Multifamily Loans: The Complete 2026 Guide to Financing Apartment Properties

Buying, refinancing, or building an apartment property? Your loan choice matters. It shapes your returns for years, sometimes decades. Multifamily lending is not one product. It is a toolbox of a dozen-plus programs. Each one fits a different deal, borrower, and property type. Pick the wrong one, and you overpay for years. Pick the right one, and you lock in strong terms from day one.

This guide covers every major multifamily loan program in the U.S. today. You will learn how each one works. You will learn who qualifies, what it costs, and how to pick the right fit. It works for the first-time buyer closing on a fourplex. It also works for the developer structuring a $40 million HUD construction loan.

Rates and program terms move with the market. The figures here reflect general 2026 conditions. Confirm current pricing with a lender before you underwrite a deal.

What Are Multifamily Loans?

A multifamily loan funds a rental property with five or more units. This includes apartment buildings, garden-style complexes, mid-rise and high-rise properties, mixed-income communities, student housing, and senior living.

Here is the key difference from a home loan. The lender looks at the property's income first, not your paycheck. Lenders check the rent roll, the operating costs, and the net operating income (NOI). Your personal credit matters too, but it comes second. This is the big mental shift for investors moving from home loans to multifamily loans. The building qualifies for the loan. You matter, but the building matters more.

Why the 5-unit line matters:

1-4 unit properties get financed as home rentals. Lenders use Fannie Mae or Freddie Mac rules, or a DSCR loan. Your personal credit still plays a real role here.

5+ unit properties get financed as commercial real estate. Lenders look at cash flow. They use DSCR, LTV, and debt yield. They do not use your personal debt-to-income ratio.

Not sure which side your property falls on? That one answer shapes almost everything else. It affects your rate, your leverage, your paperwork, and which lenders will even look at your file.

How Multifamily Loans Work

Multifamily lending runs on different logic than home loans. Here is the short version.

The property's income sets the loan size. Lenders start with net operating income. That's rent, minus vacancy loss and operating costs, before debt payments. Then they work backward. They find the loan amount that income can safely support.

Two numbers cap your loan. The lower one wins. Every deal gets tested two ways. First, LTV: how much of the value will the lender finance? Second, DSCR: how much income cushion does the lender need above the loan payment? The lender calculates the max loan under each test. Then the lender uses whichever number is smaller. On a high-cap-rate deal in a smaller market, DSCR usually wins. On a low-cap-rate coastal asset, LTV often wins.

Recourse depends on the program. Agency loans (Fannie Mae and Freddie Mac) and HUD loans are usually non-recourse. That means the lender's recovery in a default is limited to the property itself. Fraud is the main exception. Bank loans, bridge loans, and many CMBS loans carry full or partial recourse. This is common for newer investors or smaller deals.

Rate equals index plus spread. Fixed-rate agency and CMBS loans get priced off the matching Treasury yield, plus a spread. The spread depends on property class and leverage. Floating-rate bridge and construction loans price off SOFR plus a spread.

Most permanent loans amortize over 25-30 years, even with a shorter term. Here is a common structure: 10-year fixed rate, 30-year amortization. You pay principal and interest as if the loan runs 30 years. But the balance comes due (or refinances) at year 10. HUD loans break this rule. They offer full-term amortization up to 35-40 years. No balloon payment.

