Are You Paying Too Much? Navigating Current Investment Property Mortgage Rates

Is your dream property slipping away because the numbers don't add up? Every investor worries about paying too much—especially when securing financing for an investment.

The real estate market is a relentless force, and what you paid for your first home is very different from today's mortgage rates for investment properties. This rapid change is the primary source of investor anxiety. The core pain point is simple: Lenders view rental properties as riskier than primary residences. This is why you often see a higher rate, which can quickly erode your potential profit margins. According to data from the U.S. Census Bureau, the national rental vacancy rate—a key indicator of market health—has fluctuated significantly, underscoring the dynamic risks involved in rental investments. Navigating these risks while securing favorable financing requires more than just searching for "investment property mortgage rates current" online—it requires expertise.

We are Commercial Lending USA. We're not just a broker; we're a trusted correspondent and table lender with 30 years of underwriting experience. We have a deep understanding of the market and know the secrets to securing better rates than conventional banks offer. We promise to cut through the noise. This guide breaks down exactly what you need to know about investment property mortgage rates, current conditions, and the true factors driving the numbers. Our platform connects you to over 1,000 private lenders, investors, brokers, and realtors, giving you unparalleled access and helping you avoid overpaying for your next real estate venture.

The Truth About Investment Property Rates Today

Securing the right financing is the pivot point for any successful real estate investment. The reality is, the current mortgage rates for investment property are fundamentally structured differently from those for a primary home, and understanding why is your first step to saving money.

Why Are Investment Rates Higher? The Risk Factor Explained

Lenders operate on one core principle: risk. A simple, conversational way to look at it is: Lenders believe that if you ever face a financial pinch, you'll pay the mortgage on the house you live in (your primary residence) before the mortgage on your rental property. That perceived risk costs you money.

Because investment properties are non-owner-occupied, they are classified as higher risk. To offset this, lenders attach a risk premium to the interest rate. Historically, this premium has typically ranged from 0.5% to 1.5% above a comparable primary residence loan.

This risk factor is also why the current 30-year mortgage rates for investment property can differ significantly from the current 15-year mortgage rates for investment property. A longer loan term (30-year) gives the borrower more time, but also extends the period the lender is exposed to market risk, often resulting in a slightly higher rate than a shorter 15-year term.

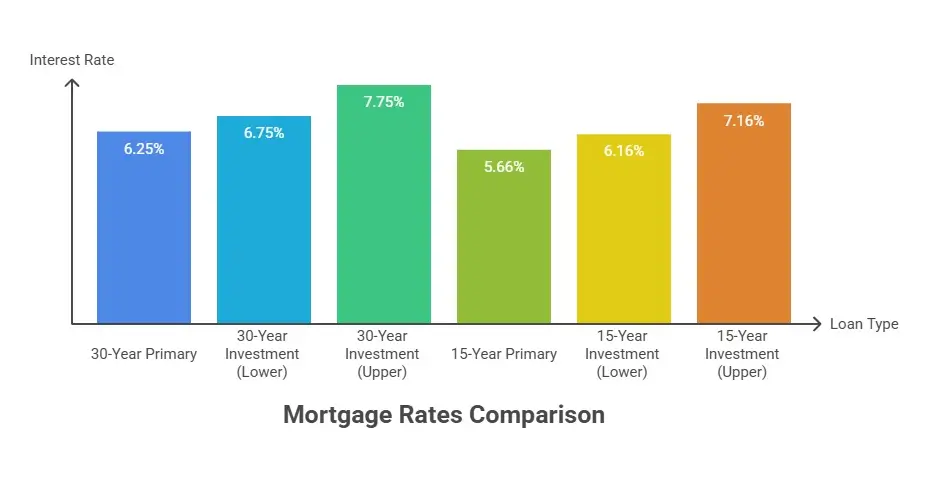

Loan Type Primary Home (Example Rate) Investment Property (Est. Range)

30-Year Fixed 6.25% 6.75% – 7.75%

15-Year Fixed 5.66% 6.16% – 7.16%

Data Snapshot: The average 30-year fixed mortgage rate for a primary residence hovered around 6.22% in early November 2025 (Source: Freddie Mac, a government-authorized enterprise). This data confirms the baseline upon which the investment property risk premium is added.

