Gas Station Financing in 2026: Loans, Rates, and How to Get Approved

Buying or building a gas station can be a smart move, whether you are a first-time owner or an investor adding to your portfolio. Gas stations offer steady demand and multiple income streams, but they also come with high upfront costs and a few unique hurdles, like fuel supply agreements and environmental reports. The right financing makes all the difference.

This guide explains how gas station financing works in 2026, the best loan options, current rates, how much you need to put down, and the exact steps to get approved. As a commercial mortgage broker, Commercial Lending USA helps business owners compare these options and connects them with the right lending sources for their deal.

How Gas Station Financing Works

A gas station is what lenders call a "special-use" property, and most purchases involve both real estate and a business. Because of that, financing usually comes from one of a few sources: government-backed SBA loans, USDA loans, conventional commercial loans, or private (bridge and hard money) financing.

Commercial Lending USA reviews your deal, packages it properly, and shops it to the lenders most likely to fund a gas station like yours. For a special-use property, that matching process matters a lot, because not every lender is comfortable with fuel stations.

Best Loan Options for Buying a Gas Station

Here are the main ways to finance a gas station, side by side:

Loan Type | Typical Rate (2026) | Down Payment | Term | Best For |

SBA 7(a) | About 9% to 11.5% | Around 10% to 20% | Up to 25 years | Most gas station purchases |

SBA 504 | About 6.5% to 7.5% | Around 10% to 20% | Up to 25 years | Real estate and fixed equipment |

USDA B&I | About 7% to 8% | Around 20% | Up to 30 years | Stations in rural or suburban areas |

Conventional Commercial | About 7% to 8.5% | 25% or more | Varies | Strong-credit, established buyers |

Bridge / Private | About 9% to 14% | 30% to 35% | 12 to 36 months | Fast closings or unique deals |

SBA 7(a) Loans

The SBA 7(a) is the most popular choice for gas stations. It is a government-guaranteed loan, which means the SBA backs a large share of it, allowing lenders to offer longer terms and competitive rates. It can cover the property, the business, equipment, and even working capital. As of mid-2026, with the prime rate at 6.75%, SBA 7(a) rates generally run from about 9% to 11.5%. To qualify, the business must be for-profit, owner-occupied (the owner must occupy at least 51%), and the borrower must show the ability to repay.

SBA 504 Loans

The SBA 504 is built specifically for buying real estate and long-life equipment, like fuel systems and buildings. It usually offers a fixed rate and is often the lowest-cost option for the real estate portion. SBA 504 rates in 2026 generally fall in the 5% to 7% range on the fixed CDC portion, which makes it attractive for buyers who want long-term payment stability.

USDA B&I Loans

If the gas station is located in a rural or suburban area, a USDA Business and Industry (B&I) loan can be a strong fit. These offer long terms up to 30 years. You should confirm the location qualifies on the USDA eligibility map before going this route.

Conventional Commercial Loans

A traditional bank loan can also fund a gas station, but the bar is higher. Banks usually want a strong credit score (often 680 or above), a solid down payment, and proven business stability. These loans can offer good rates for well-qualified buyers.

Bridge and Private Loans

When a deal needs to close fast, or when a buyer does not fit standard bank rules, a bridge or private loan can bridge the gap. These have higher rates and shorter terms, but they move quickly. Investors often use them to secure a property and later refinance into long-term SBA or conventional financing.

How Much Down Payment Do You Need?

Down payment is one of the biggest questions for gas station buyers. Here is a general guide:

Financing Type | Typical Down Payment |

SBA 7(a) and 504 | Around 10% to 20% |

USDA B&I | Around 20% |

Conventional | 25% or more |

Bridge / Private | 30% to 35% |

SBA programs usually require the least money down, which is one reason they are so popular for gas stations. Special-use properties sometimes require a bit more equity because of the added risk, so your exact number depends on the deal, your experience, and the property.

Gas Station Loan Rates in 2026

Rates depend on the loan type, your credit, your experience, and the property itself. The single biggest driver in 2026 is the prime rate, which sits at 6.75%. SBA 7(a) loan rates are capped at a spread over prime, and most competitive lenders are pricing strong borrowers around 9% to 9.5% for acquisition loans. SBA 504 loans are priced lower on the real estate portion, while private financing is priced highest.