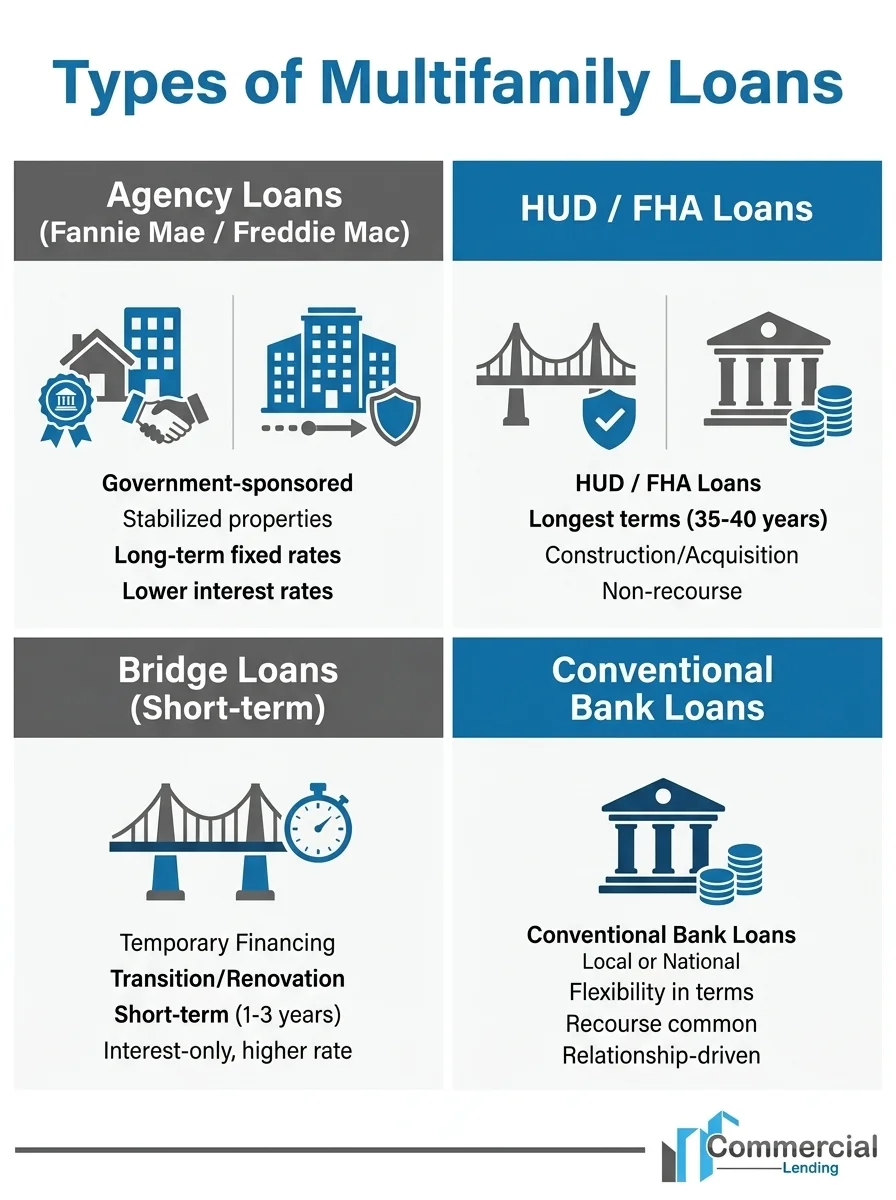

Types of Multifamily Loans

There is no single "multifamily loan." There is a toolbox. Here is every major program you will run into.

Fannie Mae Multifamily Loans (DUS Program)

Fannie Mae's Delegated Underwriting and Servicing (DUS) program is one of the largest multifamily capital sources in the country. These loans are non-recourse. They offer fixed and floating rates. Fannie Mae has special products for affordable, workforce, senior, student, and manufactured housing. Terms run 5-30 years with up to 30-year amortization. Leverage reaches roughly 80% LTV on the strongest deals. It runs lower for cash-out and value-add deals.

Freddie Mac Multifamily Loans

Freddie Mac's programs closely mirror Fannie Mae's. Non-recourse. Competitive fixed and floating pricing. Freddie Mac has dedicated products for affordable housing, seniors' housing, student housing, and small balance loans (typically $1M-$7.5M). Is your deal a smaller apartment property? Look into Freddie's small balance loan program. It moves faster and costs less to close than a full agency loan.

HUD 223(f) Acquisition & Refinance

HUD 223(f) insures loans for buying or refinancing existing, stable apartment properties. The property needs 5+ units and must be at least three years old. This program offers the longest fixed-rate term in the market: up to 35 years, fully amortizing, no balloon. Leverage runs up to 85% LTV on market-rate properties and up to 87% on affordable ones. What's the tradeoff for that leverage and rate stability? A longer, paperwork-heavy approval process, plus mortgage insurance premiums (MIP) added to your annual cost.

HUD 221(d)(4) New Construction & Substantial Rehabilitation

HUD 221(d)(4) funds ground-up multifamily construction or major rehab. The construction loan rolls straight into permanent financing, up to 40 years, at the same locked rate. No bank, agency, or CMBS lender offers that structure. It also gives the deepest leverage for construction: up to 85-87% loan-to-cost on qualifying deals. The cost? The most involved application process in the industry. Often 7-12 months from application to closing.

Multifamily Construction Loans

Outside HUD, construction financing comes from banks, debt funds, and life insurance companies. These loans are usually interest-only during construction. They price off SOFR (floating rate). They follow a draw schedule tied to construction milestones. Expect recourse, often with a burn-off after stabilization. Expect 65-75% loan-to-cost. Expect a required exit strategy at application, usually a permanent agency or HUD refinance.

Multifamily Bridge Loans

Bridge loans are short-term, typically 12-36 months. They carry a floating rate. Investors use them for value-add repositioning, lease-up, or fast-moving deals where the property does not yet qualify for permanent financing. They close fast, often in 2-4 weeks. Underwriting weighs your business plan and exit strategy more than current cash flow. The tradeoff is cost. Bridge rates run well above permanent financing. Most also carry origination fees of 1-2 points.

Multifamily Acquisition Loans

This is not one product. It is a use case. Acquisition financing can come from an agency loan, a bank, a bridge lender, or CMBS. It depends on the property's stability and your hold strategy. Stable, cash-flowing acquisitions usually go agency or bank. Value-add acquisitions usually go bridge.

