Multifamily DSCR Loans: A Simple 2026 Guide for Investors

If you want to buy an apartment building or a small multi-unit property, a multifamily DSCR loan may be the easiest way to get funded. Instead of digging through your tax returns, the lender looks at one simple thing: does the property make enough rent to cover its loan payment? If it does, you can qualify.

This guide explains multifamily DSCR loans in easy words. You will learn how they work, what a good DSCR is, the current 2026 rates, what lenders want to see, and how to apply. Commercial Lending USA is a commercial mortgage broker and correspondent, and our job is to compare lenders for you and help you find the right fit.

What Is a Multifamily DSCR Loan?

DSCR stands for Debt Service Coverage Ratio. It is just a simple comparison of the property's income to its loan payment.

A multifamily DSCR loan is a loan for a rental property with multiple units, where you qualify based on the property's rent, not your personal income. So you do not need to show W-2s, pay stubs, or tax returns. The rent the building brings in does the talking.

This makes it a great fit for investors who own several properties, write off a lot of income on their taxes, or simply want to grow without the paperwork of a normal bank loan.

How Does a Multifamily DSCR Loan Work?

The lender takes the property's yearly income after expenses and divides it by the yearly loan payment. That gives the DSCR number.

- A DSCR of 1.0 means the rent exactly covers the loan payment.

- A DSCR above 1.0 means the property earns more than it costs to carry.

- Most lenders want a DSCR of about 1.20 to 1.25 to approve a multifamily loan.

The key difference from other DSCR loans is what the lender reviews. For a multifamily building, the lender looks closely at the rent roll for every unit, the vacancy rate, and the building's operating expenses. The more units you have, the more the lender focuses on how well the whole building runs.

What Counts as Multifamily?

Multifamily DSCR loans work for a range of property sizes:

Property Size | Best For |

2 to 4 units (duplex, triplex, fourplex) | New investors starting small |

5 to 10 units | Growing investors moving up to apartments |

Larger apartment complexes | Experienced investors with bigger portfolios |

Once a property has 5 or more units, lenders treat it as true commercial multifamily, and the building's income becomes even more important than your personal finances.

How to Calculate Your DSCR (With a Simple Example)

The formula is easy:

DSCR = Net Operating Income (NOI) / Total Loan Payment

First you find the NOI, which is the rent left over after operating costs:

Gross Rental Income - Operating Expenses = NOI

Operating expenses include things like property taxes, insurance, repairs, property management, a vacancy allowance, and any utilities you pay.

Example:

Let's say a small apartment building has:

Item | Amount (per year) |

Gross rental income | $150,000 |

Operating expenses | $60,000 |

Loan payment (principal + interest) | $75,000 |

Step 1, find the NOI:

$150,000 - $60,000 = $90,000 NOI

Step 2, find the DSCR:

$90,000 / $75,000 = 1.20 DSCR

A DSCR of 1.20 means the building earns 20% more than its loan payment. That meets the minimum for most lenders. If you raised the NOI to $95,000, the DSCR would climb to 1.27, which is even stronger and could earn you a better rate.