Decoding Today's Average Rates

What is the national average current mortgage rate for investment property? As of mid-November 2025, conventional 30-year fixed rates for investment properties generally start in the 6.75% to 7.75% range for well-qualified borrowers. However, this is just a starting point—your rate depends on your credit score, down payment, and cash reserves.

Introducing the DSCR Loan (A Smarter Option)

In today's challenging rate environment, investors are increasingly turning to DSCR (Debt Service Coverage Ratio) loans. This is a niche product in which approval is based on the property's ability to generate sufficient cash flow, not on your personal income. This demonstrates sophisticated expertise in navigating modern lending.

- No personal income check needed. You don't need tax returns or W-2s; the loan is primarily underwritten on an asset basis.

- The property's rent must cover the payment. The DSCR is the ratio of the property's Net Operating Income to the mortgage payment. A ratio above 1.0 is generally required.

- Rates are higher, but approval is faster. DSCR loans often carry rates similar to or slightly higher than those of traditional investment loans (typically 6.5% to 8.5%). Still, they offer a streamlined, faster closing process that can be critical in competitive markets.

Beyond the 30-Year Fixed: Other Investment Options

The current mortgage rate for investment property also depends heavily on the loan type and purpose.

For example, a current mortgage rate for a single-unit investment property (a 1-4 unit residential home) will typically use conventional or DSCR financing, which generally offers the most competitive rates. Conversely, a multifamily investment property (5+ units) with current mortgage rates usually requires a commercial loan, which has a different underwriting structure and rate scale.

Furthermore, a loan for a "Fix and Flip" project (a short-term, 12-month loan focused on renovation) will have a much higher rate and interest-only payments than a "Buy and Hold" loan (a long-term 30-year mortgage for an investment property). Understanding the right product for your goal is key to securing the best terms.

The Money Factors You Control

While you can't control the Federal Reserve's policy, you have direct control over the three financial pillars that determine your final current loan mortgage rates for investment property. Mastering these factors is how you move from the average rate to the best-tier rate.

Your Financial Scorecard: Credit, Down Payment, and Reserves

Lenders use these "Big Three" to measure your ability and willingness to repay a loan, especially one as risky as an investment property.

Credit Score (Your Repayment Track Record)

Your credit score is your financial report card. A higher score means less risk for the lender. To lock in the most competitive current mortgage interest rate for investment property, you generally need a score of 740 or higher.

Statistic: Data shows that borrowers with credit scores below 660 typically receive mortgage rates that are 0.5% to 1.0% higher than those with scores over 760 (Source: FICO/Experian data). This difference can cost you tens of thousands of dollars over the life of a loan.

Down Payment (Your Skin in the Game)

The down payment shows the lender how much capital you are personally risking. For investment properties, the typical minimum is 20% to 25%.

- The Rule: More cash down means less risk for the lender, which directly translates to a better current mortgage interest rate for investment property. For example, putting 25% down instead of 20% can often reduce your rate by an eighth or a quarter of a percent.

Cash Reserves (Your Safety Net)

This is a crucial factor often overlooked. Lenders want assurance that you can cover the mortgage (Principal, Interest, Taxes, and Insurance, or PITI) even if the property is vacant for a few months.

- The Requirement: Lenders often require you to have 6 to 12 months of the total monthly PITI payment for the investment property sitting in liquid bank accounts after closing. For investors with multiple financed properties, this reserve requirement can increase significantly.

The Power of Your Investment Type

The nature of the asset being financed dictates the type of loan and, consequently, your current investment property mortgage interest rates. Lenders view different projects through different risk lenses.

Multifamily vs. Single-Family

In many cases, the current mortgage rates for multifamily investment property (2-4-unit residential) might be slightly better than those for single-family rentals. Why? Because if one tenant moves out of a duplex, you still have income from the other tenant, which lowers the lender's vacancy risk.

