DSCR Loan Rates in 2026: Current Rates, Best Rates, and How to Get Them

If you invest in real estate, DSCR loan rates are one of the most important numbers you will ever look at. A DSCR loan lets you qualify based on a property's rental income instead of your personal income, which makes it one of the best tools for building a rental portfolio. But the rate you pay decides how much profit you keep.

This guide gives you the current dscr rates for 2026, explains what a good DSCR ratio is, shows you what drives your rate up or down, and tells you exactly how to get the best dscr loan rates on your next deal.

What are DSCR loans?

What Is a DSCR Loan?

DSCR stands for Debt Service Coverage Ratio. A DSCR loan is a real estate investment loan that qualifies you based on whether the property's income covers its loan payment, not based on your tax returns. It's a way for commercial real estate investors to get money.

The math is simple. The lender divides the property's income by its loan payment. If the property earns more than it costs to carry, it "covers" the debt, and you can qualify. This is why DSCR loans are so popular with investors who own several properties or who write off a lot of income on their taxes.

Why are DSCR loans relevant?

DSCR loans have several benefits for people who invest in business real estate, including:

- Qualify based on property cash flow: People who own properties that bring in a lot of cash can get DSCR loan rates even if their income doesn't meet the usual loan standards.

- Building Portfolio: For first-time investors who may need a high personal income but have found good investment homes, DSCR loans can be helpful.

What Are DSCR Loan Rates Today?

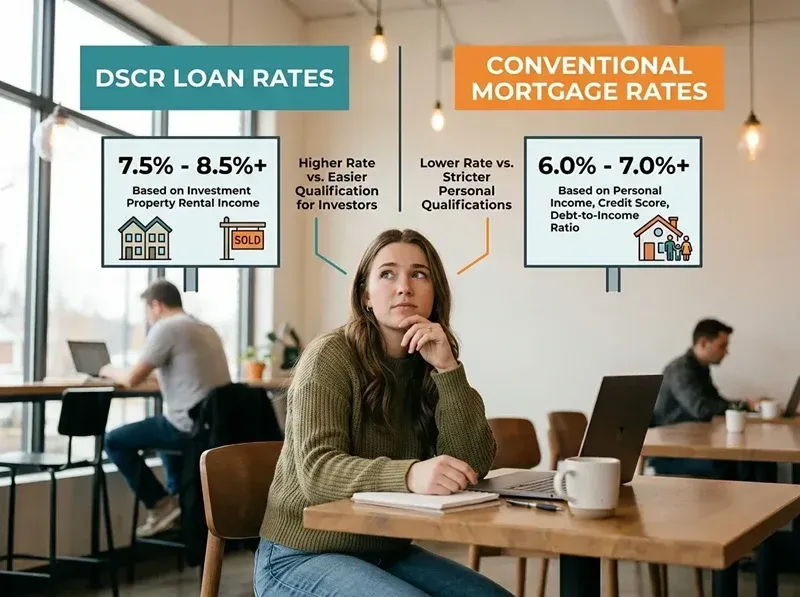

Investors searching for DSCR loan rates today want a real number, so here is the current picture. As of mid-2026, DSCR loan interest rates for residential investment properties generally range between roughly 6.5% and 8.75%, while commercial DSCR loans typically run higher, from about 7.25% to 10.75%, depending on the deal. The strongest borrowers get the lowest rates. In mid-2026, the best pricing tier sat around 6.50% to 7.25%, standard files around 7% to 8%, and weaker files higher.

Source: REI News NowDscrcapitalpartners

For comparison, the Freddie Mac weekly 30-year fixed average was about 6.53% in June 2026, and DSCR loans usually price a little above that because they are investment-property loans.

Here is a simple snapshot of where DSCR loan interest rates sit in 2026:

Borrower profile | Typical DSCR rate range (2026) |

Strongest (740+ credit, 1.25+ DSCR, 30%+ down) | About 6.5% to 7.25% |

Standard files | About 7% to 8% |

Weaker files (lower credit or higher LTV) | About 8% to 9.25% |

Commercial DSCR loans | About 7.25% to 10.75% |

Remember, rates move with the bond market and can change daily, so always confirm a live quote before you plan a deal.

Commercial Lending USA DSCR Loan Rates

At Commercial Lending USA, our current DSCR mortgage rates are competitive with the best tiers in the market:

Program | Interest Rate | Max LTV | Min Down | Term | Minimum Credit |

DSCR Loan (Residential) | 6.5% to 7.5% | Up to 80% | 20% | Up to 30 years | 660+ |

DSCR Loan (Commercial) | 8% to 9% | Up to 75% | 25% | Up to 30 years | 680+ |

Both programs qualify based on the property's cash flow, and neither requires tax returns or bank statements. Because we work as a correspondent lender with a network of capital partners, we shop your file across multiple sources to find you the best DSCR rates available for your specific deal.