Multifamily Refinance Loans

Investors refinance for a few reasons: to cut rate, extend term, cash out equity, or exit an expensive bridge loan once a property stabilizes. Rate-and-term refinances generally get better leverage than cash-out refinances. Why? The lender is not taking on extra risk beyond the existing balance.

Cash-Out Refinance

A cash-out refinance pulls equity from a stable property. You use it to fund your next deal, cover capital improvements, or pay an investor distribution. Lenders cap cash-out leverage lower than purchase leverage, usually 5-10 points of LTV lower. Expect a seasoning period too. Most lenders want 6-12 months of ownership before they will lend against your property's new, higher value instead of your original cost.

CMBS Loans (Conduit Loans)

Commercial mortgage-backed securities loans come from conduit lenders. The lender pools these loans with other commercial loans and sells them to investors as bonds. CMBS loans are non-recourse. They price competitively. They often flex more on property condition and smaller markets than agency lenders do. The tradeoff? Prepayment is restricted through defeasance or yield maintenance. Loan servicing after closing is far less flexible than agency or bank loans. That matters if you plan to sell early.

Bank Multifamily Loans

Banks remain a major multifamily capital source. This is especially true for smaller properties and borrowers who want a relationship lender. Bank loans flex more on structure and prepayment. But they typically carry recourse. They offer shorter fixed-rate periods, usually 5-10 years. They run more conservatively on leverage than agency programs.

Agency Loans (Umbrella Term)

"Agency loan" is the umbrella term for Fannie Mae and Freddie Mac multifamily products together. They set the benchmark that other multifamily loans get measured against. Why? Their mix of leverage, non-recourse structure, and rate stability.

Life Insurance Company Loans

Life companies lend their own capital. They put it into conservatively leveraged, high-quality multifamily assets, typically 55-65% LTV. In exchange, they offer very competitive fixed rates and long, stable relationships. These loans suit well-capitalized, experienced borrowers with top-tier properties in strong markets. Life companies are selective. They do not compete on maximum leverage.

Comparison at a Glance

Loan Program | Best For | Typical Max LTV | Typical Term | Recourse |

Fannie Mae DUS | Stabilized acquisitions/refi | Up to ~80% | 5-30 yrs | Non-recourse |

Freddie Mac | Stabilized acquisitions/refi, small balance | Up to ~80% | 5-30 yrs | Non-recourse |

HUD 223(f) | Acquisition/refi, max leverage & fixed rate | Up to 85-87% | Up to 35 yrs | Non-recourse |

HUD 221(d)(4) | Ground-up construction | Up to 85-87% loan-to-cost | Up to 40 yrs | Non-recourse |

Bridge Loans | Value-add, lease-up, fast closings | 65-80% (of cost) | 12-36 months | Often recourse |

CMBS | Stabilized, secondary/tertiary markets | 65-75% | 5, 7, 10 yrs | Non-recourse |

Bank Loans | Smaller deals, relationship lending | 65-75% | 5-10 yrs | Usually recourse |

Life Company Loans | Institutional-quality, low leverage | 55-65% | 5-25 yrs | Non-recourse |

