Commercial Hard Money Loans 2026: Rates & Real Costs

If you have found a great commercial property but a bank is moving too slowly, you already understand the biggest problem in real estate: good deals do not wait. Bank loans can take months, and by then the opportunity is gone. Commercial hard money loans solve this by funding fast, often in days or weeks, using the property itself as the main security.

This guide explains what commercial hard money loans are, how they work, and, most importantly, what they really cost in 2026. You will see current rates, a full worked cost example, and clear tips to keep your costs down. Commercial Lending USA is a commercial mortgage broker and correspondent with a network of private lenders, and our role is to help you compare options and find the right fit for your deal.

What Are Commercial Hard Money Loans?

A commercial hard money loan is a short-term, asset-based loan used to buy or refinance commercial real estate. Instead of focusing mainly on your income and credit like a bank does, the lender focuses on the value of the property used as collateral. Because the property secures the loan, funding is fast and the approval rules are more flexible.

These loans are usually funded by private lenders: individuals, investment firms, and specialized funds rather than banks. That flexibility is the main benefit, and the trade-off is a higher interest rate than a traditional bank loan.

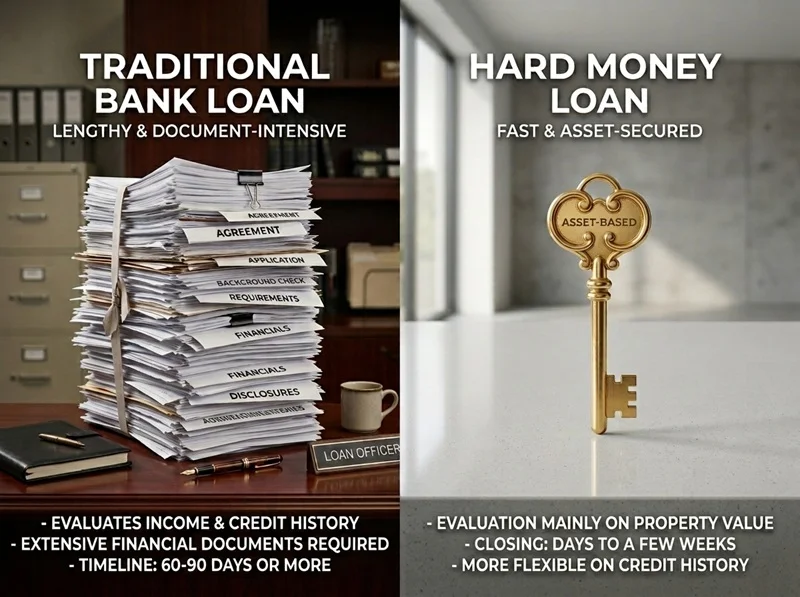

How Hard Money Differs From a Bank Loan

The biggest differences are speed and what the lender looks at. A bank loan is based on your income, credit history, and financial documents, and it can take 60 to 90 days or more. A hard money loan is based mainly on the property's value, so it can close in days or a few weeks. Hard money lenders are also more flexible on credit, which helps borrowers who do not fit strict bank rules or who need to move quickly.

Where Bridge Loans Fit In

A bridge loan is a common type of hard money financing. It "bridges" the gap between buying a property now and arranging permanent financing or selling later. Investors often use a bridge loan to buy and stabilize a property, then refinance into a long-term loan once the property is ready.

Commercial Hard Money Loan Rates in 2026

Rates are higher than bank loans because the lender takes on more risk and funds faster. As of mid-2026, commercial hard money rates typically run about 10% to 14%, with LTV caps around 60% to 70%. Lower-risk, stabilized deals price at the bottom of that range, while construction and heavy value-add projects price higher. For context, commercial bridge loans for experienced borrowers with strong deals often fall in the 9% to 11% range at 70% to 75% LTV. Crestmont CapitalAvana Capital

Most hard money loans are structured as interest-only, meaning you pay only the interest each month and repay the full principal at the end of the term when you sell or refinance.