Project-Specific Rates

Your rates will vary dramatically based on the loan's purpose:

- Land Purchase / Ground-Up Construction: These carry the highest risk because there is no finished collateral or immediate cash flow. Consequently, the rates are typically higher, and the terms are shorter (often interest-only).

- Simple Fix and Flip: These are short-term loans (6-18 months) with higher rates because the lender is exposed to the volatility of construction costs and the rapid sale market.

- Buy and Hold: A 30-year fixed loan on a stabilized rental property offers the lowest current mortgage interest rate for investment property among investment-specific options, as the risk is mitigated by established cash flow and a long repayment term.

Commercial and Specialized Loans

For extensive or specialized properties—like a small apartment complex (5+ units), a hotel, or a restaurant—you move into commercial lending territory. These are specialized loans that require specific backgrounds and different underwriting.

Commercial Lending USA Expertise: We offer assistance with 75+ loan options, including SBA, CMBS, and Bridge Loans, covering hotels, restaurants, industrial facilities, and more. This specialized access allows us to tailor a product to the exact risk profile of your commercial project, ensuring you don't overpay.

How to Beat the Average Rate (The Commercial Lending USA Advantage)

Knowing your financial scorecard is only half the battle. The other half is leverage—and that's where Commercial Lending USA's unique position allows you to transcend the average and secure the best current mortgage rates for investment properties.

Stop Shopping Alone: The Correspondent Advantage

Most real estate investors make a costly mistake: They check only 2–3 local or national banks, then ask, "What are the current investment property mortgage rates?" They settle for the rate offered by one of the few institutions they contacted, often missing the best deal entirely.

Our Solution: True Lending Power

We are not just a middleman; we are a correspondent and table lender. This means:

- We Fund Loans: We can underwrite and close loans with our own funds, giving us direct control over the timeline and the certainty of closing.

- Vast Network Access: Beyond our own capital, our platform connects you to more than 1,000 private lenders, investors, brokers, and realtors nationwide. That's over 1,000 potential sources of capital and 1,000+ chances to beat the national average rate.

We perform a comprehensive, simultaneous review of all available options—from conventional to niche DSCR and commercial products. This guarantees that the current mortgage rates on investment property you receive are truly the lowest available for your financial profile and project type.

Statistic: A study by the Consumer Financial Protection Bureau (CFPB) found that consumers who obtained loan estimates from four or more lenders typically saved an average of $1,500 per year more than those who obtained estimates from only one lender. Our system multiplies that advantage exponentially.

Get Your Current Investment Property Mortgage Rates Pre-Approval

Pre-approval is not a formality; it is your essential competitive advantage in a tight market. It's like a warm-up for the big game—it confirms your financing is ready before you make an offer.

- Losing a high-value deal to another investor simply because your financing wasn't secured, forcing you to scramble for a rate.

- Closing the deal fast because your current investment property mortgage rates pre-approval was already secured and vetted by a 30-year underwriter at Commercial Lending USA. This puts cash in the seller's hand faster and makes your offer significantly more attractive.

Our pre-approval process is straightforward and leverages our underwriting experience, giving sellers confidence in your financing.

Program Credibility

We also offer exclusive and non-exclusive referral programs to brokers and realtors. This demonstrates that real estate professionals trust our speed and rate integrity, further validating our services.

Please don't settle for average current mortgage rates. Investment Property: It's Time to Compare

When reviewing loan offers, look beyond the simple interest rate. The accurate measure of cost is the Annual Percentage Rate (APR), which includes interest, fees, and other charges.

Don't settle for the average current mortgage rates for investment property. With Commercial Lending USA, you have access to a network designed to find the exception—the best rate possible—for your investment strategy.

Your Next Steps (Securing Your Future Rate)

Securing a great rate on your purchase is only the beginning. Savvy investors know that managing their debt over time is the key to sustainable portfolio growth.