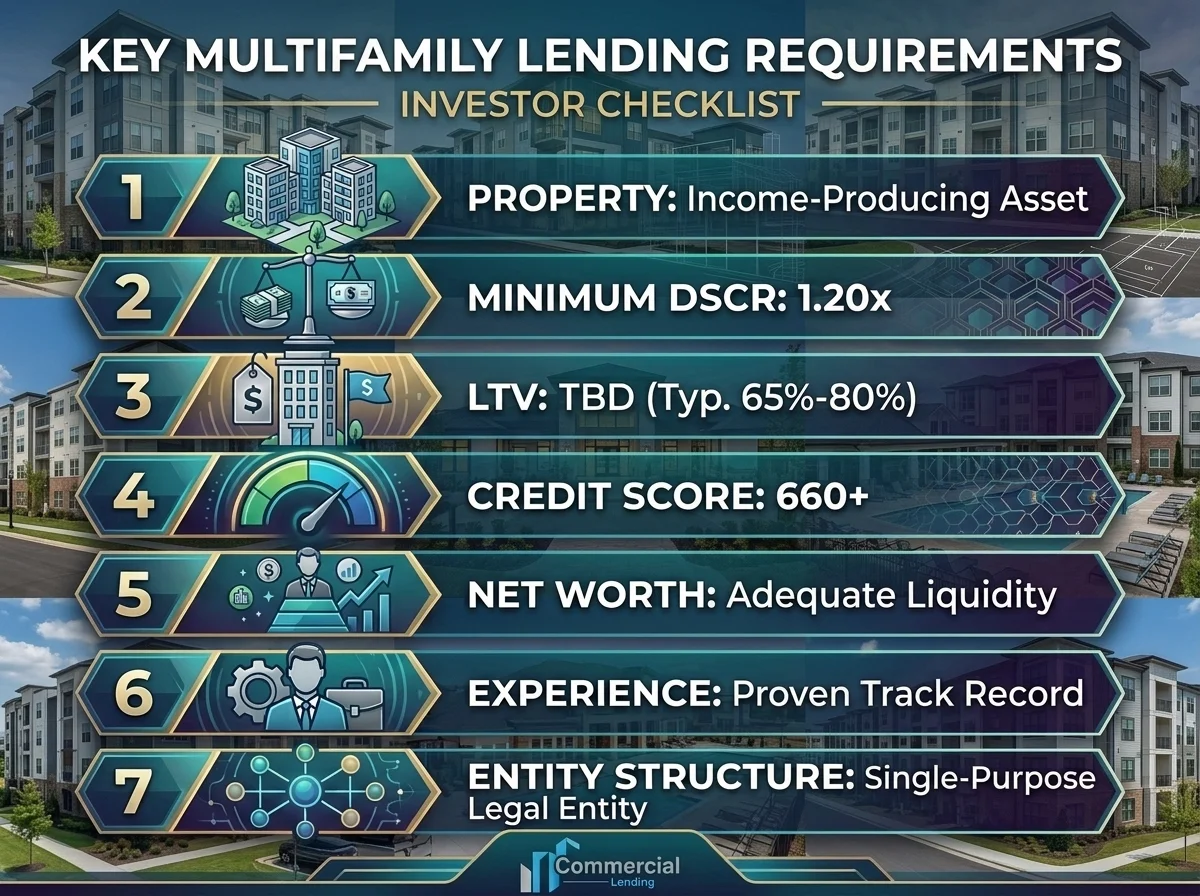

Multifamily Loan Requirements

Every program has its own rules. But most multifamily lenders check the same core things:

Property performance. Stable (or near-stable) occupancy. A rent roll that holds up under review. Expenses that match market comparables.

DSCR. Typically 1.20x-1.35x minimum. This depends on the program and property class.

LTV. Typically 65-80% for conventional and agency programs. Up to 85-87% for HUD.

Credit. Generally 660+ for the key principals. This varies by program.

Net worth and liquidity. Most programs want your net worth to match or beat the loan amount. Add 9-12 months of debt service in liquid reserves after closing.

Experience. Many lenders want to see prior multifamily ownership or management experience, especially on larger properties. This is negotiable for smaller deals with a strong co-sponsor or property manager.

Entity structure. Almost all commercial multifamily loans close in an LLC or similar single-asset entity, not in your own name.

Multifamily Loan Amounts

Loan size depends heavily on the program:

Program | Typical Loan Amount Range |

Freddie Mac Small Balance Loan | $1,000,000 – $7,500,000 |

Fannie Mae / Freddie Mac (standard) | $3,000,000 – $100,000,000+ |

HUD 223(f) / 221(d)(4) | $2,000,000 – $100,000,000+ (smaller deals possible, but less common) |

CMBS | $2,000,000 – $100,000,000+ |

Bank Loans | $500,000 – $25,000,000 (varies widely by institution) |

Bridge Loans | $1,000,000 – $50,000,000+ |

Life Company Loans | $5,000,000 – $100,000,000+ |

Have a smaller property, under roughly $1-2 million in loan size? Local banks, credit unions, or a Freddie Mac Small Balance Loan tend to fit best. Why? Agency and HUD underwriting carry fixed costs. Those costs make sense above that threshold, but not below it. Larger, institutional-scale deals can tap the full range of programs in this guide.

Multifamily Loan Rates in 2026

Rates move with whatever index they price off. There is no single "the rate" answer. Here is how the market breaks down heading through 2026:

HUD 223(f) fixed, 35-year: Among the lowest fixed rates in the market. Often prices tighter than 10-year agency debt.

Fannie Mae / Freddie Mac fixed: Priced off the matching-term Treasury, plus a spread. That spread typically runs low-to-mid 200s in basis points. It shifts with leverage and loan size.

CMBS fixed: Competitive with agency on stable deals. Sometimes wider on smaller or secondary-market loans.

Bank loans: Typically priced a bit above agency and HUD. This reflects shorter terms and recourse.

Bridge loans (floating): Priced off SOFR plus a wider spread. This reflects the short-term, higher-risk nature of the loan.

Life company loans: Often the tightest spreads available. But reserved for lower-leverage, high-quality assets.

Two things matter more than chasing the lowest headline rate. First: spreads and index rates move weekly. A number quoted today can go stale within a month. Always confirm current pricing before you underwrite a deal. Second: the "best rate" on paper is not always the best loan. A HUD 223(f) might beat a bank loan on rate. But if you need to sell in three years, prepayment penalties and MIP can erase that advantage fast. Rate is one variable out of five. Weigh rate, leverage, term, recourse, and prepayment flexibility together.

Down Payment Requirements

Down payment is just the flip side of leverage. A lender offering 75% LTV needs roughly 25% down, plus closing costs.

