DSCR Loan Requirements for Commercial Property Investors

DSCR loans have become one of the most popular financing options for real estate investors in 2026 because they let you qualify based on the property’s rental income instead of your personal tax returns or W-2s.

At Commercial Lending USA, we close DSCR loans weekly for both residential rental properties (1–4 units) and commercial investment assets. This complete 2026 guide breaks down the exact DSCR loan requirements, including minimum DSCR ratio, credit score, LTV, down payment, cash reserves, property eligibility, documentation, and how to qualify fast.

What Is a DSCR Loan?

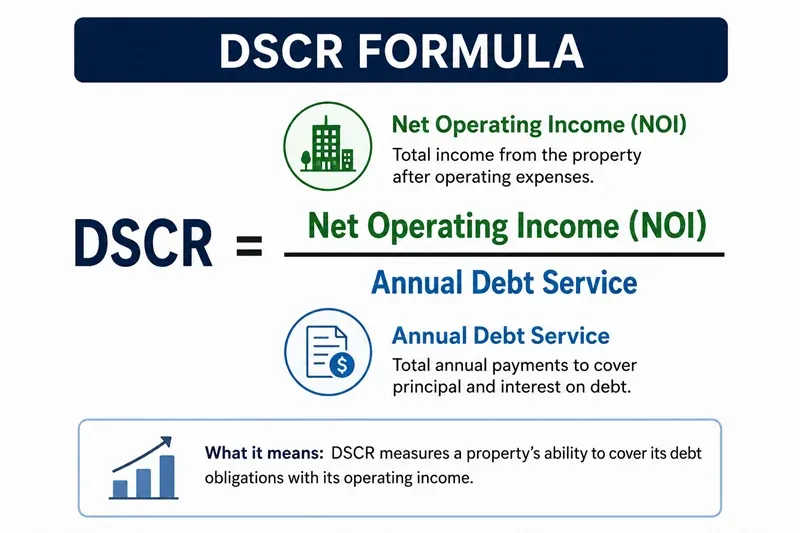

DSCR stands for Debt Service Coverage Ratio. It measures whether the property’s net operating income (NOI) is sufficient to cover the monthly mortgage payment.

Unlike traditional mortgages, DSCR lenders do not review your personal income, tax returns, W-2s, or employment history.

Instead, qualification is based entirely on the property’s rental cash flow. Lenders simply ask: “Does this property generate enough rent to pay its own mortgage?”

They answer this question by calculating the DSCR.

Lenders typically require a minimum DSCR of 1.0x–1.25x.

- 1.0x = The property’s income exactly covers the debt payment.

- 1.25x = The property generates 25% more income than needed, giving the lender a safety buffer.

How to Calculate Your DSCR (Step-by-Step Example)

- Add up monthly rental income

- Subtract vacancy and operating expenses → get Net Operating Income (NOI)

NOI = (Gross Rental Income + Other Income - Vacancy) - Operating Expenses - Divide NOI by your proposed monthly mortgage payment

Example:

A 4-unit residential property generates $8,000/month in rent. After 10% vacancy and expenses, NOI = $6,500/month ($78,000/year).

Proposed monthly debt service = $5,200.

DSCR = $78,000 ÷ ($5,200 × 12) = 1.25x → Qualifies easily.

Current DSCR Loan Rates 2026

As of May 2026, here are the rates we are closing daily:

- DSCR Residential: 6.5–7.5%

- DSCR Commercial: 8–9%

Rates are fixed for 30-year terms and move with the 10-year Treasury. Higher credit, stronger DSCR, and larger down payments = best pricing.

The Scoring Breakdown:

- DSCR of 1.25+: The property is highly profitable, generating 25% more rent than the mortgage cost. This unlocks the lowest interest rates and highest leverage.

- DSCR of 1.00: The property breaks even. The rent exactly covers the mortgage.

- DSCR below 1.00: The property operates at a monthly loss. Most lenders will reject this, though some specialized "no-ratio" programs allow it if the borrower puts down a massive down payment.

Traditional Loan vs. DSCR Loan

Feature | Traditional Mortgage (Conforming) | DSCR Loan (Non-QM/Investor) |

Qualification Focus | Your personal salary, debt-to-income (DTI) ratio, and job history. | The property’s rental income and market viability. |

Required Income Docs | 2 years of tax returns, W-2s, and recent paystubs. | None. No tax returns or personal financial statements required. |

Approval Speed | Slow (typically 45–60 days due to manual underwriting). | Fast (typically 21–30 days due to streamlined asset qualification). |

Down Payment | Can be as low as 3%–5% for primary homes. | A minimum 20% to 25% down payment is required. |

Interest Rates | Standard market consumer rates. | Generally 1% to 2% higher than standard conventional loans. |

Current DSCR Loan Requirements 2026 (Residential vs Commercial)

