Commercial Loans Ultimate Guide 2026: Rates Terms LTV Requirements and How to Choose the Right Program

If you are a business owner or real estate investor looking to purchase, refinance, or build commercial property, you need clear reliable information on commercial loans. The right financing can make the difference between seizing a great opportunity and watching it slip away. This ultimate guide explains everything borrowers need to know about commercial loans in 2026. You will see current rates, terms, loan-to-value ratios down payments, credit requirements, and qualification steps for 17 popular programs.

For a quick side-by-side comparison of all 17 programs with 2026 rates and terms, jump to our Commercial Loan Programs Comparison 2026.

What Is a Commercial Loan and How It Differs from Residential Financing

A commercial loan is financing designed specifically for business purposes. You can use these funds to buy office buildings, retail spaces, warehouses, industrial properties, or land for development. You can also refinance existing commercial real estate or fund construction and renovations.

Commercial loans differ from residential mortgages in several important ways. Residential loans focus on homes you live in or rent out as personal investments. Commercial loans support active business operations. Lenders look closely at your business cash flow profitability and overall financial health in addition to the property itself.

Loan terms also vary. Residential mortgages often run 15 to 30 years with fixed rates. Commercial loans range from short-term bridge options of 12 to 36 months up to 30-year terms on stabilized properties. Interest rates on commercial loans tend to be higher than residential rates because of the added risk to lenders.

Collateral requirements are stricter too. The property serves as primary collateral, but lenders also review your business tax returns bank statements, debt service coverage ratio, and personal credit. This comprehensive review helps lenders confirm you can handle the payments while growing your business.

17 Commercial Loan Programs Compared 2026 Rates and Terms

The table below gives you the most up-to-date comparison of the 17 most common commercial loan programs available right now. All figures reflect typical 2026 market conditions. Actual rates and terms depend on your credit profile property type and location. Use this as your starting point when comparing commercial loan programs.

SL | Loan Program | Interest Rate Range (%) | LTV (Max) | LTC % | ARV | Down Payment (Min) | Loan Term | Credit Score (Min) | Bank Statement | Tax Return |

1 | 9-12 | Up to 70% | N/A | No | 30% | 12-36 months | 620+ | Required | No | |

2 | 10-14 | Up to 65% | N/A | No | 35% | 12-24 months | 500+ | No | No | |

3 | 6.5-7.5 | Up to 80% | N/A | No | 20% | 30 years | 660+ | No | No | |

4 | 8-9 | Up to 75% | N/A | No | 25% | 30 years | 680+ | No | No | |

5 | USDA B&I Term | 7-8 | Up to 80% | N/A | No | 20% | 30 years | 680+ | Required | Yes |

6 | 10-11 | Up to 65% | Up to 75% | 65% | 25% | 30 years | 680+ | Required | Yes | |

7 | 8.5-9.0 | Up to 80% | Up to 80% | 70% | 20% | 25 years | 680+ | Required | Yes | |

8 | 6.5-7.5 | Up to 80% | Up to 80% | 70% | 20% | 25 years | 680+ | Required | Yes | |

9 | 10-11 | Up to 70% | Up to 75% | 65% | 25% | Up to 12-24 months | 660+ | No | No | |

10 | 10-11 | Up to 75% | Up to 85% | 70% | 20% | Up to 12 months | 660+ | No | No | |

11 | 5.5-6.5 | Up to 70% | 70% | 65% | 25% | Up to 30 years | 680+ | Required | Yes | |

12 | 10-12 | Up to 70% | N/A | No | 30% | Up to 30 years | 660+ | No | No | |

13 | Lite-Doc Loan | 8-11 | Up to 75% | N/A | No | 25% | Up to 30 years | 660+ | Required | No |

14 | 8-11 | Up to 75% | N/A | No | 25% | Up to 30 years | 660+ | Required | No | |

15 | 5.25-6.5 | Up to 80% | Up to 85% | 75% | 15% | Up to 40 years | 680+ | Required | Yes | |

16 | Blanket Loan | 10-11 | Up to 70% | N/A | No | Up to 30% | Up to 30 years | 660+ | No | No |

17 | CMBS | 7-8.5 | Up to 70% | N/A | No | Up to 30% | Up to 30 years | 680+ | Yes | Yes |

This table makes it easy to see which programs fit your down payment budget, credit profile, and property type. For example, borrowers with strong rental income often prefer DSCR loans, while owner-occupied businesses look at SBA options first.

