CMBS Loan: The Complete Guide to Commercial Mortgage-Backed Securities Financing

If you own or plan to buy commercial property, you will likely encounter the term CMBS loan" (or "conduit loan"). While it sounds technical, the underlying concept is straightforward. This is one of the most popular tools in commercial real estate because it offers large loan amounts, long amortization schedules, and competitive fixed rates.

This comprehensive guide breaks down how CMBS loans work, outlines current market benchmarks, details underwriting requirements, and highlights critical structural features such as prepayment penalties and defeasance that most borrowers overlook.

What is a CMBS (Conduit) Loan?

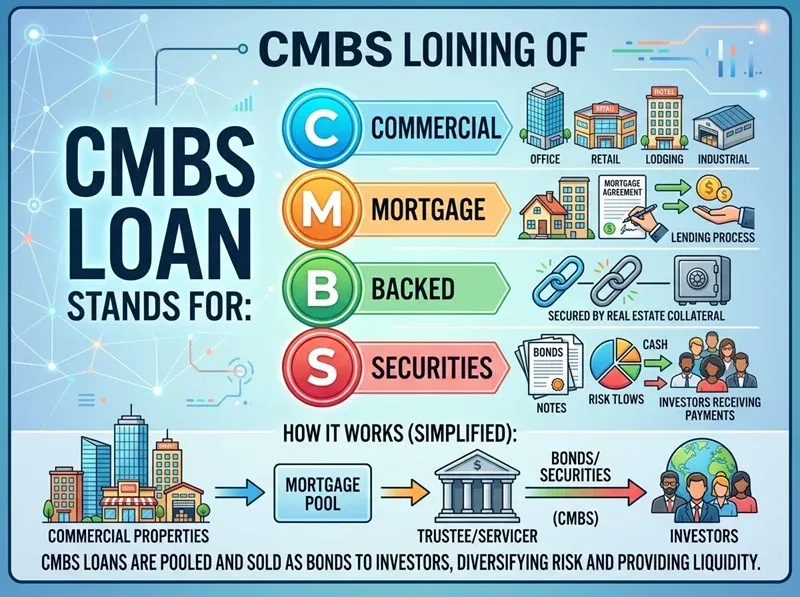

A Commercial Mortgage-Backed Securities (CMBS) loan is a first-priority commercial mortgage packaged into a pool with similar debts and sold to Wall Street investors as bonds.

In a traditional bank loan, the lender keeps your mortgage on their balance sheet. With a CMBS loan, the originating bank acts as a "conduit." They fund your loan, immediately pass it into a diversified pool, and securitize it.

Why Borrowers Choose CMBS

- Predictable Expenses: Long-term, fixed interest rates protect against market volatility.

- Lower Monthly Payments: Amortization schedules up to 30 years maximize monthly cash flow.

- Non-Recourse Structure: Most conduit loans limit personal liability, protecting your personal assets in a default.

How Does a CMBS Loan Work?

Here is how a CMBS loan works, step by step: [Borrower Originates Loan]➔ [Lender Pools Mortgages]➔ [Wall Street Securitizes Bonds] ➔ [Servicer Manages Payments]

- You borrow. A lender gives you a loan on your commercial property.

- The loan is pooled. Your loan is grouped with many other commercial loans. These groups are called CMBS loan pools.

- Bonds are created. The pool is turned into bonds and sold to investors.

- A servicer collects payments. A loan servicer collects your monthly payment and passes it on to the bond investors.

- You repay over time. You make payments until the loan term ends, usually with a large final balloon payment.

This pooling process is the heart of the CMBS loan structure. Because the risk is spread across many investors, lenders can often offer attractive fixed rates and large loan sizes.

Who Is the Lender on a CMBS Loan?

Because your loan is sold to investors, you will not deal with the original lender post-closing. Instead, your loan is managed by two specialized entities:

- Master Servicer: Handles routine day-to-day operations, including collecting monthly payments, managing escrow accounts, and processing standard requests.

- Special Servicer: Steps in during financial distress or default. They also manage complex, non-routine property events, such as lease approvals, property assumptions, or easement requests.

