Renovation Loans for Investment Property: The Complete Investor's Guide

Buying an investment property is only half the battle. Many of the best deals are houses that need work, and that means you need money for both the purchase and the repairs. A regular bank usually will not hand you cash for renovations, and it certainly will not move fast enough to win a competitive deal.

That is where renovation loans for investment property come in. These loans are built for investors who want to buy a property, fix it up, and either sell it for a profit or rent it out. In this complete guide, we will explain what these loans are, how they work, the rates and requirements, how much you can borrow, and how to use them for both flips and rentals.

What Is a Renovation Loan for an Investment Property?

A renovation loan is short-term financing that covers the cost of buying a property plus the cost of fixing it up. Unlike a normal mortgage, an investment property renovation loan is designed around the future value of the property, not just what it is worth today.

This is the key idea. A traditional bank loan looks at the home as it sits right now. A rehab loan for investment property looks at what the home will be worth after the repairs are done, which is called the After-Repair Value, or ARV. Because the lender can see the bigger picture, you can often borrow enough to cover both the purchase and the renovation.

These are usually funded by private lenders rather than big banks. A private money renovation loan moves faster and has simpler rules, which is exactly what investors need when a good deal will not wait.

How Do Renovation Loans for Investment Property Work?

Here is how these loans work, step by step:

- You find a property. Ideally one you can buy below market value and improve.

- You apply. You share the property details, your purchase price, and your repair budget.

- The lender reviews the deal. They look at the purchase price, the repair plan, and the ARV.

- You get approved and close. You receive funds to buy the property.

- You draw on the rehab budget. The repair money is usually released in stages as the work gets done.

- You finish the project. Then you either sell the property or refinance it into a long-term rental loan.

Because a hard money renovation loan is short-term, you are not stuck with it for years. You use it to buy and fix, then you exit by selling or refinancing.

Types of Renovation Loans for Investors

Not every project is the same. A simple cosmetic update is very different from a full gut renovation. Here are the main renovation loans for investment property we offer, side by side:

Feature | Fix and Flip Loan | Construction / Heavy Rehab Loan | Bridge Loan |

Interest rate | 10-11% | 10-11% | 9-12% |

LTV (max) | Up to 85% on purchase | Up to 70% | Up to 70% |

LTC (max) | Up to 80% of rehab | Up to 75% | N/A |

ARV | Up to 70% | Up to 65% | N/A |

Down payment | 20% | 25% | 30% |

Loan term | Up to 12 months | 12-24 months | 12-36 months |

Credit score | 660+ | 660+ | 620+ |

Best for | Cosmetic to moderate flips | Major or structural renovations | Flexible short-term needs |

Fix and Flip Loan

This is our most popular renovation loan for investors. It covers up to 85% of the purchase and up to 100% of the rehab budget. It is perfect for a renovation loan for flipping houses, whether you plan to sell at the end or refinance into a rental. Best of all, flipping experience is not required.

Construction and Heavy Rehab Loan

If your project is bigger, such as a gut renovation or structural work, a construction renovation loan for investors gives you more time, up to 24 months. It is built for major projects where the property needs serious work before it is ready.

Bridge Loan

A bridge loan is a flexible short-term renovation loan that helps you move quickly. It is useful when you need fast financing and a longer runway of up to 36 months to complete and exit your project.

Our Renovation Loan Terms at a Glance

Here are the full terms of our main renovation loan, the Fix N' Flip Private Lender program:

Feature | Our Renovation Loan |

Interest rate | 10-11% |

LTV (Loan-to-Value) | Up to 85% on the purchase |

Rehab funding (LTC) | Up to 100% of the renovation budget |

ARV (After-Repair Value) | Up to 70% |

Minimum down payment | 20% |

Loan term | Up to 12 months |

Minimum credit score | 660+ |

Tax returns | Not required |

Bank statements | Not required |

Experience | Not required |

The fact that we can fund up to 100% of the renovation budget is a big deal. It means you may only need cash for the down payment, while the repairs are covered by the loan.

Renovation Loan Rates: What to Expect

Our renovation loan rates sit in the 10-11% range for fix-and-flip projects and 9-12% for bridge loans. These rehab loan rates are higher than a standard mortgage, and that is normal for short-term investor financing.

Here is why higher rates still make sense. These loans are fast and flexible, and they fund your repairs. You only pay that rate for a few months while you complete the project, not for 30 years. For most investors, speed and access to rehab money matter far more than the rate itself.

How Much Can You Borrow? Understanding LTV, LTC, and ARV

To understand a loan to renovate investment property, you need to know three quick terms:

- LTV (Loan-to-Value): how much you can borrow against the purchase price. Ours goes up to 85%.

- LTC (Loan-to-Cost): how much of your renovation cost is covered. Ours goes up to 100%.

- ARV (After-Repair Value): the value of the property once repairs are done. We lend up to 70% of the ARV.

The lender uses all three to decide your loan amount, and the final number is capped so it stays safe for everyone. This is sometimes called an after repair value loan because the ARV is so important.

A simple example

Let's say you find a property like this:

Item | Amount |

Purchase price | $200,000 |

Renovation budget | $50,000 |

After-Repair Value (ARV) | $320,000 |

With our program:

- Loan toward purchase (85% of $200,000) = $170,000

- Rehab funding (100% of $50,000) = $50,000

- Your down payment (the rest of the purchase) = about $30,000

The ARV check makes sure the total loan stays under 70% of $320,000, which is $224,000. In this example the loan fits comfortably, so the deal works. Always run your own numbers before you commit.