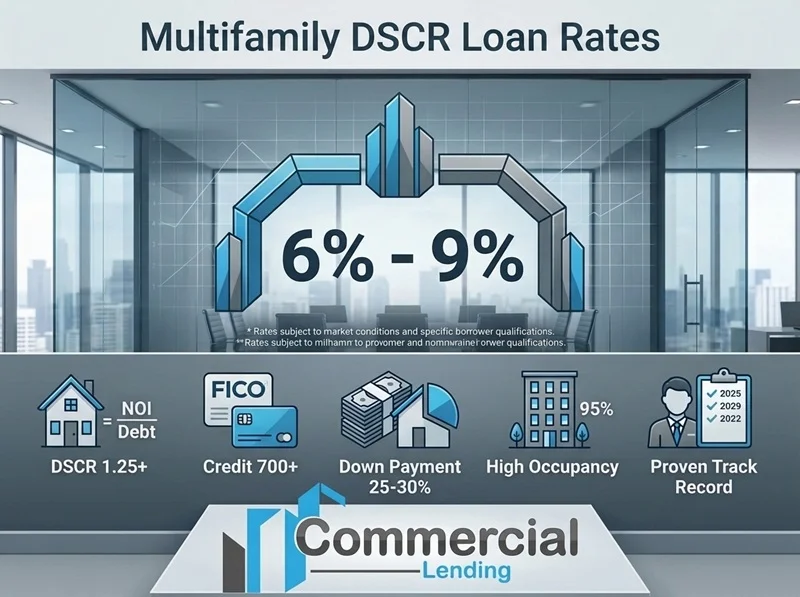

Multifamily DSCR Loan Rates in 2026

Rates change with the market, but as a general guide for 2026, multifamily DSCR loan rates usually fall in the high 6% to 9% range for strong deals. Your exact rate depends on your DSCR, your credit score, your down payment, and the size and condition of the building.

Here is a simple view of what moves your rate:

Factor | Better Rate When |

DSCR ratio | Higher (1.25 or more) |

Credit score | 700 or above |

Down payment | 25% to 30% |

Property condition | Well-maintained, high occupancy |

Experience | Proven track record with rentals |

Rates move daily, so always get a live quote before you plan a deal.

What Lenders Look For

Even though DSCR loans skip your personal income, lenders still check a few important things for a multifamily property:

- The property's DSCR. This is the biggest factor. The higher, the better.

- Credit score. Usually 660 or higher, with better scores earning better terms.

- Down payment (LTV). Most multifamily DSCR loans go up to 70% to 80% LTV, so you need 20% to 30% down.

- Cash reserves. Lenders often want 6 to 12 months of payments set aside as a safety net.

- Rent roll and occupancy. For 5+ units, a clean rent roll with steady occupancy is key.

Many lenders also let you borrow through an LLC, which many investors prefer for liability protection.

Standard Requirements at a Glance

Requirement | Typical Range |

Minimum DSCR | 1.20 to 1.25 |

Minimum credit score | 660+ |

Maximum LTV | 70% to 80% (lower for cash-out) |

Down payment | 20% to 30% |

Cash reserves | 6 to 12 months of payments |

Property type | 2 to 4 units, 5 to 10 units, larger complexes |

Borrowing entity | LLC, corporation, or individual |

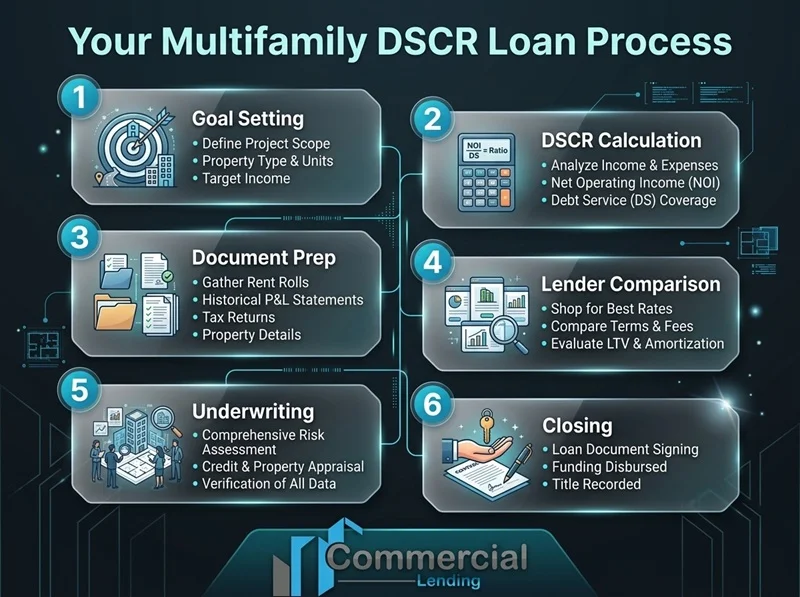

How to Apply for a Multifamily DSCR Loan

Here is the simple step-by-step:

- Know your goal. Decide if you are buying, refinancing, or taking cash out and what size building you want.