Because rates move with the market and vary by lender, the smartest approach is to compare several offers. That is exactly what a broker helps you do.

What Lenders Look At for Gas Station Loans

When reviewing a gas station deal, lenders focus on a few key things:

- Business cash flow. Can the station's income comfortably cover the loan payment? Strong, documented sales make approval far easier.

- Credit score. Most SBA and conventional lenders look for a 680 or higher credit score, though some programs are flexible.

- Down payment and equity. More money down lowers the lender's risk.

- Experience. Prior business or gas station experience helps, though it is not always required.

- The environmental report. This is unique to fuel properties, and it is a big one.

The Environmental Piece: Why Gas Stations Are Different

Gas stations store fuel in underground storage tanks, so lenders require an environmental review before they will fund the deal. This usually starts with a phase I environmental site assessment, which checks the property's history for contamination risk. If concerns come up, a Phase II assessment with soil or water testing may follow.

This step protects you as much as the lender. Buying a station with a leaking tank can be enormously expensive. Budget time for this review in your closing timeline, since it is a normal and required part of gas station financing.

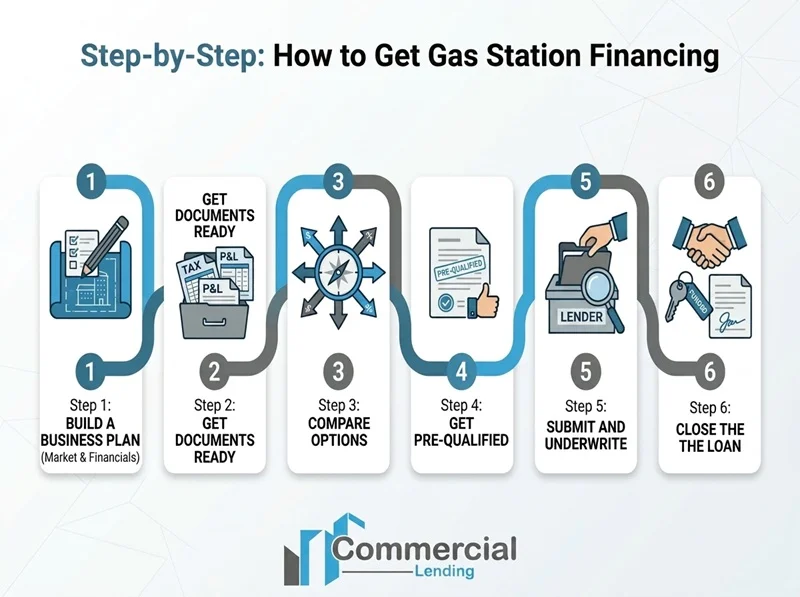

Step-by-Step: How to Get Gas Station Financing

- Build a business plan. Include realistic income, expenses, and growth projections. Lenders want to see you understand the business.

- Get your documents ready. Expect to provide tax returns, financial statements, a credit report, the purchase agreement, and environmental reports.

- Compare your options. Different lenders price and view gas stations differently. This is where working with a broker saves time.

- Get pre-qualified. This tells you your likely loan amount and rate before you commit.

- Submit and underwrite. The lender verifies the business income, your finances, the property value, and the environmental report.

- Close the loan. Once approved, you sign and fund, and the station is yours.

What It Costs and How Gas Stations Make Money

Gas stations earn from more than just fuel. In fact, fuel margins are often thin, and the real profit comes from the extras. The main revenue streams include:

- Fuel sales. Steady demand, but lower margins.

- Convenience store sales. Often the biggest profit driver, with high margins on snacks, drinks, and everyday items.

- Car wash. A strong add-on that boosts profit with low ongoing cost.

- Other services. Lottery, ATM fees, food service, and more.

When you finance a gas station, lenders look closely at these combined income streams, especially the convenience store, since it often carries the profitability of the whole business.

Refinancing a Gas Station

Financing is not only for buying. Many owners refinance an existing gas station to lower their rate, pull out equity for upgrades, or move from a short-term private loan into a long-term SBA or conventional loan. If you bought with a bridge loan to close fast, refinancing into an SBA 7(a) or 504 is a common next step once the business is stable.