DSCR Loan Rates vs Conventional Mortgage Rates

A common question is how DSCR rates compare to a normal mortgage. DSCR loans usually cost a little more because the lender is underwriting the property's income instead of your personal income. DSCR loans typically run about 0.75% to 1.5% above conventional investment property loan rates. That small premium buys you something valuable: you can qualify without showing personal income, and you can keep buying properties without your debt-to-income ratio getting in the way. For most serious investors, that flexibility is worth far more than the difference in rate.

What Is a Good DSCR Ratio?

Many borrowers ask, "What is a good DSCR ratio?" or "How much should their DSCR be?" Here is the simple answer.

- A DSCR of 1.0 means the property's income exactly equals its loan payment.

- A DSCR above 1.0 means the property earns more than it costs to carry.

- Most lenders want a DSCR of around 1.25 to qualify, though some programs allow lower.

So what should the average DSCR be? Aim for 1.25 or higher. That is the level most lenders see as healthy, and it usually unlocks better pricing. Borrowers who want the best DSCR rates should aim for a ratio above 1.25x. Some lenders will still work with you below 1.0 using larger down payments or no-ratio programs, but your rate will be higher.

The takeaway: the higher your DSCR, the lower your risk to the lender, and the better your rate.

What Affects Your DSCR Loan Rate?

Your final rate is not random. These are the main factors that move it:

Factor | How it affects your rate |

DSCR ratio | A higher ratio (1.25+) means a lower rate |

Credit score | 700+ unlocks much better pricing |

Down payment / LTV | 25% to 30% down usually gets the best tier |

Property type | Single-family homes price better than multi-unit or short-term rentals |

Loan term and prepay | Different terms and prepayment options carry different rates |

Lender | Every lender prices differently, so it pays to compare |

Most of these work together. A borrower with a high DSCR, strong credit, and a larger down payment will see the lowest DSCR loan rate, while a weaker file on every factor will see the highest.

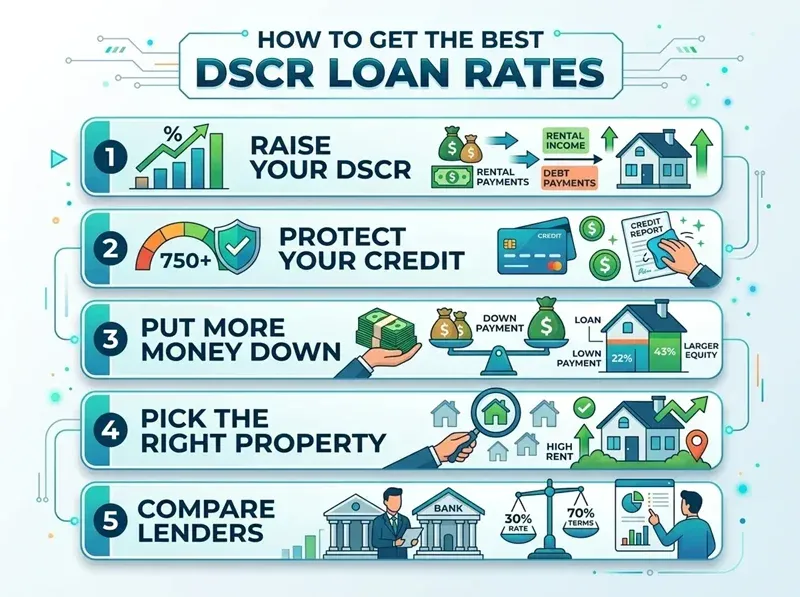

How to Get the Best DSCR Loan Rates

Want to compare DSCR loan rates and land the lowest one? Focus on the things you can control:

- Raise your DSCR. Increase rental income or lower the loan amount so the property covers its payment more comfortably.

- Protect your credit. A higher score moves you into a better pricing tier.

- Put more money down. A bigger down payment lowers the lender's risk and your rate.

- Pick the right property. Clean, well-leased single-family rentals usually price best.

- Compare lenders. This is the big one. Rates vary a lot between lenders, so shopping your file is the fastest way to save.

Who Has the Best DSCR Loan Rates?

When investors ask who has the best DSCR rates or who the best DSCR lenders are, the honest answer is that no single lender always wins. Pricing shifts constantly, and the best rate depends on your exact file.