The world of commercial loans offers a variety of options to suit your specific business needs. Here's a quick breakdown of some of the most common types:

- Term Loans: These are the workhorses of commercial financing, providing a lump sum of money to be repaid over a fixed term with regular monthly installments. They're ideal for financing property acquisition, equipment purchases, or any significant one-time expense.

- SBA Loans: Backed by the Small Business Administration, these government-guaranteed loans offer attractive terms for qualified small businesses. They can be used for various purposes, including working capital, expansion, and real estate acquisition.

- Construction Loans: Explicitly geared towards financing the development or construction of commercial property, these loans typically have shorter terms and are paid off once the construction project is complete.

- Lines of Credit: Think of a line of credit like a business credit card. It provides access to a pre-approved amount of funding you can tap into as needed, offering flexibility for ongoing operational expenses or unexpected needs.

Loan Type Factors to Consider for a Commercial Loan:

The specific requirements for each loan type will vary depending on the lender. However, some general factors lenders consider include the following:

- Business financials: Your credit history, profitability, and cash flow will be heavily scrutinized.

- Loan purpose: A clear and well-defined plan for using the loan funds is essential.

- Collateral: The property you're financing or other business assets may be used as collateral to secure the loan.

By understanding the different types of commercial loans and the factors that influence qualification, you can decide on the best financing option for your business needs.

Unlock Your Business Potential with a Commercial Loan

A commercial loan can be the fuel that propels your business to new heights. Here's how this powerful financing tool can help you achieve your goals:

Grow Your Space: Whether you need a larger office to accommodate a growing team or a spacious warehouse to manage increased inventory, a commercial loan can help you acquire the property you need to expand your operations.

Invest in Your Infrastructure: Renovating your existing space, upgrading equipment, or making strategic improvements can significantly enhance your business's efficiency and productivity. A commercial loan allows you to invest in these improvements without dipping into your daily operating capital.

Unlock New Opportunities: That dream location for your new retail store or that perfect piece of land for development has finally become available. A commercial loan can empower you to seize these opportunities and translate them into tangible growth for your business.

Generate Income Streams: Commercial property can be a valuable asset that generates income. For example, acquiring a multi-unit building allows you to collect rent. At the same time, a strategically located warehouse could offer storage solutions to other businesses. A commercial loan can help you secure these income-producing properties.

Achieve Long-Term Goals: Surely, commercial loan is an investment in your business's future. Finishing essential property needs frees up working capital to invest in marketing, research, and development – all crucial aspects of achieving your long-term vision.

In short, a commercial loan is a strategic tool beyond simply acquiring property. It's about investing in the tools and infrastructure your business needs to thrive and generate revenue.

Qualification Guidelines Every Borrower Should Know

Understanding qualification rules helps you prepare a stronger application and avoid surprises. Here are the key guidelines straight from current lender standards.

SBA Loans Eligibility

Small owner-occupied businesses with a minimum of 51 percent owner occupancy qualify. The business must show profitability and provide full documentation. Projection based income or working capital requests usually fall under the SBA 7a program. Eligible property types include restaurants, self-storage facilities, gas stations, car washes, daycare centers, medical offices, and other qualifying owner-occupied businesses.

Non-SBA Loan Options for Insufficient Income

If your loan does not qualify for SBA programs because of insufficient income on business or personal tax returns, consider the Lite Doc Loan, Stated Income Loan, or No Doc Term Loan. These options support maximum loan amounts up to 5 million dollars per property.

Blanket Loans

Borrowers who own multiple residential properties across different locations often choose blanket loans. This program streamlines financing for an entire portfolio in one transaction.

Property Requirements

If the property value is 150000 dollars or higher and it is rented consider a DSCR loan for more favorable terms.

Income and Vacancy Rates Guidance

Unstable income or high vacancy rates may require review under the No Doc Term Loan. In such cases bridge loans or hard money options provide flexible short-term solutions.

USDA B&I Loans

Confirm eligibility using the official USDA qualification map before proceeding. These loans work best for properties located in suburban or rural areas.

Construction Loans

Collect three years of business and personal tax returns. Lenders evaluate the borrowers' debt-to-income ratio income stability, credit history, and relevant experience.

