Fix and Flip Hard Money Loans: A Complete Investor Guide

Flipping a house can be one of the fastest ways to grow money in real estate. You buy a property below market value, fix it up, and sell it for a profit. Simple, right? Well, there is one big problem most flippers run into: cash. You find a great deal, the clock is ticking, and a regular bank takes weeks (or even months) to say yes. By then, the deal is already gone to someone else.

This is exactly why fix and flip hard money loans exist. They are built for speed, built for investors, and built around the property, not just your paycheck. In this complete guide, we will explain everything in plain English: what these loans are, how fix and flip loans work, what they cost, how to compare lenders, and how you can use one to flip your next house with confidence.

What Is a Fix and Flip Hard Money Loan?

A fix and flip loan is short-term funding used to buy a property, fix it up, and sell it for a profit. Most of these are funded by hard money fix and flip lenders instead of big banks.

The phrase "hard money" simply means the loan is based on a "hard asset", the property itself. So hard money lenders for house flipping care more about the deal and the after-repair value of the home than about your tax returns or pay stubs. If the deal is strong, the loan usually works.

For us, this is our Fix N' Flip Private Lender program. It is designed so real estate investors can move quickly and grab good deals before anyone else. We act as a fix and flip private money lender, which means we lend our own private capital. There is no slow committee, no endless wait. Decisions are fast.

Who is this loan for?

- First-time flippers who found a good deal but can't get a bank loan

- Experienced investors who want to move fast and do several flips a year

- Buyers who need money for both the purchase and the repairs

- People with self-employed income who don't have clean tax returns or pay stubs

How Fix and Flip Loans Work (Step by Step)

Here is the simple version of how to fix and flip with hard money lenders:

- Find a deal. You locate a property that you can buy, repair, and sell for more than your total cost.

- Apply for the loan. You send us the property details and your project plan.

- Get approved fast. We focus on the property value and the project, not piles of paperwork.

- Close and buy. You receive the funds to purchase the home.

- Use the rehab budget. We can fund up to 100% of your repair costs, usually released in stages as the work is done.

- Fix the property. Your contractor completes the renovation.

- Sell (flip) the home. You repay the loan from the sale and keep the profit.

Because loans for fix and flip are short-term, you are not stuck with debt for years. Our term goes up to 12 months, which is enough time to fix the property and sell it without pressure.

Our Fix and Flip Loan Terms at a Glance

People always want real numbers, so here are our actual fix and flip loan terms in one clear table:

Feature | Our Fix N' Flip Private Lender Program |

Interest rate | 10–11% |

LTV (Loan-to-Value) | Up to 85% on the purchase |

Rehab budget | Up to 100% of the rehabilitation cost |

ARV (After-Repair Value) | Up to 70% |

Minimum down payment | 20% |

Loan term | Up to 12 months |

Minimum credit score | 660+ |

Tax returns | Not required |

Bank statements | Not required |

Flipping experience | Not required |

That last point is big. A lot of top fix and flip lenders only work with people who have already flipped several homes. We do not. You can start your very first flip with us, because experience is not required.

Fix and Flip Loan Rates: What Should You Expect?

The most common question we hear is about cost. Our fix and flip loan rates sit in the 10–11% range. That may sound higher than a normal mortgage, and it is, but that is completely normal for hard money.

Here is why higher fix and flip rates still make sense: these loans are short-term, fast, and flexible. You are not paying that rate for 30 years. You are paying it for a few months while you flip the house. The speed and easy approval usually matter far more to a flipper than the rate itself, because a fast "yes" is what lets you grab the deal in the first place. A slightly higher rate on a deal you actually win beats a low rate on a deal you lost.

Comparison: Fix and Flip Loan vs Hard Money Loan vs Bank Loan

Many new investors ask which loan to use. This table compares our two main investor products against a typical bank loan so you can see the difference quickly:

Feature | Fix N' Flip Private Lender | General Hard Money Loan | Typical Bank Loan |

Interest rate | 10–11% | 10–14% | 6–8% |

Funds the repairs? | Yes, up to 100% | Sometimes | Usually no |

Speed to fund | Fast | Fast | Slow (weeks/months) |

Minimum credit score | 660+ | 500+ | 700+ |

Tax returns needed? | No | No | Yes |

Loan term | Up to 12 months | 12–24 months | 15–30 years |

Best for | Buying + fixing + reselling | Lower credit or unusual deals | Long-term holds |

As you can see, the rate is higher with hard money, but you trade that for speed, easy approval, and money for repairs, the three things a flipper actually needs.

Fix and Flip vs Hard Money Loan: What's the Difference?

A lot of people ask about fix and flip vs hard money loan as if they are two totally different things. In reality, a fix and flip loan is usually a type of hard money loan. The fix and flip version is just built specifically for buying, repairing, and reselling a property.