That is why working with a broker helps. As a commercial mortgage broker and correspondent lender, Commercial Lending USA compares your deal across many capital partners at once, so you do not have to apply to lender after lender yourself. We can compare options, push for better pricing on your behalf, and handle the paperwork. For most borrowers, that is the simplest path to the best rates on DSCR loans.

What a Commercial Mortgage Broker Knows

It can take a lot of work to determine how to get the best rates on DSCR loans. This is where a business mortgage broker like Commercial Lending USA can come in handy. They know a lot about the market for DSCR loans and can:

Compare different lenders: Because they work with many loans, your chances of getting the best rate increase.

Negotiate on your behalf: Because they have done this before, they can speak up for you and possibly get you a lower interest rate.

Make the process easier: They can handle many forms and talk to lenders, saving you time and work.

Work with a commercial mortgage broker to get a good DSCR ratio. This will help you get the best DSCR loan rate for your commercial real estate investment.

How Often Can You Get a DSCR Loan?

A great feature of DSCR loans is that there is no real limit on how many you can have. Because you qualify on each property's income rather than your personal income, you can finance one property after another. This is what makes DSCR loans so powerful for scaling a rental portfolio. As long as each new property cash flows, you can keep going.

A Quick DSCR Example

Let's say you have a rental property like this:

Item | Amount |

Monthly rental income | $2,500 |

Monthly loan payment (PITIA) | $2,000 |

The DSCR is simply income divided by payment:

DSCR = $2,500 / $2,000 = 1.25

A DSCR of 1.25 means the property earns 25% more than its payment. That hits the level most lenders want, so this deal would likely qualify and price well.

Why Choose Commercial Lending USA for Your DSCR Loan

We make DSCR financing simple, fast, and competitive. With us, you get:

- Competitive DSCR rates starting at 6.5%

- Up to 80% LTV on residential investment properties

- Terms up to 30 years

- No tax returns and no bank statements

- A network of capital partners working to find you the best rate

- In-house underwriting to speed up your approval

Commercial Lending USA is a member of the American Association of Private Lenders and is BBB accredited, so you are working with a trusted partner.

Ready to Get Your Best DSCR Rate?

The fastest way to find out your real rate is to get a personalized quote. Reach out to Commercial Lending USA today, and we will review your property, compare your options, and help you lock in a competitive DSCR loan rate. Call (855) 365-9200 or apply online to get started.

FAQs

What is the interest rate on a DSCR loan?

As of 2026, DSCR loan rates for residential investment properties generally range from about 6.5% to 8.75%, and commercial DSCR loans run higher. Our current DSCR rates start at 6.5% for residential and 8% for commercial. Your exact rate depends on your DSCR ratio, credit score, and down payment.

What are DSCR rates today?

DSCR rates today sit in the high 6% to 9% range for most residential borrowers, with the strongest files reaching the high 6s or low 7s. Rates change daily with the bond market, so contact us for a live quote.

What is a good DSCR ratio?

A good DSCR ratio is 1.25 or higher. At that level, the property earns at least 25% more than its loan payment, which most lenders view as healthy and which usually earns you a better rate.

Who has the best DSCR loan rates?

No single lender always has the best rate, because pricing changes constantly and depends on your file. Working with a broker like Commercial Lending USA lets you compare many lenders at once to find the best rate for your specific deal.

Are DSCR loan rates higher than conventional rates?

Usually yes, by about 0.75% to 1.5%. The slightly higher rate reflects that the loan is underwritten on the property's income rather than your personal income, but the trade-off is far easier qualification.

How can I get the best DSCR rate?

Aim for a DSCR above 1.25, keep your credit strong, put down 25% to 30%, choose a well-leased property, and compare lenders. Each of these helps move you into a better pricing tier.

How is a DSCR loan rate calculated for my deal?

Lenders look at your DSCR ratio, credit score, loan-to-value, property type, loan term, and prepayment choice, then price your rate off the current market. A stronger profile on each factor means a lower rate.

How often can I get a DSCR loan?

There is no set limit. Since you qualify on each property's cash flow, you can finance many properties over time, which makes DSCR loans ideal for growing a rental portfolio.

Do DSCR loans require tax returns or income verification?

No. Our DSCR loans qualify based on the property's rental income, with no tax returns and no bank statements required.

How do I contact Commercial Lending USA?

Call (855) 365-9200, email sales@commerciallendingusa.com, or apply online for a personalized DSCR loan quote.

Disclaimer: DSCR loan rates and terms shown here are based on current programs and market conditions as of 2026 and may change at any time. Market rates move daily. All loans are subject to approval and underwriting. This article is for general information only and is not financial or legal advice.

0 Comments

Leave A Comment