SBA, USDA, B&I, FHA, and Conventional Loans

All of these programs must strictly adhere to underwriting guidelines. Working with an experienced lender ensures your application meets every requirement.

Loan to Value and Loan to Cost Considerations

Fix and flip loans allow up to 85 percent loan to value on the purchase price and up to 100 percent of the rehabilitation budget. Experience is not always required.

New construction loans adjust loan-to-value and loan-to-cost ratios depending on whether the project is residential or commercial. Commercial new construction projects typically require lower ratios than residential ones.

How to Choose the Right Commercial Loan Program

Start by reviewing your credit score, down payment amount, property type and intended use of funds. Short-term options like bridge loans and hard money loans suit quick acquisitions or renovations. Long term programs such as DSCR SBA and Fannie Mae loans support stable cash flow properties.

Match the loan term to your business plan and cash flow projections to avoid unnecessary costs. Consider these questions:

- Do you need fast funding with flexible documentation?

- Is the property owner-occupied or investment-based?

- How much down payment can you comfortably provide?

- What is your minimum credit score?

Answering these questions narrows your options quickly. The comparison table above serves as your decision-making tool.

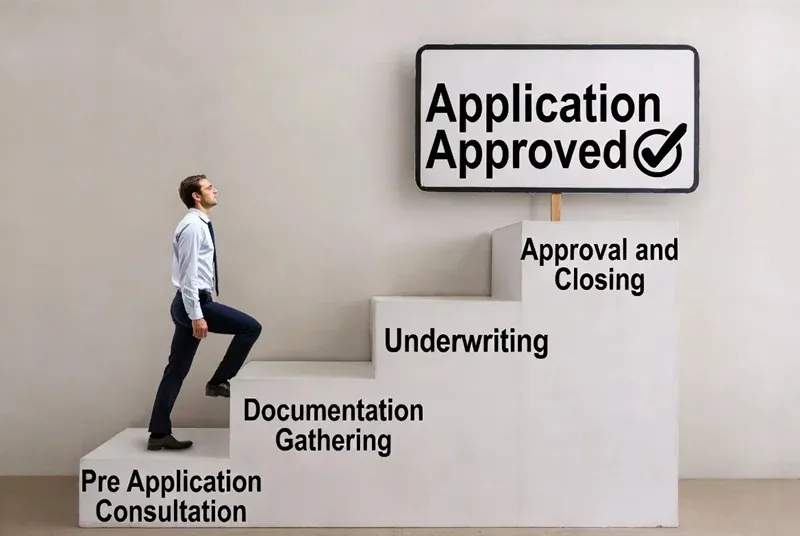

Step-by-Step Commercial Loan Application Process

Securing a commercial loan follows a clear sequence of steps. Here is what borrowers can expect in 2026.

- Pre-application consultation Speak with a commercial lending specialist who reviews your goals, property details, and financial picture. This step usually takes one to two days and gives you a realistic view of available programs.

- Documentation Gathering Prepare financial statements, tax returns, bank statements, business plans, and property information. Some programs require full tax returns, while others accept bank statements or stated income documentation.

- Underwriting The lender evaluates your application package. This review looks at credit history cash flow debt service coverage ratio and property appraisal. Turnaround time ranges from a few days for private lender programs to several weeks for government-backed loans.

- Approval and Closing Once approved, you receive a commitment letter with final terms. The closing process includes title work, appraisal review, and legal documentation. Funds are typically disbursed within 30 to 60 days of application depending on the program.

Factors That Affect Commercial Loan Approval in 2026

Lenders focus on several key factors when deciding approval and pricing.

- Creditworthiness: Both personal and business credit scores matter. Most programs require a minimum of 620, while preferred rates start at 680.

- Debt Service Coverage Ratio: Lenders want to see that the property or business generates enough income to cover loan payments. DSCR loans base approval primarily on this ratio.

- Loan Purpose and Property Type: Owner occupied properties often qualify for better terms through SBA programs. Investment properties work well with DSCR and Fannie Mae options.

- Down Payment and Equity: Higher down payments generally improve approval odds and lower interest rates.

- Documentation Strength: Full documentation programs offer the lowest rates but require complete tax returns and financial statements. Limited documentation programs provide faster approvals for borrowers with strong credit and cash reserves.

