Lite Doc Loan:Complete Guide for Self-Employed Borrowers and Investors

Getting a home or investment loan is supposed to be straightforward, but for millions of people it isn't. If you are self-employed, own a business, work on commission, or write off a lot of expenses on your taxes, a regular bank often says "no," not because you can't afford the loan but because your tax returns don't show enough income on paper.

This is exactly the problem a lite doc loan solves. Instead of forcing you to prove every dollar with years of tax returns, a lite documentation loan lets you qualify with simpler paperwork, usually just your bank statements. In this complete guide, we will explain what a lite doc loan is, how it works, who it is for, the rates and terms, and how to qualify.

What Is a Lite Doc Loan?

So, what is a lite doc loan? It is a mortgage that uses "light" documentation to prove your income, instead of the full stack of paperwork a traditional loan demands. With a normal loan, the bank wants two years of tax returns, W-2s, pay stubs, and more. With a lite doc mortgage, you can often qualify using your bank statements alone.

This makes it one of the best options for people whose real income is strong but whose tax returns don't tell the full story. That is why a lite doc loan for self-employed borrowers is so popular. Business owners legally write off expenses to lower their taxable income, which is smart for taxes but makes them look "poorer" to a bank.

A lite doc loan is part of a family of alternative documentation loan products. It sits between a full-documentation loan, which needs lots of paperwork, and a no doc loan, which needs almost none. You give some proof, just not all of it.

How Does a Lite Doc Loan Work?

The idea is simple. Instead of digging through your tax returns, we look at the money actually flowing through your bank account. If your deposits show you can comfortably handle the payments, you can qualify.

Here is the typical process for our lite doc home loan:

- You apply. You tell us about the property and your situation.

- You share bank statements. This is the main proof of income, with no tax returns needed.

- We review the deal. We look at your deposits, the property value, and your down payment.

- You get approved. Because there is less paperwork, the process is usually faster.

- You close. You get your loan and move forward with your purchase or refinance.

Because this is a no-tax-return mortgage, self-employed people, freelancers, and business owners avoid the biggest headache of traditional lending.

Lite Doc Loan Requirements

Here are the actual lite doc loan requirements for our program, laid out in one clear table:

Feature | Our Lite-Doc Loan Program |

Interest rate | 8-11% |

LTV (Loan-to-Value) | Up to 75% |

Minimum down payment | 25% |

Loan term | Up to 30 years |

Minimum credit score | 660+ |

Bank statements | Required |

Tax returns | Not required |

Maximum loan amount | Up to $5 million per property |

As you can see, the trade-off is simple. You bring a slightly larger down payment of 25% and your bank statements, and in return you skip the tax returns entirely. For many self-employed buyers, that is a fair and welcome deal.

Lite Doc Loan Rates: What to Expect

Our lite doc loan rates sit in the 8-11% range. That is typically a little higher than a full-documentation loan, and there is a good reason. The lender is taking on a bit more risk by not reviewing tax returns. You are paying a small premium for the convenience, speed, and the ability to qualify at all.

For a self-employed borrower who would otherwise be turned away by a bank, that slightly higher rate is usually well worth it, because the alternative is no loan at all.

Who Is a Lite Doc Loan For?

A lite doc loan is a great fit if you are

- Self-employed or a freelancer with variable income

- A small business owner who writes off a lot of expenses

- A real estate investor wanting a lite doc loan for investment property

- Someone who earns through commissions, tips, or 1099 work

- A borrower with strong bank deposits but messy or low tax returns

In fact, our qualification guidelines specifically point self-employed borrowers to this option when their tax returns don't reflect enough income for a traditional loan. If that sounds like you, this loan was practically designed for your situation.

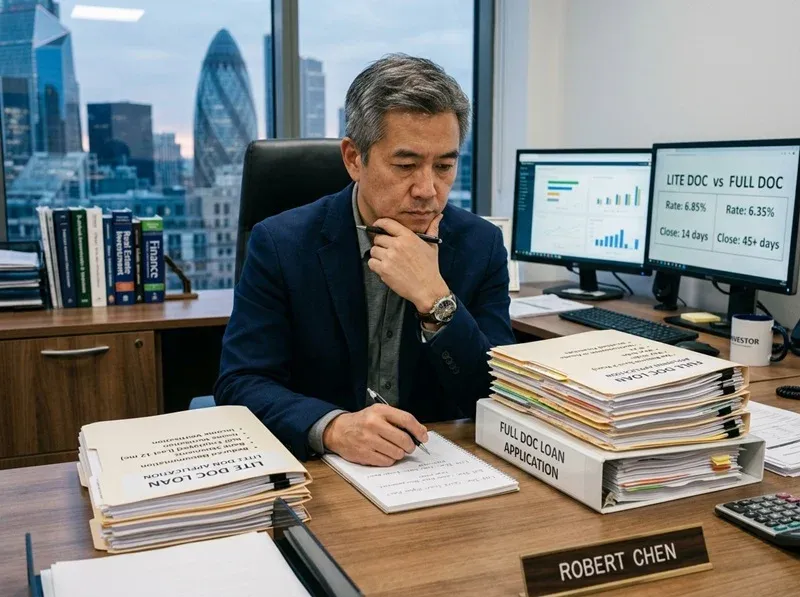

Lite Doc vs Full Doc Loan: What's the Difference?