Beyond the Purchase: Refinancing and Portfolio Growth

The best rate you secure today may not be the best rate tomorrow. Market conditions change, and a successful investor tracks their loan performance to maximize cash flow.

Refinancing for Profit

We proactively help seasoned investors monitor the market to find the optimal current mortgage rates for refinancing investment property. Whether rates drop or your property's value increases, a strategic refinance can:

- Pull Cash Out: Access equity tax-free for your next down payment.

- Lower Your Payment: Lock in better current mortgage rates for a refinance investment property to boost monthly cash flow.

- Fix and Hold/Rent: If you completed a short-term fix-and-flip and are now ready to move it to a permanent rental, we can help secure the best long-term mortgage for refinancing the investment property, turning a short-term loan into a long-term profit center.

Financing Every Type of Investment

Our expertise extends beyond single-family homes. We finance growth across a broad spectrum of asset types: land, ground-up construction, assisted living facilities, mixed-use properties, industrial warehouses, and more. Whatever your next project, we have a specialized loan to match.

Ready to Secure Your Rate?

Don't let high rates and limited options eat into your profits. The time to act is now.

Your investment is too significant to leave to chance or to the single, high rate offered by your local bank. Leverage our 30 years of underwriting expertise and our platform of over 1,000 private lenders, investors, brokers, and realtors.

Click here to get started and find the absolute best loan product for your next investment.

FAQs

1. What are the typical closing costs for an investment property loan?

Closing costs for investment properties are generally higher than for primary residences, typically ranging from 2% to 6% of the loan amount, but they can be higher. This is because investment property mortgages often have additional fees. These costs include standard items such as appraisal, title insurance, and attorney fees, as well as specific lender fees, such as origination fees (often 1% of the loan amount) and discount points (paid to buy down the interest rate). Buyers must also pay for prepaid taxes and insurance reserves at closing.

2. Is Private Mortgage Insurance (PMI) required for investment property loans with less than 20% down?

No, Private Mortgage Insurance (PMI) is generally not an option for investment properties. PMI is typically designed for conventional loans on primary residences. Because investment properties are viewed as higher risk, lenders mitigate this risk by requiring a larger down payment, usually 20% to 25% minimum. Suppose you put down less than 20% on an investment property. In that case, a traditional lender will deny the loan or require a non-conventional product (such as a DSCR loan) rather than use PMI.

3. What is the difference between a "conforming" and "non-conforming" investment loan?

A conforming loan adheres to the maximum loan limits and underwriting guidelines set by government-sponsored entities like Fannie Mae and Freddie Mac. These loans usually have the lowest rates. A non-conforming loan does not meet these guidelines, often because the loan amount exceeds the limit (called a Jumbo loan) or the borrower/property qualifications fall outside standard criteria (like a DSCR loan). Non-conforming loans generally come with stricter requirements and a slightly higher interest rate, reflecting the increased risk the lender must hold onto.

4. Can I use a DSCR loan to finance a property that is currently a "fix and flip"?

DSCR (Debt Service Coverage Ratio) loans are primarily designed for properties that are already income-producing or immediately ready to be rented (turnkey properties). While you can use a DSCR loan for a cash-out refinance after you have completed the fix-and-flip and secured a tenant, the initial purchase and renovation phase typically requires a Bridge Loan or Hard Money Loan. DSCR lenders need an accurate rental appraisal to calculate the property's ability to cover the debt, which is difficult with a vacant property under renovation.

5. Are investment property interest rates fixed or variable?

Investment properties are typically financed using both fixed-rate and variable-rate options. The most common is the 30-year fixed-rate mortgage, which offers predictable payments over the life of the loan. However, lenders also provide Adjustable-Rate Mortgages (ARMs), where the rate is fixed for an initial period (e.g., 5/1 ARM or 7/1 ARM) and then adjusts annually. Investors often use ARMs if they plan to sell or refinance the property before the fixed period ends, as the initial rate may be lower than a 30-year fixed rate.

0 Comments

Leave A Comment