Program | Typical Down Payment |

HUD 223(f) / 221(d)(4) | 13-15% (market-rate); as low as 10-13% for affordable |

Fannie Mae / Freddie Mac | 20-25% |

CMBS | 25-35% |

Bank Loans | 25-35% |

Bridge Loans | 20-35% of total project cost |

Life Company Loans | 35-45% |

Here is a real-world example. Say you are buying a stable 24-unit property for $3,000,000. It qualifies for 75% LTV agency financing. You would need roughly $750,000 down, plus closing costs. Now compare that to a HUD 223(f) loan at 85% LTV on the same property: roughly $450,000 down. That $300,000 gap is exactly why experienced apartment investors pay close attention to HUD financing, even with its longer approval timeline.

Credit Score Requirements

Multifamily lenders check the credit of the "key principals." These are people with real ownership or signing power in the borrowing entity. Lenders do not just check one personal FICO score alone.

660-680: The practical floor for most conventional, agency, and bank programs.

700+: Unlocks better pricing tiers and, on some programs, extra leverage.

HUD programs: Weigh overall financial strength, prior real estate experience, and property performance more than a specific credit number. Credit history still gets reviewed.

Bridge lenders: Generally, the most flexible on credit. They weigh the asset and business plan more heavily. But that flexibility gets priced into the rate.

Does a key principal's credit fall short of a program's bar? Adding a stronger co-sponsor is often the fastest fix. It is far faster than trying to repair credit on a live deal timeline.

Debt Service Coverage Ratio (DSCR)

DSCR measures how much cushion a property's income gives above its debt payment.

DSCR = Net Operating Income ÷ Annual Debt Service

A DSCR of 1.25x means the property makes 25% more income than it needs to cover the loan payment. Most multifamily lenders require a minimum DSCR between 1.20x and 1.35x. HUD programs allow some of the lowest minimums in the industry, as low as roughly 1.11x-1.176x on affordable deals. That is a big reason HUD loans support such high leverage.

A worked example: A 30-unit property makes $420,000 in annual NOI. The lender requires a 1.25x DSCR. Max annual debt service allowed: $420,000 ÷ 1.25 = $336,000, or $28,000 a month. That monthly number sets your max loan amount under the DSCR test. Not the purchase price.

What if that number produces a smaller loan than the LTV test allows? DSCR becomes your binding constraint. No appraisal value changes that. This is the most misunderstood mechanic in multifamily lending. It is also why two buyers offering the same price on the same building can qualify for very different loan amounts if their expense or vacancy assumptions differ.

Loan-to-Value (LTV)

LTV = Loan Amount ÷ Lesser of Purchase Price or Appraised Value

LTV caps shift by program, property class, and deal type. Cash-out refinances almost always cap lower than acquisition financing. One caution for value-add deals: do not underwrite to a future, post-renovation appraised value. Most permanent lenders size the loan off the current as-is value, not your pro forma stabilized value. The exception: a bridge-to-permanent structure built for that purpose.

Debt Yield

Debt yield is a leverage-neutral risk measure. CMBS and bank lenders use it alongside DSCR and LTV.

Debt Yield = Net Operating Income ÷ Loan Amount

Unlike DSCR, debt yield ignores interest rate and amortization. It tells a lender what return they would earn on the loan amount if they had to foreclose and hold the property today. Most lenders want a minimum debt yield of 8-10% for stable multifamily.

Here is when this matters most. In a low-rate environment, DSCR math can support very high leverage. But debt yield might not. If DSCR and LTV both seem to support a bigger loan than debt yield allows, debt yield becomes your real ceiling.

Occupancy Requirements

Most permanent loan programs require the property to be "stabilized" before closing. That typically means physical occupancy of at least 90% (85-90% for HUD, depending on the program). This level must hold for a minimum period, often 90 days, before you apply.

Economic occupancy matters just as much as physical occupancy. Picture a building that is 95% occupied but full of below-market, rent-controlled, or late-paying tenants. It will not underwrite like a truly stable asset. Does your property fall short of stabilization? Maybe it is a recent buy in lease-up or a post-renovation repositioning. Bridge financing is the better fit until occupancy and rents stabilize. Then you refinance into permanent debt.

Eligible Property Types

Garden-style apartment communities

Mid-rise and high-rise apartments

Mixed-income and workforce housing

Affordable housing (LIHTC, Section 8, income-restricted)

Student housing

Seniors housing and independent living (age-restricted, non-licensed care)

Manufactured housing communities

Cooperative housing

Mixed-use properties with a majority residential share (treatment varies by lender; commercial space usually must stay under a set share of net rentable area or income)

A few property types fall outside standard multifamily programs. Hotels. Licensed skilled nursing and assisted living (these use separate HUD 232 and healthcare-specific programs). Single-purpose commercial buildings. These need different financing entirely.

Eligible Borrowers

Multifamily loans are open to a wide range of borrowers. Almost all are in a single-asset entity.