CMBS Loan Rates and Terms

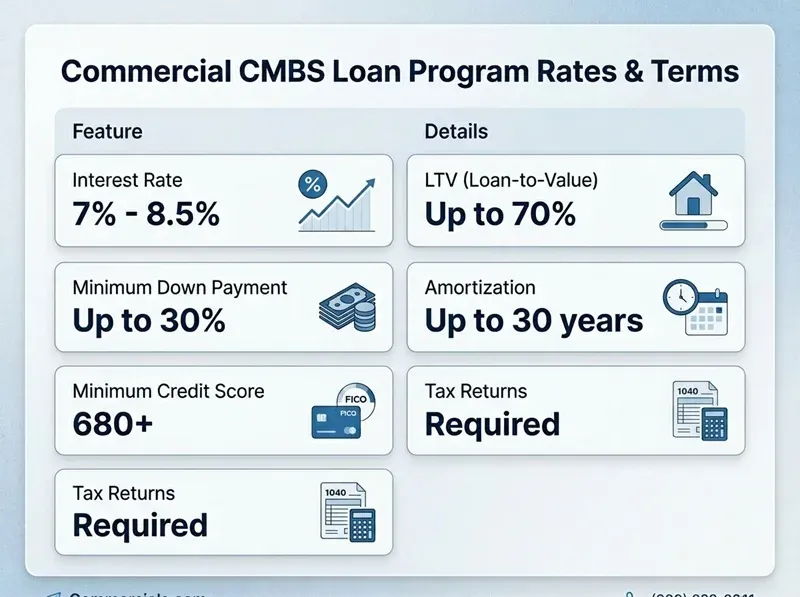

Borrowers always want real numbers, so here are the rates and terms for our commercial CMBS loan program:

Feature | Our CMBS Loan Program |

Interest rate | 7-8.5% |

LTV (Loan-to-Value) | Up to 70% |

Minimum down payment | Up to 30% |

Amortization | Up to 30 years |

Minimum credit score | 680+ |

Bank statements | Required |

Tax returns | Required |

A few notes on CMBS loan rates. CMBS loans are usually fixed-rate, which gives you stable, predictable payments. The fixed loan term is commonly 5, 7, or 10 years, while the CMBS loan amortization can stretch up to 30 years. That long amortization keeps your monthly payment lower, but it usually leaves a balloon payment due at the end of the term.

If you are searching for current CMBS loan rates or CMBS loan rates today, remember that market rates move constantly with the bond market. The range above reflects our program, but always confirm live CMBS loan pricing before you plan a deal.

CMBS loan size and LTV

The CMBS loan size can be large, which is one reason investors like these loans for bigger properties. The CMBS loan-to-value on our program goes up to 70%, meaning you generally need a down payment of up to 30%. Many lenders also set a CMBS loan minimum, often around $2 million, because the cost of securitizing very small loans is high.

CMBS Loan Requirements

Here are the typical CMBS loan requirements for approval:

- A credit score of 680 or higher

- A down payment of up to 30%

- Strong, stable property income (the property must pay for itself)

- Full documentation, including bank statements and tax returns

- A property in good condition with reliable tenants

CMBS lending is property-focused, so CMBS loan underwriting looks closely at the building's income, expenses, and value. This is part of what characterizes a CMBS loan: the property's ability to generate income matters even more than the borrower's personal finances.

CMBS loan documents

The CMBS loan documents are detailed because the loan will be sold to investors. Expect a thorough CMBS loan agreement, plus property financials, leases, and CMBS loan insurance requirements such as property and liability coverage. The paperwork is heavier than a simple bank loan, but it protects everyone in the bond pool.

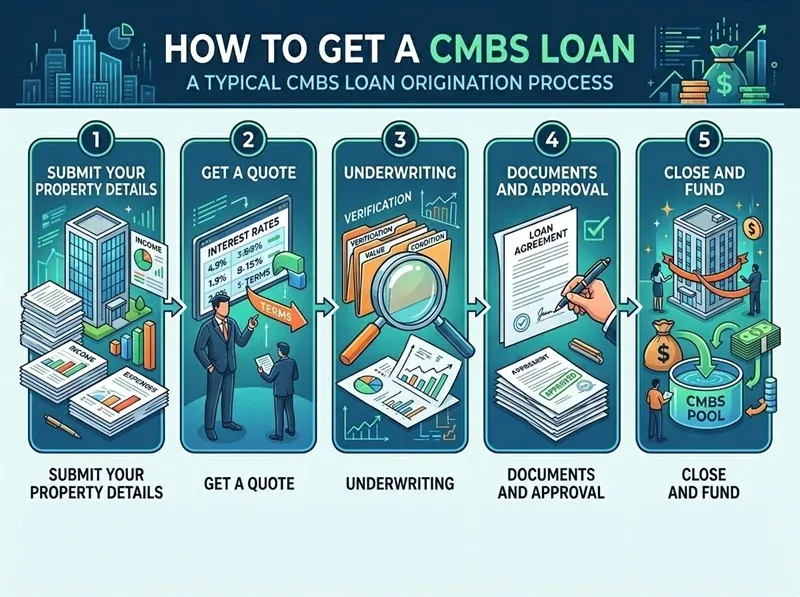

How to Get a CMBS Loan

Wondering how to get a CMBS loan? Here is the typical CMBS loan process and CMBS loan origination process:

- Submit your property details. Share the building's income, expenses, and value.