- Estimate the DSCR. Use the property's rent and expenses to check if it clears 1.20 to 1.25.

- Gather your documents. For DSCR loans you mainly need property documents: a rent roll, an appraisal, operating statements, the purchase contract, bank statements showing reserves, and your LLC papers if you use one.

- Compare lenders. This is where a broker helps. Commercial Lending USA compares options across a network of lenders to find the right terms for your building.

- Submit and underwrite. The lender reviews the property's income and your file.

- Close. You sign, bring your down payment, and the loan funds. DSCR loans often close faster than bank loans because there is less personal paperwork.

Ways to Improve a Weak DSCR

If your building's DSCR comes in too low, you have options:

- Raise the income. Bring rents up to market, reduce vacancy, or add income like parking, laundry, or pet fees.

- Lower the expenses. Trim operating costs where you can, such as shopping for better insurance.

- Put more money down. A bigger down payment means a smaller loan and a lower payment, which raises the DSCR.

- Choose a longer amortization. Spreading payments over a longer term lowers the monthly payment.

Why Work With Commercial Lending USA

Financing an apartment building is a big move, and the right guidance makes it simpler. As a commercial mortgage broker and correspondent, Commercial Lending USA:

- Reviews your building and packages your file the way lenders want to see it

- Compares options across a network of private lenders to find competitive terms

- Guides you through the rent roll, reserves, and appraisal steps

- Supports many loan types, including DSCR, bridge, and SBA, so you can plan your next move

To be clear, Commercial Lending USA is a broker and correspondent, not a direct lender, so we do not approve or fund loans ourselves. We connect you with the right lenders and manage the process. Commercial Lending USA is a member of the American Association of Private Lenders and is BBB accredited.

Ready to Fund Your Next Multifamily Property?

If you have a multi-unit deal in mind, the right DSCR loan can help you move fast and grow your portfolio. Reach out to Commercial Lending USA today for a free consultation. Call (855) 365-9200 or apply online, and we will help you compare your options.

Frequently Asked Questions

Are multifamily DSCR loans only for experienced investors?

No. Many lenders work with first-time investors too. Less experienced borrowers may just need a slightly higher credit score, a bigger down payment, or a stronger DSCR. Experienced investors often get better terms.

Do multifamily DSCR loans have higher rates than regular mortgages?

Usually a little higher, because they are investment-property loans based on the building's income. In 2026, strong multifamily DSCR deals generally fall in the high 6% to 9% range, depending on your file.

What if my DSCR is below the required ratio?

You can raise the rent, lower expenses, put more money down, or choose a longer amortization to improve it. If it still does not work, a bridge loan can be a short-term option while you stabilize the property.

Can I use a DSCR loan for a property held in an LLC?

Yes. Most DSCR lenders allow you to borrow through an LLC or corporation, which many investors prefer for liability protection.

Are there prepayment penalties?

Many DSCR loans have a prepayment penalty in the first few years, often on a step-down schedule. Some lenders offer no penalty in exchange for a slightly higher rate. Always check the terms before signing.

Can I use a multifamily DSCR loan for a property I live in?

No. DSCR loans are for investment properties only. If you live in the property, it is owner-occupied and does not qualify.

How many units can a multifamily DSCR loan cover?

From 2 to 4 unit properties up to larger apartment complexes with many units. The larger the building, the more the lender focuses on its income and occupancy.

How do I get started?

Call (855) 365-9200, email sales@commerciallendingusa.com, or apply online for a free review of your multifamily deal.

Disclaimer: Loan rates, terms, and requirements shown here are based on current programs and market conditions as of 2026 and may change at any time. Rates move with the market and vary by lender, property, and borrower. All loans are subject to lender approval and underwriting. This article is for general information only and is not financial or legal advice.

0 Comments

Leave A Comment