First-time multifamily investors (often with somewhat more conservative leverage or a co-sponsor requirement)

Experienced individual investors and syndicators

Real estate investment groups and family offices

Developers (for construction and rehab programs)

Nonprofit and for-profit affordable housing sponsors

Foreign nationals (on select programs, typically with adjusted leverage and extra paperwork)

Loan Terms & Amortization

Program | Fixed-Rate Term | Amortization |

HUD 223(f) | Full term | Up to 35 years |

HUD 221(d)(4) | Full term (construction + permanent) | Up to 40 years |

Fannie Mae / Freddie Mac | 5, 7, 10, 12, 15, 30 years | Up to 30 years |

CMBS | 5, 7, 10 years | 25-30 years |

Bank Loans | 3-10 years | 20-25 years |

Bridge Loans | 1-3 years | Interest-only |

Life Company Loans | 5-25 years | Up to 30 years |

Closing Costs

Budget roughly 2-5% of the loan amount for total closing costs on most conventional, agency, and bank multifamily loans. That covers:

Loan origination and underwriting fee (commonly 0.5-1.0% of the loan amount)

Third-party reports: appraisal, Phase I environmental, property condition assessment, seismic (where needed)

Legal fees (your counsel and, on many programs, the lender's counsel, which you usually reimburse)

Title insurance and recording fees

Application or processing deposit (often applied toward final closing costs)

HUD loans add program-specific costs. An initial mortgage insurance premium. An ongoing annual MIP. HUD-required third-party reports. Total closing costs run higher than conventional financing. Over the life of the loan, though, the lower rate and longer amortization usually make up for it.

Required Documents

Have these ready before you approach a lender. This is the single biggest lever you have over your own timeline.

Property-level:

Current rent roll

Trailing 12-24 months of operating statements (T-12)

Current-year and prior-year property tax bills

Insurance declarations page

Copies of leases (or a lease sample for larger properties)

Capital expenditure history and any deferred maintenance list

Survey and title commitment

Borrower and entity-level:

Entity formation documents (LLC operating agreement, articles of organization)

Personal financial statement and schedule of real estate owned for each key principal

Two to three years of tax returns (personal and entity, where needed)

Bank statements showing reserves and source of down payment

Resume or track record of multifamily ownership or management experience

Organizational chart showing ownership percentages

The Approval Process, Step by Step

Pre-qualification. Share the property's rent roll, T-12, and your financial profile. Get a first read on loan amount, rate, and terms.

Term sheet or letter of intent. The lender issues non-binding proposed terms. You review and negotiate before you commit.

Application and deposit. You formally apply and pay an application deposit. The lender orders third-party reports: appraisal, environmental, property condition.

Underwriting. The lender checks income, expenses, and your financials. Then the lender finalizes DSCR, LTV, and debt yield numbers.

Program-specific review. Agency loans go through Fannie Mae or Freddie Mac approval, on top of the lender's own underwriting. HUD loans go through HUD's review and firm commitment process. This adds time. But it also underwrites the deal to a government-insured standard.

Loan committee approval. The lender's credit committee signs off internally.

Closing documentation. Loan documents, title work, and legal review get finalized.

Funding. Loan proceeds get disbursed at closing. For construction loans, funds release through an ongoing draw schedule instead.

Realistic Timeline

Program | Typical Timeline |

Bridge Loans | 2-4 weeks |

Bank Loans | 30-60 days |

Fannie Mae / Freddie Mac | 45-75 days |

CMBS | 45-75 days |

HUD 223(f) | 4-7 months |

HUD 221(d)(4) | 7-12 months |

Here is the biggest lever you have over closing speed. It is not the lender. It is how fast and complete your paperwork is. Deals stall far more often from a late rent roll or a missing tax return than from lender delays.

Common Mistakes Borrowers Make

Underwriting to the seller's or broker's pro forma instead of trailing actuals. Projected NOI and verified, actual NOI are often very different numbers. Lenders underwrite to the actual figure.

Ignoring debt yield in a low-rate environment. A deal can clear DSCR with room to spare and still get capped by debt yield. This surprises borrowers who thought DSCR was the only test that mattered.

Waiting to gather documents until after applying. This is the single most common cause of blown timelines and lost rate locks.

Choosing the lowest rate without checking prepayment terms. A locked-in HUD or agency loan with defeasance or yield maintenance can be very expensive to exit early if your hold period changes.

Underestimating reserve requirements. Many borrowers budget for the down payment and closing costs. Then they forget the 9-12 months of post-closing liquidity many lenders require.

Assuming all lenders treat 2-4 unit and 5+ unit properties the same. They do not. Bringing a duplex deal to a commercial multifamily lender (or the reverse) wastes weeks.

Skipping the exit strategy on a bridge loan. Bridge lenders ask for your refinance or sale plan upfront. Borrowers without one risk running out the clock on a maturing bridge loan with no takeout in place.

Real-World Example: Sizing a Deal

Here is how these numbers actually play out on a live deal. The scenario below is a composite, built from patterns we see often. It is not one client's file.