- Get a quote. The lender provides terms based on the property's cash flow.

- Underwriting. The lender verifies income, value, and condition.

- Documents and approval. You sign the loan agreement and provide all paperwork.

- Close and fund. The loan closes, and later it is pooled and securitized.

Because the property income drives the decision, a building with strong, steady tenants moves through this process most smoothly.

CMBS Loan Prepayment, Defeasance, and Assumption

This is the part many borrowers do not fully understand before they sign, so read it carefully.

Prepayment penalty

CMBS loans usually have a CMBS loan prepayment penalty. Because investors are counting on a fixed stream of payments, you cannot simply pay the loan off early without a cost. Early CMBs loan prepayments are either restricted or expensive, which is one of the biggest trade-offs of this loan type.

Defeasance

To get around the prepayment problem, many CMBS loans use CMBS loan defeasance. Defeasance lets you replace your property as the loan's collateral with a set of securities (usually government bonds) that produce the same payments for the investors. It is a complex process, but it is the standard way to exit a CMBS loan before the term ends.

Can you assume a CMBS loan?

A common question is, can you assume a CMBS loan? Yes, often you can. CMBS loans are frequently assumable, which means a buyer can take over your existing loan and its rate. In a high-rate market, an assumable low-rate CMBS loan can be a real selling point for your property.

CMBS Loan Extensions and Modifications

Markets change, and sometimes borrowers need more time or new terms.

Can you extend a CMBS loan?

People often ask, "Can you extend a CMBS loan?" A CMBS loan extension is possible, but it is not automatic. Because investors own the loan, any CMBS loan extensions must go through the servicer and follow the rules in the loan agreement. Extensions are more common when a loan is maturing and the borrower needs a little more time.

CMBS loan modification

A CMBS loan modification changes the terms of an existing loan, such as the rate, payment, or maturity date. These are handled by the special servicer and usually happen when a borrower is struggling or a loan is at risk. In the news, you may see large real estate owners pursuing modifications and extensions. Searches like "RXR CMBS loan extension" reflect how even big, sophisticated borrowers negotiate new terms when market conditions shift. These are real-world examples of the kind of activity that happens across the CMBS market.

CMBS Loan Defaults, Delinquency, and Workouts

No one likes to think about trouble, but understanding it is part of being a smart borrower.

What happens when a CMBS loan defaults?

So what happens when a CMBS loan defaults? When a borrower stops paying, the loan moves from the master servicer to the special servicer. The special servicer then works on a solution. CMBS loan defaults do not always end in foreclosure. Often the result is a workout instead.

CMBS loan workout

A CMBS loan workout is a negotiated plan to fix a troubled loan. This might include a modification, an extension, or a repayment plan. Specialists known as CMBS loan workout advisors help borrowers and servicers reach a deal. On the servicer side, CMBS loan workout portfolio management teams handle many of these troubled loans at once. The goal of any CMBS loan restructuring is to recover as much value as possible for the bond investors while giving the borrower a realistic path forward.

Delinquency and losses

The industry watches CMBS loan delinquency closely. The cmbs loan delinquency rates and cmbs loan default rates are key signals of how healthy the commercial real estate market is. When borrowers cannot pay, the result can be a cmbs loan loss, and rising cmbs loan losses worry the investors who own the bonds. Before things reach default, a struggling loan is often placed on a CMBS loan watchlist so servicers can monitor it.

CMBS Loan Risks for Commercial Property

Every loan type has trade-offs. The main CMBS loan risks for commercial property include the following:

- Prepayment is hard. Defeasance and penalties make early payoff costly.

- Less flexibility. You deal with a servicer, not a relationship banker.

- Balloon payment. A large amount is due at the end of the term.

- Strict rules. The loan agreement is detailed and not easily changed.