So when you are deciding between hard money loans or fix and flip loan products, here is a simple way to look at it:

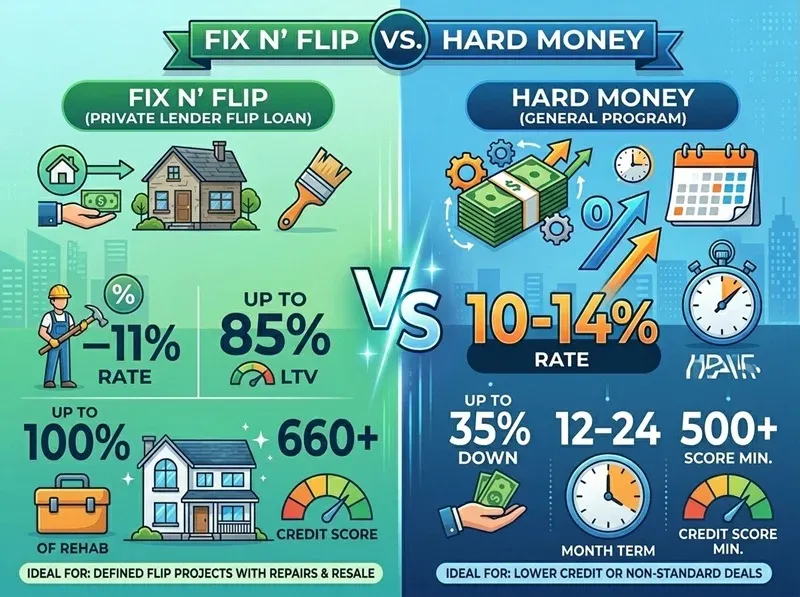

- Fix N' Flip Private Lender (our flip loan): 10–11% rate, up to 85% LTV, up to 100% of rehab, 660+ credit. Best when you have a clear flip project with repairs and a resale plan.

- Hard Money Loan (our general program): 10–14% rate, up to 65% LTV, 35% down, 12–24 month term, and a lower 500+ credit score minimum. Best when your credit is lower or your deal does not fit the standard flip box.

If your credit is below 660 or your project is unusual, the general hard money option may still get you funded. We will help you pick the right one for your situation.

Are Hard Money Loans a Good Idea?

Many first-time investors wonder, "Are hard money loans a good idea?” The honest answer: yes, for the right project. If you have a solid deal where the after-repair value is well above your total cost, a hard money loan helps you act fast and win the deal. If your numbers are tight or the property barely makes a profit, the higher rate can eat your margin. So the math has to work first.

Pros and Cons of Fix and Flip Hard Money Loans

Pros | Cons |

Very fast approval and funding | Higher interest rate than a bank |

Funds both purchase and repairs | Short repayment window |

No tax returns or bank statements | You need a clear exit plan |

Lower credit requirements | Best for short-term projects only |

Experience not required | Costs more if your flip runs late |

Are hard money loans safe?

People also ask, are hard money loans safe? They are as safe as any loan, as long as you borrow responsibly and have a real exit plan (selling or refinancing). The main risk is buying a bad deal but not the loan type itself. A good lender will be upfront about every cost and term. As long as you run your numbers carefully before you borrow, hard money is a normal, widely used tool for property flippers.

How to Use a Hard Money Fix and Flip Calculator

Before you borrow a single dollar, do the math. A hard money loan fix and flip calculator helps you see if a deal will actually make money. You plug in numbers like the following:

- Purchase price

- Repair (rehab) budget

- Loan amount and interest rate

- Holding costs (taxes, insurance, utilities)

- Closing and selling costs

- Expected sale price (ARV)

A simple example

Here is what a basic deal might look like when you run it through a hard money fix and flip calculator:

Item | Amount |

Purchase price | $150,000 |

Repair budget | $40,000 |

Loan + holding costs (about 6 months) | $15,000 |

Selling costs | $12,000 |

Total cost | $217,000 |

Expected sale price (ARV) | $275,000 |

Estimated profit | $58,000 |

If the profit is too small after all costs, walk away. This one habit separates flippers who win from flippers who lose money. If you would like, we can help you run your numbers before you apply.

What You Need to Qualify for a FIx and FLip Loan

One of the best things about our program is how simple the requirements are. To qualify, you generally need:

- A credit score of 660+ for the fix and flip program (or 500+ for our general hard money loan)

- At least a 20% down payment

- A property and a clear plan to fix and resell it

- A deal where the numbers make sense after repairs

You do not need tax returns, bank statements, or past flipping experience. That is what makes the process so much faster than a bank.

How to Find a Good Lender

If you have been searching online for “fix and flip hard money lenders near me” here is what to look for in a trustworthy lender:

- Clear terms. They explain the rate, LTV, ARV, and loan term up front, with no surprises.

- No hidden fees. Everything is in writing before you sign.

- They fund repairs. The best programs cover both the purchase and the rehab.

- Fast communication. They answer your questions quickly and close on time.

- Fair credit rules. Good lenders look at the deal, not just your credit.

Commercial Lending USA aims to be one of the best fix-and-flip hard money lenders on every one of these points.

0 Comments

Leave A Comment