes |

Additional Fannie Mae Multifamily Guidelines (2026):

- Minimum property size: 5+ units (or 50+ pads for manufactured housing communities)

- Stabilized occupancy: Typically 90% for 90 days prior to funding

- Minimum DSCR: 1.25x (conventional properties)

- Recourse: Non-recourse available

- Property types: Conventional multifamily, affordable housing, seniors housing, student housing, manufactured housing communities

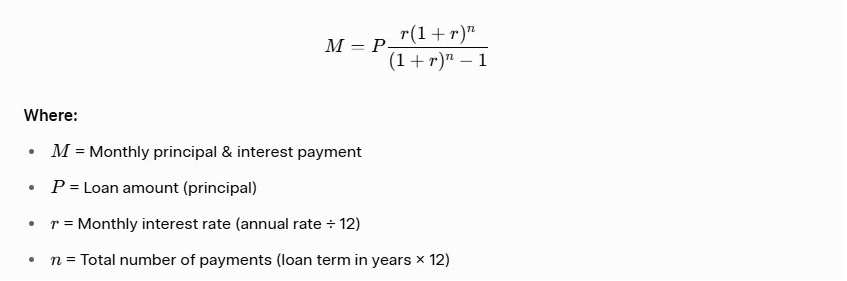

Fannie Mae Mortgage Calculator 2026

_1779384625.webp)

Want a Fannie Mae mortgage calculator to estimate your monthly payments on multifamily or commercial real estate financing?

The standard fixed-rate mortgage payment formula used for Fannie Mae loans is:

Real-World Multifamily Example (2026 Rates):

- Loan amount (P) = $2,000,000 (typical for a 20–30 unit apartment building at ~70% LTV)

- Interest rate = 6.0% (current Fannie Mae range: 5.5–6.5%)

- Loan term = 30 years (n n n = 360 months)

Monthly Principal & Interest Payment = $11,991

Pro Tip: At Commercial Lending USA, we shop Fannie Mae and Freddie Mac simultaneously to get you the lowest rate possible for your specific multifamily or commercial property.

2026 Fannie Mae Loan Payment Examples (30-year amortization, principal & interest only):

Loan Amount | Interest Rate | Monthly P&I Payment |

$1,000,000 | 5.5% | $5,678 |

$1,000,000 | 6.0% | $5,996 |

$1,000,000 | 6.5% | $6,321 |

$2,000,000 | 5.5% | $11,356 |

$500,000 | 6.5% | $3,160 |

Note: These are principal & interest only. Actual payments also include property taxes, insurance, and replacement reserves. Rates are current as of May 2026 and subject to change based on credit, property type, and market conditions.

Pro Tip: For a custom Fannie Mae mortgage calculator quote tailored to your exact multifamily or commercial property (including DSCR, LTV, and best execution vs. DSCR/bridge alternatives), submit your deal details. We’ll run numbers across Fannie Mae, Freddie Mac, and all 26 programs in minutes.

Who Should Get a Fannie Mae Loan in 2026?

Perfect for:

- Owners of stabilized multifamily properties

- Investors seeking long-term, fixed-rate financing

- Borrowers who want no prepayment penalty after the initial lock period

- Real estate investors with strong credit (680+) and clean tax returns

Better alternatives if:

- You need to close in under 30 days → Bridge or Hard Money Loan

- Property is not yet stabilized → Construction or Bridge Loan

- Credit score 500–680 → Hard Money or DSCR Loan

- You want zero tax returns → DSCR Loan is best choice

Fannie Mae Loan vs Other Popular Options (Side-by-Side)

Loan Type | Rate Range | LTV | Closing Speed | Docs Required | Prepayment Penalty | Best For |

Fannie Mae | 5.5–6.5% | 70%+ | 30–45 days | Full underwriting | Low after year 1 | Stabilized multifamily |

SBA 7(a)/504 | 6.5–9% | 75–80% | 45–90 days | Heavy | Yes (early years) | Owner-occupied businesses |

DSCR Loan | 6.5–9% | 75–80% | 15–30 days | Rental income only | None | Investment properties |

Bridge Loan | 9–12% | 70% | 7–21 days | Minimal | None | Acquisition & repositioning |

Hard Money Loan | 10–14% | 65% | 7–14 days | Asset-based | None | Fix-and-flip / short-term |

How to Qualify for a Fannie Mae Loan – Step-by-Step

_1779384578.webp)

- Pre-Qualify (5 minutes) – Submit basic property & borrower info

- Submit full package – 2–3 years tax returns, rent rolls, operating statements

- Appraisal & underwriting – Fannie Mae delegated underwriting available

- Rate lock & close – 30–45 days typical

For Commercial Multifamily Investors (5+ Units)

- Confirm property eligibility. Must be stabilized (90% occupancy for 90 days) with 5+ units.

- Prepare financials. 3 years of property operating statements, rent rolls, and borrower personal financial statements.

- Verify experience. 2+ years of multifamily ownership or management.

- Engage a DUS lender. Not all banks are approved. Work with a [Fannie Mae DUS lender] who can shop multiple capital sources.

- Obtain third-party reports. Appraisal, Phase I environmental, property condition assessment, and seismic (if applicable).

- Underwriting & commitment. DUS lenders underwrite to Fannie Mae standards; typical timeline: 45–60 days.

- Close & securitize. The loan is sold to Fannie Mae and often converted into a DUS mortgage-backed security.

Frequently Asked Questions (FAQ Schema Ready)

Q: What is a Fannie Mae loan?

A: A Fannie Mae loan is a conventional multifamily or commercial mortgage purchased and guaranteed by Fannie Mae in the secondary market, offering some of the lowest fixed rates and longest terms available in 2026.

Q: What are the current Fannie Mae loan rates in 2026?

A: Rates range from 5.5% to 6.5% depending on loan size, property type, and credit. Contact us today for a live quote.

Q: Are there good alternatives to Fannie Mae loans?

A: Yes. Strong alternatives include DSCR loans, bridge loans, hard money loans, No-Doc loans, USDA B&I, and CMBS programs. These options often close faster, require less documentation, and have no prepayment penalties.

Q: Does a Fannie Mae loan have a prepayment penalty?

A: Most have a declining or yield-maintenance prepayment structure in the early years, but many borrowers refinance or sell without penalty after the initial lock period.

Q: Can I get a Fannie Mae loan with a 650 credit score?

A: Minimum is typically 680+. Lower scores are better served with our DSCR or Hard Money programs.

0 Comments

Leave A Comment