The Edge of Expertise: Expediting Approval with In-House Underwriting

The underwriting process can be a complex dance. Here's where Commercial Lending USA's in-house underwriting expertise comes into play. Our team of seasoned professionals understands the intricacies of commercial loan applications and lender requirements. We can:

Package Your Application for Success: We'll meticulously compile your application, ensuring it includes all necessary documentation and is presented in a way that effectively highlights your strengths.

Navigate Lender Requirements: We extensively know various lenders' underwriting criteria. This allows us to tailor your application to meet the specific requirements of the lenders most likely to approve your loan.

Advocate for Your Business: Our team will act as your advocate throughout the process, confidently presenting your business case and effectively communicating your vision to potential lenders.

By leveraging our in-house underwriting expertise, you can streamline the approval process, increase your chances of securing financing, and expedite your journey toward achieving your business goals. Let Commercial Lending USA be your guide on the path to commercial loan success.

Frequently Asked Questions

What are the different types of commercial loans available?

There are various commercial loans, each suited for specific needs. Some common types include term loans, SBA loans, construction loans, and lines of credit.

What are the benefits of using a commercial loan?

Commercial loans offer several advantages, such as financing property acquisition, expansion, renovations, and equipment purchases. They can help generate income streams and achieve long-term business goals.

How can a correspondent lender like Commercial Lending USA help me?

As a correspondent lender, we connect you with a broader range of lenders, increasing your chances of securing favorable terms. We handle communication and leverage our expertise to streamline the application process.

What steps are involved in applying for a commercial loan?

The commercial loan application typically involves pre-application, document gathering, underwriting, and approval. We recommend consulting a specialist for pre-qualification before diving into the formal application.

What documents do I need to submit for a commercial loan application?

You'll typically need financial statements, tax returns, business plans, and property information.

What factors affect commercial loan approval?

Lenders consider various factors like creditworthiness, business plan, financial health, property value (if applicable), and management expertise.

How can I get started with securing a commercial loan?

Contact Commercial Lending USA today for a free consultation or loan quote. Our team can assess your needs and guide you through the process.

What is the lowest interest rate available for commercial loans in 2026?

FHA Commercial and Fannie Mae/Freddie Mac programs currently show the lowest ranges starting as low as 5.25 percent depending on borrower qualifications.

Which commercial loan requires the lowest down payment?

FHA commercial loans allow a minimum down payment of only 15 percent, making them attractive for qualified borrowers.

Do I need full tax returns for every commercial loan?

No. Programs such as DSCR loans, No Doc Term Loans, and certain private lender options do not require tax returns.

Can I use a commercial loan for property construction?

Yes. USDA B&I Construction, SBA 7a Construction, Private Lender, and Fix N Flip programs support new builds and renovations.

How do I qualify for a DSCR loan?

DSCR loans focus primarily on the property's cash flow rather than personal income. They work well for investment properties valued at 150000 dollars or higher that are rented.

What credit score do I need for an SBA loan?

Most SBA programs require a minimum credit score of 680. Stronger scores improve approval chances and lower rates.

Are there commercial loans with no tax return requirement?

Yes. Lite Doc Stated Income and No Doc Term Loans provide alternatives when full tax documentation is not available.

Can I finance multiple properties with one loan?

Yes. Blanket loans let you finance several residential or commercial properties under a single loan agreement.

How long does commercial loan approval take in 2026?

Private lender and bridge programs can close in as little as 10 to 30 days. Government-backed programs such as SBA and FHA typically take 45 to 90 days.

What is the maximum loan amount available?

Limits vary by program and lender. Many options support loans up to 5 million dollars per property, while larger CMBS and portfolio loans can go significantly higher.

Do commercial loans require personal guarantees?

Most programs require personal guarantees from owners especially on SBA and conventional loans. Some private lender options offer limited or no personal guarantee structures.

Can I refinance an existing commercial loan?

Yes. Many programs, including DSCR, Fannie Mae, and SBA, allow cash-out refinance or rate-and-term refinance when it makes financial sense.

Ready to Move Forward with the Right Commercial Loan

At Commercial Lending USA we review your specific situation and match you with the program that offers the strongest terms and highest approval probability. Our team works directly with borrowers to simplify the process and deliver clear options.

Submit your information today for a fast prequalification and personalized rate comparison. We make the process straightforward so you can focus on growing your business and real estate portfolio.

This guide will be updated regularly as market conditions change. Bookmark it and check back for the latest rates and program details in 2026 and beyond.

0 Comments

Leave A Comment