Here is a quick snapshot of the 2026 market:

Loan Scenario | Typical Rate (2026) | Typical LTV | Term |

Stabilized commercial bridge | About 9% to 11% | 70% to 75% | 12 to 36 months |

Standard commercial hard money | About 10% to 14% | 60% to 70% | 12 to 24 months |

Value-add or construction | About 11% to 15% | Based on cost | 12 to 24 months |

Rates move with the market and vary by lender, property, and your experience. Always compare a few offers before you commit.

The Real Cost of a Commercial Hard Money Loan

The interest rate is only part of the picture. To budget properly, you need to understand every cost that goes into a hard money loan.

Interest

This is your largest cost. Because most hard money loans are interest-only, your monthly payment covers just the interest, and the principal is due at the end. A higher LTV or a riskier project usually means a higher rate.

Points (Origination Fees)

Points are an upfront fee charged as a percentage of the loan. One point equals 1% of the loan amount. In 2026, hard money lenders typically charge 1 to 4 points, so a $500,000 loan at 2 points costs $10,000 at closing. Crestmont Capital

Appraisal and Due Diligence

The lender needs to confirm the property's value and check for risks. Expect to pay for an appraisal or valuation, a title search, and any property-specific reviews. This protects both you and the lender from overpaying or inheriting a hidden problem.

Closing Costs

These include legal fees for the loan documents, title insurance, recording fees, and other administrative charges. They vary by location and loan size, so ask for a full written list before closing.

A Full Worked Cost Example

Let's walk through a realistic commercial hard money loan from start to finish so you can see the total cost.

The deal:

Detail | Amount |

Property value | $1,000,000 |

LTV | 65% |

Loan amount | $650,000 |

Interest rate | 11% (interest-only) |

Points | 2 points |

Loan term | 12 months |

Step 1: Find the loan amount.

Multiply the property value by the LTV.

$1,000,000 x 65% = $650,000 loan

Step 2: Calculate the monthly interest payment.

For interest-only, multiply the loan by the annual rate, then divide by 12.

$650,000 x 11% = $71,500 per year

$71,500 / 12 = $5,958 per month

Step 3: Calculate the points.

$650,000 x 2% = $13,000 in points

Step 4: Estimate the other upfront costs.

Appraisal: about $2,500

Title, legal, and closing: about $6,000

Step 5: Add up the total cost of the loan over 12 months.

Cost | Amount |

Total interest (12 months) | $71,500 |

Points (2%) | $13,000 |

Appraisal | $2,500 |

Title, legal, and closing | $6,000 |

Total cost of financing | $93,000 |

So on a $650,000 loan held for a full year, your all-in financing cost is roughly $93,000. That works out to an effective annualized cost of about 14.3% once points and fees are included, even though the interest rate is 11%. This is why smart investors always calculate the total cost, not just the rate. If your project profit comfortably exceeds this number, the speed of hard money is well worth it.

Commercial Hard Money vs Bank Loan: Side by Side

Feature | Commercial Hard Money | Traditional Bank Loan |

Main focus | Property value | Income and credit |

Speed to close | Days to a few weeks | 60 to 90+ days |

Interest rate | About 9% to 14% | Lower (roughly 6% to 8.5%) |

Points | 1 to 4 | Often lower or none |

Term | 12 to 36 months | 5 to 30 years |

Credit flexibility | High | Low |

Best for | Fast, short-term, or complex deals | Long-term, stabilized properties |

How to Reduce Your Hard Money Loan Costs

You have more control over your costs than you might think. Here is how to keep them down:

- Compare multiple lenders. Rates and points vary a lot. A loan at 10% with 3 points can cost more than one at 11% with 1 point, so compare the total cost, not just the rate. Working with a broker lets you shop many lenders at once.

- Lower your LTV. Putting more money down reduces the lender's risk and often earns you a lower rate.

- Have a clear exit plan. A defined plan to sell or refinance reassures the lender and can improve your terms.