Many borrowers ask about lite doc vs. full doc loans. Here is a side-by-side comparison so you can see it clearly:

Feature | Lite Doc Loan | Full Doc Loan |

Tax returns required? | No | Yes (usually 2 years) |

Main income proof | Bank statements | Tax returns, W-2s, pay stubs |

Best for | Self-employed, business owners | W-2 employees with steady pay |

Paperwork | Light | Heavy |

Speed | Faster | Slower |

Interest rate | Slightly higher (8-11%) | Slightly lower |

Down payment | 25% | Can be lower |

If you have a regular salaried job with clean pay stubs, a full doc loan may get you a lower rate. But if your income is from self-employment or hard to document, a lite doc loan is often the only realistic path and a very good one.

How a Lite Doc Loan Compares to Our Other Programs

A lite doc loan is one of several flexible options we offer for borrowers who don't fit the standard bank mold. Here is how it compares to two close cousins:

Feature | Lite-Doc Loan | No-Doc Term Loan | Stated Income Loan |

Interest rate | 8-11% | 10-12% | 8-11% |

LTV (max) | Up to 75% | Up to 70% | Up to 75% |

Down payment | 25% | 30% | 25% |

Bank statements | Required | Not required | Required |

Tax returns | Not required | Not required | Not required |

Loan term | Up to 30 years | Up to 30 years | Up to 30 years |

Credit score | 660+ | 660+ | 660+ |

The lite doc loan often gives you a better rate and LTV than a no-doc loan because providing bank statements lowers the lender's risk. If you can show bank statements, lite doc is usually the smarter choice over no-doc.

Pros and Cons of a Lite Doc Loan

Pros | Cons |

No tax returns required | Slightly higher rate than full doc |

Great for self-employed borrowers | Larger down payment (25%) |

Faster, simpler process | Need a 660+ credit score |

Long 30-year terms available | Bank statements still required |

Works for investment properties | Not ideal if you have clean W-2 income |

How to Qualify for a Lite Doc Loan

Wondering how to qualify for a lite doc loan? The good news is the requirements are straightforward. To get approved, you generally need:

- A credit score of 660 or higher

- At least a 25% down payment

- Bank statements that show healthy, steady deposits

- A property that meets standard value guidelines

You do not need tax returns, which removes the single biggest obstacle for self-employed borrowers. Bring clean bank statements and a solid down payment, and you are most of the way there.

Can You Use a Lite Doc Loan to Refinance?

Yes. A lite doc refinance works just like a purchase loan, only you are replacing an existing loan instead of buying it. This is a popular move for self-employed homeowners who bought with a high-rate loan or a hard money loan and now want a longer 30-year term with simpler paperwork. If you want to lower your payment or pull out equity without showing tax returns, a lite doc refinance is worth exploring.

Why Choose Us for Your Lite Doc Loan

We aim to be one of the best lite doc loan lenders by keeping things simple, fast, and fair. With us you get:

- No tax returns, just bank statements

- Loans up to $5 million per property

- Long terms up to 30 years

- Competitive rates from 8%

- Funding for investment properties

- Real people who understand self-employed income

If you have been searching for lite doc loan lenders near me, our goal is to be the clear, reliable choice that finally says "yes."

Ready to Get Started?

If your tax returns have been holding you back, a lite doc loan could be your answer. Reach out today and we will look at your situation and tell you exactly what is possible, with no pressure and no piles of paperwork.

Frequently Asked Questions (FAQ)

What is a Lite Doc loan, and how does it work?

A lite doc loan is a mortgage that uses light documentation, usually just bank statements, to prove your income instead of full tax returns. You apply and share your bank statements; we review your deposits and the property, and you get approved. It is built for people whose income is strong but hard to document the traditional way.

What are the requirements for a Lite Doc loan?

For our program you need a 660+ credit score, at least a 25% down payment, and bank statements showing steady deposits. Tax returns are not required. The maximum loan amount is up to $5 million per property.

What are the typical interest rates for a Lite Doc loan?

Our Lite Doc loan rates range from 8 to 11%. That is slightly higher than a full-documentation loan because the lender takes on a bit more risk by skipping tax returns, but it is usually well worth it for self-employed borrowers.

Who are the best Lite Doc loan lenders near me?

The best lender is one with clear terms, fair rates, and experience working with self-employed income. We offer lite doc loans with no tax returns, rates from 8%, terms up to 30 years, and loans up to $5 million. Reach out to see if your deal qualifies.

Can I get a Lite Doc loan if I'm self-employed?

Yes, this is exactly who the loan is designed for. Business owners, freelancers, and 1099 workers often show low income on tax returns because of write-offs. A lite doc loan lets you qualify using bank statements instead.

Lite Doc loan vs Full Doc loan: What's the difference?

A full doc loan requires tax returns, W-2s, and pay stubs. A lite doc loan uses bank statements instead. Full doc may offer a slightly lower rate for salaried workers, but lite doc is far easier for self-employed borrowers and closes faster.

How much can I borrow with a Lite Doc loan?

With our program you can borrow up to $5 million per property, depending on the property value, your down payment (minimum 25%), and your credit. The maximum LTV is up to 75%.

Do Lite Doc loans require tax returns?

No. That is the main benefit. A lite doc loan is a no-tax-return mortgage. You qualify with bank statements instead, which is ideal for self-employed and business-owner borrowers.

Best lenders offering Lite Doc loans

The best lite doc lenders fund quickly, explain every term up front, and understand self-employed income. At Commercial Lending USA, our program offers competitive 8-11% rates, up to 75% LTV, 30-year terms, and loans up to $5 million, with no tax returns required.

How to qualify for a Lite Doc loan quickly

Bring three things: a 660+ credit score, a 25% down payment, and clean bank statements showing steady deposits. Because there are no tax returns to review, the process moves much faster than a traditional bank loan.

Disclaimer: Loan terms, rates, and requirements shown here are based on our current programs and may change. All loans are subject to approval and underwriting. This article is for general information only and is not financial or legal advice.

0 Comments

Leave A Comment