From our latest loan products and terms summary (updated May 2026):

Requirement | DSCR Residential | DSCR Commercial |

Interest Rate Range | 6.5–7.5% | 8–9% |

Max LTV | Up to 80% | Up to 75% |

Minimum Down Payment | 20% | 25% |

Minimum DSCR Ratio | 1.0–1.25x | 1.0–1.25x |

Loan Term | 30 years | 30 years |

Minimum Credit Score | 660+ | 680+ |

Documentation | Rental income only | Rental income + light docs |

Bank Statement / Tax Return | Not required | Not required |

Cash Reserves Requirements for DSCR Loans 2026

Most DSCR lenders require 3–6 months of PITIA reserves (Principal, Interest, Taxes, Insurance, and Association dues) after closing.

- Stronger profiles (DSCR ≥ 1.25x + 700+ credit) → often 3 months

- Standard profiles → 6 months

- Some programs allow 0–3 months with higher down payment or compensating factors

Pro Tip: Cash reserves are one of the easiest ways to strengthen a borderline DSCR file.

Property Type Eligibility for DSCR Loans

Property Type | Eligible? | Max LTV | Notes |

Single-Family Residence | Yes | 80% | Most common |

2–4 Unit Residential | Yes | 80% | Strongest segment |

Condos / Townhomes | Yes | 75–80% | Warrantable condos only |

Small Commercial (5+ units) | Limited | 75% | Use our DSCR Commercial program |

Mixed-Use | Case-by-case | 75% | Must be primarily residential |

Note: DSCR loans are strictly for investment / rental properties, not primary residences.

DSCR Loan Documentation Checklist (What Lenders Actually Need)

Most DSCR programs are designed to be light on paperwork. Here’s exactly what you’ll need:

- 2–3 months of bank statements (to verify reserves)

- Current rent rolls and lease agreements

- Property appraisal with 1007 rent schedule (for residential) or market rent analysis (for commercial)

- Credit report

- Proof of property insurance and reserves

- Entity documents (if purchasing in an LLC or partnership)

No personal tax returns, W-2s, or full financial statements are required on most programs.

DSCR Loan Requirements

What is the Debt Service Coverage Ratio (DSCR)?

Lenders use the Debt Service Coverage Ratio (DSCR) as a primary way to determine if a commercial property loan will work. In this case, it looks at how much money a property can make to cover its debts, like the monthly mortgage payment.

Minimum DSCR Loan Requirements

Commercial property loans usually have a DSCR of around 1.25. Still, the minimum requirement can be different based on several factors, such as:

Loan Type

SBA Loans: The DSCR standards for these government-backed loans may be slightly lower, starting at 1.10.

Property Type

Higher-risk properties: Lenders may need a higher DSCR (e.g., 1.40 or more) for properties in less established markets or with a higher chance of vacancies.

Lower-risk properties: Properties in significant areas or with stable tenants may get by with a slightly lower DSCR (1.20).

Lender

There are different risk tolerances and underwriting rules for each loan. If the borrower has a lot of experience and a good loan package, some lenders may be more flexible with their DSCR standards.

DSCR Loan vs Other Financing Options (2026)

Loan Type | Qualify On | Closing Speed | Prepayment Penalty | Best For |

DSCR Loan | Rental income only | 15–30 days | None | Investment rentals |

Traditional Bank | Personal income + DSCR | 45–120 days | Varies | Long-term stabilized hold |

SBA 7(a)/504 | Full tax returns | 45–90 days | Penalty, Yes (early years) | Owner-occupied businesses |

Fannie Mae / Freddie Mac | Strong DSCR + full docs | 30–45 days | Low after lock | Large stabilized multifamily |

Bridge / Hard Money | Asset value | 7–21 days | None | Fix-and-flip / short-term |

Pro Tip: Many investors start with a DSCR loan, then refinance into a Fannie Mae or Freddie Mac permanent loan once the property is fully stabilized for even lower rates.

How to Improve Your DSCR Ratio (and Get Approved Faster)

- Increase rental income (raise rents or add short-term rental income)

- Lower the proposed loan amount (larger down payment)

- Reduce operating expenses

- Choose a longer amortization or interest-only option (if available)

- Add cash reserves or a co-borrower with strong credit

Even a small improvement from 0.95x to 1.10x can make the difference between denial and approval.

Who Should Get a DSCR Loan in 2026?

Perfect for:

- Real estate investors buying rental properties

- Borrowers with complex tax returns or self-employed income

- Anyone who wants to avoid personal income verification

- Residential (1–4 units) or small commercial investment deals

Better alternatives if:

- You need to close in under 15 days → Bridge or Hard Money

- Credit score below 660 → Hard money loans or No-Doc programs

- Property is owner-occupied → SBA or conventional bank loan

How to Qualify for a DSCR Loan – Step-by-Step

- Pre-qualify in minutes – Submit property address, purchase price, and estimated rents

- Provide rent rolls & leases

- Get appraisal & 1007 rent schedule

- Review credit & reserves

- Receive term sheet & close in 15–30 days

Ready to check your DSCR loan eligibility?