- Match the term to your project. Do not pay for 24 months if your project takes 9. But do leave a safety margin so you are not forced into penalties or extensions.

- Do thorough due diligence. A careful property and title review prevents costly surprises that can blow up your budget mid-project.

Which Properties Qualify?

Commercial hard money works for many property types, including:

- Multifamily buildings (5+ units)

- Office buildings

- Retail centers and strip malls

- Industrial and warehouse space

- Self-storage facilities

- Mixed-use properties

- Land and development projects

Lenders care more about the property's value and your exit plan than the exact property type, which makes hard money flexible for a wide range of commercial deals.

Why Work With Commercial Lending USA

Financing commercial real estate is complex, and the right guidance saves you time and money. As a commercial mortgage broker and correspondent, Commercial Lending USA:

- Reviews your deal and packages it the way private lenders want to see it

- Compares options across a network of private lenders to find competitive rates and terms

- Helps you weigh the full cost of each offer, not just the headline rate

- Guides you through appraisal, due diligence, and closing

- Supports many loan types, including bridge, DSCR, SBA, and other commercial financing, so you can plan your exit

To be clear, Commercial Lending USA is a broker and correspondent, not a direct lender, so we do not approve or fund loans ourselves. We connect you with the right lenders and manage the process from start to finish. Commercial Lending USA is a member of the American Association of Private Lenders and is BBB accredited.

Frequently Asked Questions

What is a commercial hard money loan?

It is a short-term loan secured mainly by commercial real estate rather than your income or credit. Because the property is the main security, these loans fund quickly and have flexible approval rules, in exchange for a higher rate than a bank loan.

What are commercial hard money loan rates in 2026?

As of mid-2026, commercial hard money rates typically run about 10% to 14%, while strong bridge deals for experienced borrowers can fall in the 9% to 11% range. Your rate depends on the property, your experience, the LTV, and the deal's complexity.

How many points are on a hard money loan?

Points are an upfront fee, where one point equals 1% of the loan. In 2026, lenders typically charge 1 to 4 points. On a $500,000 loan, 2 points equals $10,000 paid at closing.

How do I calculate the total cost of a commercial hard money loan?

Add up the interest over your hold period, the points, and the other fees like appraisal, title, and closing. On a $650,000 loan at 11% for 12 months with 2 points, the all-in cost is roughly $93,000, or about 14.3% annualized. Always compare total cost, not just the rate.

How fast can a commercial hard money loan close?

Much faster than a bank. Depending on the deal and the lender, closings can happen in a few days to a few weeks, compared to 60 to 90 days or more for a traditional loan.

What LTV can I expect?

Most commercial hard money loans offer around 60% to 70% of the property's value, or up to about 70% of after-repair value on renovation projects. A lower LTV usually earns a better rate.

Can I use a commercial hard money loan for a fix-and-flip or value-add project?

Yes. These loans are ideal for buying and improving a property quickly. Investors commonly renovate or stabilize the property, then sell or refinance to repay the loan.

How do I pay off a hard money loan?

Most borrowers exit by selling the property or refinancing into a longer-term loan, such as a conventional commercial mortgage or a DSCR loan, once the property is stabilized or income-producing.

What happens if I default?

Because the property is the collateral, a default can lead to foreclosure, where the lender takes and sells the property to recover the loan. A clear exit plan and a realistic budget are the best ways to avoid this.

Is Commercial Lending USA a direct lender?

No. Commercial Lending USA is a commercial mortgage broker and correspondent. We do not approve or fund loans ourselves. We compare lenders on your behalf and guide you through the process.

How do I get started?

Call (855) 365-9200, email sales@commerciallendingusa.com, or apply online for a free, no-obligation review of your deal.

Disclaimer: Loan rates, points, and terms shown here are based on current programs and market conditions as of 2026 and may change at any time. Rates and costs vary by lender, property, and borrower profile. The cost example is illustrative only. All loans are subject to lender approval and underwriting. This article is for general information only and is not financial or legal advice.

0 Comments

Leave A Comment