Using a Renovation Loan for a Rental Property: The BRRRR Method

Renovation loans are not just for flipping. Many investors use them to build a rental portfolio with a strategy called BRRRR, which stands for Buy, Rehab, Rent, Refinance, Repeat.

Here is how a renovation loan for rental property fits into BRRRR:

- Buy the property with a renovation loan.

- Rehab it using the rehab budget.

- Rent it out to a tenant.

- Refinance into a long-term loan, such as a DSCR loan, to pay off the renovation loan.

- Repeat the process with your next property.

Our DSCR loan is a great exit for this. It offers rates of 6.5-7.5%, up to 80% LTV, and terms up to 30 years, and it qualifies based on the rental income, not your tax returns. This makes the full BRRRR cycle possible under one roof.

Renovation Loan Requirements

The renovation loan requirements for our program are simple:

- A credit score of 660 or higher

- At least a 20% down payment

- A clear renovation plan and budget

- A property with a strong After-Repair Value

You do not need tax returns or bank statements, and you do not need past experience. That makes qualifying far easier than with a traditional bank.

How to Qualify Quickly

To get approved fast, come prepared with:

- The property address and purchase price

- Your renovation budget and scope of work

- Your estimated After-Repair Value

- Proof of your down payment funds

Because we skip tax returns and bank statements, the process moves quickly. The clearer your numbers, the faster we can say yes.

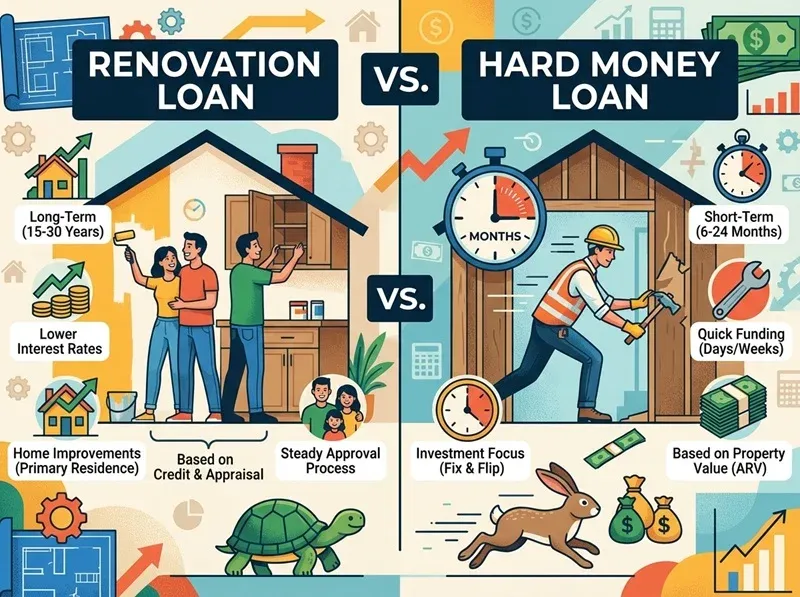

Renovation Loan vs Hard Money Loan

People often ask about the difference between a renovation loan and a hard money loan. The truth is that most renovation loans for investors are a type of hard money loan. The renovation version is simply built to fund repairs as well as the purchase.

If your project is a clear buy, fix, and exit deal, our Fix and Flip renovation loan is usually the best fit. If your credit is lower or your deal is unusual, our general hard money loan accepts credit scores of 500+ and may still get you funded.

Pros and Cons of Renovation Loans for Investment Property

Pros | Cons |

Funds both purchase and repairs | Higher rate than a standard mortgage |

Fast approval and funding | Short repayment window |

No tax returns or bank statements | You need a clear exit plan |

Based on future ARV, not current value | Best for short-term projects |

Experience not required | Requires a solid renovation budget |

Why Choose Us for Your Renovation Loan

We aim to be the easy, reliable choice for investors who want to buy and improve property. With us, you get:

- Up to 85% of the purchase price.

- Up to 100% of your renovation budget.

- No tax returns and no bank statements.

- No experience required.

- A clear path to refinance into a rental loan if you want to hold.

Whether you are flipping your first house or building a rental portfolio, our renovation loans are built to help you move fast and grow.

Ready to Fund Your Next Project?

The best investment deals do not wait around. If you are ready to buy, renovate, and profit, our renovation loan program is built to fund you quickly. Reach out today and we will review your numbers with no pressure.

Frequently Asked Questions (FAQ)

What is a renovation loan for an investment property?

It is short-term financing that covers both the purchase of an investment property and the cost of fixing it up. Unlike a bank loan, it is based on the after-repair value of the property, so you can borrow enough to complete the whole project.

How do renovation loans for investment property work?

You apply with your property and repair plan, the lender reviews the deal and the after-repair value, you close and buy the property, and you draw on the rehab budget as the work is done. When the project is finished, you sell or refinance to pay off the loan.

What are the interest rates for an investment property renovation loan?

Our renovation loan rates are 10-11% for fix and flip projects and 9-12% for bridge loans. They are higher than a standard mortgage because they are short-term and they fund your repairs.

Can I get a renovation loan with no income verification?

Yes. Our renovation loan does not require tax returns or bank statements. We focus on the property, the repair plan, and the after-repair value instead of your personal income documents.

How much can I borrow for renovations on an investment property?

We can fund up to 85% of the purchase price an

0 Comments

Leave A Comment