Tell us about your rental property or upcoming investment deal, and we’ll run numbers across DSCR, Fannie Mae, Freddie Mac, Bridge, and all 26 programs in minutes, with no obligation and same-day pre-approval available.

Beyond DSCR: Additional Commercial DSCR Loan Requirements

Even though DSCR is essential, getting a commercial DSCR loan comes with extra requirements made by lenders to keep risk in check. Here is a list of some basic requirements:

Loan-to-Value (LTV) Ratio

The LTV ratio checks how much the loan is compared to how much the property is worth. Lenders usually need a lower LTV (around 75–80%) for DSCR loans than regular ones. A significant down payment will lower the lender's danger.

Credit Score

It is better to have a credit score of at least 680 to get a DSCR loan than for most other loans. A good credit score shows you know how to handle debt and are careful with your money.

Down Payment

DSCR loans usually need a more significant down payment (20-30%) than regular loans because they focus on how the property will make money. This lowers the risk for the lender because they don't have to give as much money.

Property Type

You can only get a DSCR loan for some commercial property. Lenders usually want to lend money on homes that can consistently bring in money and have low vacancy rates. Office buildings, stores, warehouses, and multifamily flats are all eligible property types.

Experience

The amount of knowledge an investor has about commercial properties can significantly affect the approval of a DSCR loan. Suppose a borrower has a history of managing properties well and making money. In that case, lenders may be more flexible with their DSCR or LTV standards. On the other hand, new investors may have to meet stricter standards or find a co-signer with more experience.

Why Choose Commercial Lending USA for Your DSCR Loan?

To get through the complicated world of DSCR loans, you need an investor with a lot of knowledge and experience. There are a few main reasons why Commercial Lending USA stands out:

In-House Underwriting Expertise

Our team knows much about DSCR loans and can quickly get through the approval process. This can make your application easier and speed up the loan acceptance process.

Correspondent Lender and Superbroker Advantage

Commercial Lending USA doesn't just give loans from one lender. They can connect you with a vast network of lenders and loan programs because they are both an associate lender and a superbroker. This lets them find the best rates and terms for your needs, which increases your chances of getting the best DSCR loan possible.

Beyond DSCR Loans

We know a lot more than just DSCR loans. A traditional loan with a minor DSCR requirement or a different loan structure would be better for you. That being the case, we can also look into those choices. We want to help you get the money you need to reach your goals in the best way possible.

Conclusion

To get a commercial DSCR loan, you must know how much the property could make. A DSCR that satisfies or exceeds the lender's requirements, typically around 1.25, can demonstrate this. In addition to DSCR, lenders also look at loan-to-value ratio (LTV), which is generally lower for DSCR loans at 75-80%; credit score, which is usually higher at 680 or above; and down payment, which is typically between 20 and 30%.

Refrain from handling DSCR loans by yourself. Get a free consultation from Commercial Lending USA or call us (571) 544-6600 today and determine which DSCR loan option will help you reach your commercial property goals.

FAQs

Q: What are the DSCR loan requirements in 2026?

Minimum DSCR ratio of 1.0–1.25x, credit score 660–680+, 20–25% down payment, and qualification based on rental income only.

Q: Do I need tax returns for a DSCR loan?

No. Most DSCR programs do not require personal or business tax returns.

What is a good DSCR ratio for loan approval?

1.25x or higher gets you the best rates and highest LTV. Anything above 1.0x can still qualify.

Q: Are DSCR loans available for commercial properties?

Yes, we offer both DSCR Residential (up to 80% LTV) and DSCR Commercial (up to 75% LTV).

Q: Can I get a DSCR loan with a 650 credit score?

Residential DSCR starts at 660+. Lower scores are better served with our Hard Money or No-Doc programs.

Q: What is a DSCR loan?

A DSCR (Debt Service Coverage Ratio) loan is a financing option for commercial properties that prioritizes the property's cash flow potential over the borrower's income.

Q: What are the benefits of DSCR loans?

DSCR loans have these pros:

You can only qualify if you show proof of your regular income.

Do not mix commercial loans with personal money.

Q: What is a decent DSCR for a business loan?

The average rate on commercial loans is about 1.25, but it can differ for each loan type, property type, and lender.

Q: Besides DSCR, what else do lenders consider?

Lenders also consider factors like loan-to-value ratio (LTV), credit score, down payment, and property type.

Q: How can I get started with a DSCR loan?

Contact Commercial Lending USA for a free consultation and pre-qualify for the best DSCR loan option for you.

0 Comments

Leave A Comment