For the right property with steady income, these risks are manageable. But you should understand them before you sign.

How to Track and Look Up CMBS Loans

Because CMBS loans become public bonds, there is a lot of data available about them. Investors and analysts use a CMBS loan lookup or a CMBS loan tracker to follow how specific loans and pools are performing. Industry groups also publish reports. For example, you may see a CREFC update on CMBS loan performance, since CREFC (the CRE Finance Council) is a trade association that tracks the commercial real estate finance market. Staying current with CMBS loan news and the overall CMBS loan market helps borrowers and investors understand where rates and risk are heading. When a loan changes hands, that is known as a CMBS loan sale.

CMBS Loans for Specific Property Types

CMBS loans work for many property types, including office, retail, industrial, multifamily, and hospitality. A hotel CMBS loan is common because hotels often have strong income but can be harder to finance through a traditional bank. The flexibility of CMBS makes it a useful option for these income-producing properties.

Using a CMBS Loan Calculator

Before you commit, run the numbers with a CMBS loan calculator. A good calculator helps you estimate your monthly payment, your balloon payment at the end of the term, and your total cost, including any CMBS loan fees. You plug in the loan amount, interest rate, amortization, and term, and the calculator shows what you will actually owe. If you would like, we can help you run these numbers on a real property.

How CMBS Loan Calculations Work (With a Full Example)

A CMBS loan calculator does a few math steps behind the scenes. Once you understand them, you can size almost any deal yourself. CMBS lenders use three tests to decide how big a loan they will give, and the final loan amount is the smallest figure that passes all three.

The three tests are:

- Loan-to-Value (LTV): the loan compared to the property value.

- Debt Service Coverage Ratio (DSCR): whether the property income covers the loan payments.

- Debt Yield: the property income compared to the loan amount.

Let's walk through each one with a real example.

Example:

- Property value: $5,000,000

- Net Operating Income (NOI): $400,000 per year

- Interest rate: 7.5%

- Amortization: 30 years (360 months)

- Loan term: 10 years (with a balloon payment at the end)

- Maximum LTV: 70%

NOI just means the property's income after operating expenses but before the loan payment.

Step 1: Size the loan by LTV

The formula is simple:

Loan Amount = Property Value x Maximum LTV

Loan Amount = $5,000,000 x 70% = $3,500,000

So based on value alone, the property could support a $3,500,000 loan.

Step 2: Calculate the monthly payment

CMBS loans amortize over a long period, so we use the standard mortgage payment formula:

M = P x [ r (1 + r)^n ] / [ (1 + r)^n - 1 ]

Where:

- M = monthly payment

- P = loan amount ($3,500,000)

- r = monthly interest rate (annual rate divided by 12)

- n = total amortization months

First, find the monthly rate:

r = 7.5% / 12 = 0.625% = 0.00625

n = 30 years x 12 = 360

Plug it in:

M = 3,500,000 x [ 0.00625 x (1.00625)^360 ] / [ (1.00625)^360 - 1 ]

M = 3,500,000 x [ 0.00625 x 9.4216 ] / [ 9.4216 - 1 ]

M = 3,500,000 x 0.0069922

M = $24,473 per month (rounded)

Step 3: Find the annual debt service

This is just the monthly payment times 12:

Annual Debt Service = $24,473 x 12 = $293,676

Step 4: Check the DSCR

DSCR tells the lender if the property earns enough to cover the loan. Most CMBS lenders want at least 1.25x.

DSCR = Net Operating Income / Annual Debt Service

DSCR = $400,000 / $293,676 = 1.36x

A result of 1.36x means the property earns 36% more than it needs to make the payments. This passes the 1.25x minimum, so the deal looks healthy.

Step 5: Check the debt yield

Debt yield is a safety measure that ignores the rate and the loan term. CMBS lenders often want a minimum of about 9% to 10%.

Debt Yield = Net Operating Income / Loan Amount

Debt Yield = $400,000 / $3,500,000 = 11.4%

At 11.4%, this passes too. Since the loan clears all three tests (LTV, DSCR, and debt yield), the lender can approve the full $3,500,000.