The deal: A first-time multifamily buyer signed a contract on a 28-unit garden-style apartment community for $4,200,000. The broker's marketing package projected NOI of $294,000. That number assumed every unit hit full market rent right at closing.

The problem: The real trailing 12-month operating statement told a different story. Eight units were leased below market to long-term tenants who were not turning over soon. Actual collections ran about 12% below the pro forma rent roll. Verified trailing NOI came in at roughly $252,000, not $294,000.

The math: The lender required a 1.25x DSCR. At a market rate in the mid-6% range, that $252,000 in verified NOI supported a loan of roughly $3,150,000. That was well below the $3,780,000 the 75% LTV test on the original $4,200,000 price would have allowed. DSCR was the binding constraint here, not LTV. It capped the deal well below what the buyer first assumed.

The fix: The buyer did not walk away. Instead, the buyer renegotiated the price down to $3,850,000. The buyer also raised the down payment slightly and structured the loan on verified trailing NOI, not the broker's projection. This kept the deal non-recourse. It also preserved a healthy DSCR cushion for the buyer's first year of ownership, when surprise expenses show up most.

The takeaway: The gap between a marketing pro forma and verified trailing income is the top reason a multifamily deal does not size the way a buyer expects. Get the trailing 12-month operating statement, not just the rent roll, before you go firm on price. It is the cheapest insurance in the whole process.

Pros and Cons of Multifamily Loans

Pros

Income-based underwriting lets strong properties qualify even when a sponsor's personal income is complex or unconventional

Non-recourse options (agency, HUD, CMBS, life company) limit personal liability beyond standard carve-outs

Long fixed-rate periods and amortization schedules, especially HUD, give you long-term rate certainty

HUD programs offer high leverage compared to other commercial asset classes

A wide range of programs means most deals have a financing path, from a 5-unit building to a 400-unit development

Cons

More paperwork and underwriting steps than a home loan

Longer closing timelines, especially for HUD and agency loans

Prepayment penalties (yield maintenance, defeasance, step-down) are standard on fixed-rate agency, HUD, and CMBS loans

Reserve and net worth requirements can block newer investors without a strong co-sponsor

Rate and leverage tie closely to property performance; a soft rent roll limits your options, no matter how strong you are as a borrower

Best Multifamily Loan Programs Compared

If your priority is... | Best-fit program |

Maximum leverage | HUD 223(f) / 221(d)(4) |

Lowest long-term fixed rate | HUD 223(f) |

Fastest closing | |

Ground-up construction | HUD 221(d)(4) or bank/debt fund construction loan |

Value-add repositioning | Bridge loan, refinanced into agency/HUD post-stabilization |

Non-recourse with moderate leverage and fast execution | Fannie Mae / Freddie Mac |

Smaller balance apartment deal ($1M-$7.5M) | Freddie Mac Small Balance Loan or local bank |

Lowest possible rate on a low-leverage, top-tier asset | Life insurance company loan |

Secondary/tertiary market flexibility | CMBS |

Cashing out built-up equity | Agency or bank cash-out refinance |

How to Choose the Right Multifamily Loan

Work through these questions in order. They narrow the field faster than comparing rates alone.

Is the property stable today, or does it need lease-up or renovation first? Stable properties fit permanent financing: agency, HUD, CMBS, bank. Properties that are not stable yet need a bridge loan, with a permanent refinance planned once occupancy and NOI stabilize.

How long do you plan to hold? Short hold? Avoid heavy prepayment penalties. Look at a bank loan or a bridge structure. Long hold? HUD or agency fixed-rate financing captures the most long-term value.

How much leverage do you actually need? Do not max out leverage just because it is available. Higher leverage means a tighter DSCR cushion and less room for error if expenses rise or occupancy softens.

Does recourse matter to you? Scaling a portfolio? Non-recourse financing preserves your balance sheet for the next deal.

How fast do you need to close? A tight closing date on a competitive deal may rule out HUD entirely, no matter how good the rate looks on paper.

What is your experience level? First-time multifamily buyers should expect more conservative leverage, or a co-sponsor requirement on larger deals. Plan for that upfront instead of discovering it mid-underwriting.

Multifamily Lending Glossary

Quick definitions for terms used throughout this guide:

NOI (Net Operating Income): Rent income, minus vacancy loss and operating costs, before debt payments and capital spending.

DSCR (Debt Service Coverage Ratio): NOI divided by annual debt service. It measures the income cushion above the loan payment.

LTV (Loan-to-Value): Loan amount divided by the lesser of purchase price or appraised value.

Debt Yield: NOI divided by loan amount. A leverage-neutral risk measure that ignores interest rates.

Non-Recourse: A loan where the lender's recovery in a default is limited to the property itself, aside from fraud or waste carve-outs.

T-12: A trailing 12-month operating statement. It shows a property's real income and expenses.

Stabilized Property: A property that has hit a set occupancy level, commonly 90%+, and held it for a set period, usually 90 days.

Yield Maintenance: A prepayment penalty. It pays the lender back for lost interest if you pay off a fixed-rate loan early.