Common Challenges and How to Handle Them

- High upfront cost. Plan for a solid down payment, and consider SBA programs that require less money down.

- Special-use property. Not every lender funds gas stations, so work with someone who knows which lenders do.

- Environmental risk. Always complete the environmental review, and never skip it to save time.

- Industry complexity. Fuel supply agreements, branding, and permits add layers. Lean on experienced advisors.

2026 Trends Shaping Gas Stations

The industry keeps evolving, and lenders pay attention to where it is headed:

- Convenience stores lead profits. Stations are becoming one-stop shops, and the store is where the margin is.

- EV charging. As electric vehicles grow, adding charging stations can future-proof a location and bring in new customers.

- Technology. Self-service fueling, cashless payment, and automated inventory cut labor costs and improve margins.

Buyers who plan for these trends often present stronger loan applications, because lenders see a business built for the future.

Why Work with Commercial Lending USA

We make gas station financing simpler. As a commercial mortgage broker and correspondent, Commercial Lending USA:

- Reviews your deal and packages it the way lenders want to see it

- Compares options across a network of capital sources, including SBA, USDA, conventional, and private lenders

- Helps you find competitive rates and terms for a special-use property

- Guides you through the environmental review and documentation

- Offers in-house underwriting support to help keep your file moving

Commercial Lending USA is a member of the American Association of Private Lenders and is BBB accredited, so you are working with an experienced, trusted partner.

Ready to Finance Your Gas Station?

Whether you are buying your first station, expanding, or refinancing, the right loan starts with the right guidance. Reach out to Commercial Lending USA today for a free consultation. Call (855) 365-9200 or apply online, and we will help you compare your options and move toward approval.

Frequently Asked Questions

What is the best loan for buying a gas station?

For most buyers, an SBA 7(a) or SBA 504 loan is the best option. They offer long terms, competitive rates, and lower down payments. The 504 is ideal for the real estate portion, while the 7(a) is more flexible and can also cover the business and working capital.

What credit score do I need to finance a gas station?

Most SBA and conventional lenders look for a credit score of 680 or higher for the best terms. Some private loan programs are more flexible on credit but charge higher rates.

How much down payment do I need for a gas station?

SBA loans typically require around 10% to 20% down. Conventional loans usually want 25% or more, and private loans often require 30% to 35%. Special-use properties like gas stations sometimes require a bit more equity.

What are gas station loan rates in 2026?

With the prime rate at 6.75%, SBA 7(a) rates generally run about 9% to 11.5%, SBA 504 rates fall in the 5% to 7.5% range on the real estate portion, and private loans run higher. Your exact rate depends on your credit, experience, and the deal.

Can I get an SBA loan for a gas station?

Yes. Gas stations are commonly financed with SBA 7(a) and 504 loans, as long as the business is for-profit and owner-occupied, meaning the owner occupies at least 51% of the property.

Why do gas stations need an environmental report?

Gas stations store fuel in underground tanks, so lenders require a Phase I Environmental Site Assessment to check for contamination risk. This protects both you and the lender from costly cleanup surprises.

Can I finance a gas station with a convenience store or car wash?

Yes. In fact, lenders like these added income streams because the convenience store and car wash often carry most of the profit. Combined revenue can strengthen your loan application.

Can I refinance my existing gas station?

Yes. Owners often refinance to lower their rate, access equity for upgrades, or move from a short-term private loan into a long-term SBA or conventional loan.

Is Commercial Lending USA a direct lender?

No. Commercial Lending USA is a commercial mortgage broker and correspondent. We do not approve loans ourselves. We connect you with the right lenders and guide you through the process.

How do I get started?

Call (855) 365-9200, email sales@commerciallendingusa.com, or apply online for a free consultation about your gas station financing options.

Disclaimer: Loan rates and terms shown here are based on current programs and market conditions as of 2026 and may change at any time. Rates move with the market and vary by lender and borrower profile. All loans are subject to lender approval and underwriting. This article is for general information only and is not financial or legal advice.

0 Comments

Leave A Comment