Step 6: Calculate the balloon payment

Because the loan amortizes over 30 years but the term is only 10 years, you will still owe a large balance at the end. This is the balloon payment. The formula for the remaining balance is:

Balloon = P x [ (1 + r)^n - (1 + r)^p ] / [ (1 + r)^n - 1 ]

Where p = the number of payments you have made by the end of the term:

p = 10 years x 12 = 120 payments

Plug it in:

Balloon = 3,500,000 x [ 9.4216 - 2.1121 ] / [ 9.4216 - 1 ]

Balloon = 3,500,000 x [ 7.3095 ] / [ 8.4216 ]

Balloon = $3,037,832 (rounded)

So after 10 years of payments, you would still owe about $3,037,832 in one lump sum. At that point, you would typically sell the property, refinance, or pay it off. This balloon is one of the most important things to plan for with any CMBS loan.

Putting it all together:

Item | Result |

Property value | $5,000,000 |

Loan amount (70% LTV) | $3,500,000 |

Interest rate | 7.5% |

Amortization | 30 years |

Monthly payment | $24,473 |

Annual debt service | $293,676 |

DSCR | 1.36x (passes 1.25x minimum) |

Debt yield | 11.4% (passes ~10% minimum) |

Loan term | 10 years |

Balloon payment due at year 10 | $3,037,832 |

This is exactly the kind of math a cmbs loan calculator runs for you in seconds. If you want, send us a property's value and income, and we will run these numbers on your real deal.

A couple of notes: the DSCR (1.25x) and debt yield (9 to 10%) minimums I used common industry benchmarks, not from your product sheet, so adjust them if your underwriting uses different thresholds.

Pros and Cons of a CMBS Loan

Pros | Cons |

Large loan sizes available | Hard and costly to prepay |

Long amortization up to 30 years | Balloon payment at term end |

Fixed, predictable rates | Less flexible than a bank loan |

Property income matters most | Detailed documents and rules |

Often assumable by a buyer | You deal with a servicer, not a banker |

Why Choose Commercial Lending USA for Your CMBS Loan

We aim to make a complex product simple. With our commercial CMBS loan program, you get:

- Competitive fixed rates from 7%

- Loans up to 70% of property value

- Long amortization up to 30 years

- Clear guidance through every step of the process

- Help understanding prepayment, defeasance, and your exit options

If you have a strong income-producing property and want long-term, stable financing, a CMBS loan could be the right fit.

Ready to Explore a CMBS Loan?

A great commercial property deserves the right financing. If you want to learn whether a CMBS loan fits your property, reach out today and we will review your numbers and walk you through your options with no pressure.

Frequently Asked Questions (FAQ)

What does "CMBS Loan" stand for?

CMBS stands for Commercial Mortgage-Backed Securities. So a CMBS loan is a commercial mortgage that backs a bond sold to investors.

What are the typical CMBS loan rates?

Our CMBS loan rates range from 7-8.5%. They are usually fixed for the loan term. Market rates move with the bond market, so always check current pricing before planning a deal.

What are the requirements for a CMBS loan?

You generally need a 680+ credit score, a down payment of up to 30%, strong property income, and full documentation, including bank statements and tax returns. The property's cash flow is the most important factor.

Who is the lender on a CMBS loan?

At first, the lender is the bank or finance company that originates the loan. After it is securitized, the real owners are the bond investors, and a master servicer handles your payments. A special servicer steps in only if the loan has problems.

Can you pay off a CMBS loan early?

Usually not without a cost. CMBS loans typically have a prepayment penalty, and the standard way to exit early is defeasance, which replaces your property with securities that pay the investors instead.

Can you assume a CMBS loan?

Yes, CMBS loans are often assumable, meaning a buyer can take over your loan and its existing rate. This can be a strong selling point when market rates are higher than your loan rate.

Can you extend a CMBS loan?

A CMBS loan extension is possible but not automatic. Any extension must go through the servicer and follow the loan agreement. Extensions often come up when a loan is reaching maturity.

What happens when a CMBS loan defaults?

The loan moves to a special servicer, who tries to find a solution. This is called a workout and may include a modification, an extension, or a repayment plan. Default does not always lead to foreclosure.

What is the minimum CMBS loan size?

Many lenders set a minimum around $2 million because the cost of pooling and securitizing very small loans is high. Larger, income-producing properties are the best fit.

How do I get a CMBS loan?

Submit your property's income and value, get a quote, go through underwriting, sign the loan documents, and close. Because the decision is based on the property's cash flow, a building with strong, steady tenants moves through the process most easily.

Disclaimer: Loan terms, rates, and requirements shown here are based on our current programs and may change. CMBS market rates and performance data move constantly. All loans are subject to approval and underwriting. This article is for general information only and is not financial, legal, or investment advice.

0 Comments

Leave A Comment