Defeasance: A prepayment method common on CMBS loans. You swap government securities in as loan collateral instead of paying the loan off directly.

Loan-to-Cost (LTC): Loan amount divided by total project cost. Used mainly in construction lending.

Key Principal: A person with real ownership or signing power in the borrowing entity. The lender underwrites this person's credit and financial strength.

Cap Rate: Net operating income divided by property value or purchase price. A measure of unleveraged return.

Why Borrowers Choose Commercial Lending USA

Commercial Lending USA structures multifamily financing across every program in this guide. Fannie Mae. Freddie Mac. HUD 223(f) and 221(d)(4). CMBS bank. Bridge. Life company financing. That means the recommendation you get fits your deal. It is not based on which product a single lender happens to sell.

Our team brings 30 years of real estate and mortgage lending experience to every file. We have underwritten deals across nearly every property type and market cycle in this guide. We work directly with acquisition, refinance, construction, and value-add borrowers nationwide.

Are you evaluating a multifamily acquisition, refinance, or construction project? Talk to our team before you go under contract. The right financing structure often changes how you should negotiate the deal itself.

Ready to explore your multifamily loan options? Contact Commercial Lending USA to get matched with the right program for your property, timeline, and long-term strategy.

Frequently Asked Questions

1. What is considered a multifamily property for loan purposes?

Properties with five or more units count as commercial multifamily. Properties with two to four units use residential investment property rules instead.

2. What credit score do I need for a multifamily loan?

Most conventional, agency, and bank programs want a minimum of 660-680 for key principals. Requirements vary by program. Some lenders weigh property performance and sponsor experience more than a single credit number.

3. How much down payment do I need for a multifamily property?

It ranges from 13-15% on HUD-insured loans up to 35-45% for conservatively leveraged life company loans. Most conventional and agency financing falls in the 20-30% range.

4. What is a good DSCR for a multifamily loan?

Most lenders want a minimum DSCR between 1.20x and 1.35x. That means the property's net operating income beats the annual debt service by 20-35%. Some HUD programs allow lower minimums, which is part of why they support higher leverage.

5. Are multifamily loans recourse or non-recourse?

It depends on the program. Fannie Mae, Freddie Mac, HUD, CMBS, and life company loans are usually non-recourse, aside from standard fraud and waste carve-outs. Bank loans and many bridge loans are usually recourse, especially for smaller balances or newer borrowers.

6. What is the difference between HUD 223(f) and HUD 221(d)(4)?

HUD 223(f) finances the purchase or refinance of existing, stable apartment properties. HUD 221(d)(4) finances new construction or major rehab. The construction loan converts into permanent financing at the same locked rate.

7. Can first-time investors qualify for a multifamily loan?

Yes. Expect somewhat more conservative leverage, a possible co-sponsor requirement on larger deals, or a preference for smaller properties until you build a track record. Property performance still carries real weight, no matter your experience level.

8. How long does it take to close a multifamily loan?

It ranges from 2-4 weeks for bridge loans to 45-75 days for agency and CMBS loans to 4-12 months for HUD-insured financing, depending on program complexity.

9. What is the maximum LTV available on a multifamily loan?

HUD programs offer the highest leverage in the multifamily market: up to 85% LTV on market-rate properties and up to 87% on qualifying affordable housing.

10. Do multifamily loans require personal income documentation?

Multifamily loans get underwritten mainly on the property's income and the borrowing entity's financial strength. But lenders still review key principals' personal financial statements, tax returns, and real estate schedules as part of underwriting.

11. What is debt yield, and why does it matter?

Debt yield (NOI divided by loan amount) is a leverage-independent risk measure. Lenders use it alongside DSCR and LTV. It can cap your loan amount even when DSCR and LTV would allow a bigger loan, especially in low-rate environments.

12. Can I get a multifamily loan for a property that is not fully occupied yet?

Permanent loan programs generally require the property to be stable, commonly 85-90% physical occupancy held for a set period. Properties still in lease-up or renovation typically use bridge financing until they stabilize, then refinance into permanent debt.

13. What is the difference between a bridge loan and a permanent multifamily loan?

Bridge loans are short-term (12-36 months), floating-rate financing for transitional properties. They price higher to reflect that risk. Permanent loans, like agency, HUD, CMBS, bank, and life company loans, finance stable properties with longer fixed-rate terms and lower relative pricing.

14. Can foreign nationals get multifamily financing in the U.S.?

Yes, on select programs. Foreign national borrowers should expect adjusted leverage, extra paperwork, and a smaller pool of lenders willing to underwrite the file.

15. What happens if I need to sell before my multifamily loan term ends?

Most fixed-rate agency, HUD, and CMBS loans carry prepayment penalties, like yield maintenance, defeasance, or a step-down schedule. These can get expensive if triggered early. Planning a shorter hold? Talk to your lender about prepayment flexibility before you lock a loan structure, not after.

0 Comments

Leave A Comment