7 Key Benefits of SBA Loans for Commercial Property

Buying your own commercial property is a big step for any small business. It means no more rent, more control, and a real asset that can grow in value. The hard part is paying for it. That is where an SBA loan for commercial property can help.

SBA loans are designed to make it easier for small businesses to buy real estate, with lower down payments and long, affordable terms. In this guide, we explain the 7 biggest benefits along with current 2026 rates and how the process works. Commercial Lending USA is a commercial mortgage broker and correspondent, and our job is to guide you and connect you with the right SBA lender for your deal.

First, What Is an SBA Loan?

The SBA is the U.S. Small Business Administration, a government agency that helps small businesses. It does not lend money itself. Instead, it guarantees part of your loan, which lowers the risk for the bank or lender that funds it. Because the government backs the loan, lenders can offer better terms than they normally would.

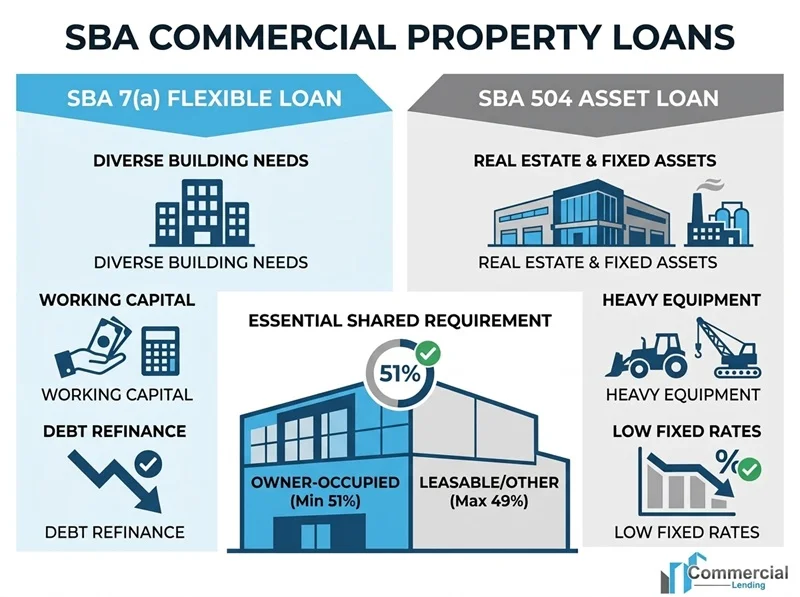

For buying commercial property, there are two main SBA loans:

- SBA 7(a): The most flexible option. It can be used for real estate, equipment, and working capital.

- SBA 504: Built specifically for buying real estate and large equipment, usually with a low fixed rate.

To qualify, your business must be for-profit and owner-occupied, meaning you use at least 51% of the property for your own business.

Now, here are the 7 key benefits:

Benefit 1: Low Down Payment

This is often the biggest reason business owners choose an SBA loan. A regular commercial loan can ask for 25% to 30% down. An SBA loan usually asks for just 10% to 20%.

That difference is huge. On a $1,000,000 property, a bank might want $300,000 down, while an SBA loan might need only $100,000 to $150,000. Keeping that extra cash in your business gives you room to hire, buy inventory, or handle surprises.

Benefit 2: Competitive Interest Rates

Because the government guarantees part of the loan, lenders can offer competitive rates. As of mid-2026, with the prime rate at 6.75%, SBA 7(a) rates for commercial property generally run about 9% to 11.5%. SBA 504 loans price lower on the real estate portion, often in the 6.5% to 7.5% range, and usually come with a fixed rate.

A lower rate means a lower monthly payment, which frees up cash flow for the rest of your business.

Benefit 3: Long Repayment Terms

SBA loans give you a long time to pay, which keeps your monthly payments manageable. For commercial real estate, terms commonly run up to 25 years.

Longer terms mean smaller monthly payments. Smaller payments mean less pressure on your cash flow and more money to reinvest in growth. This is one of the clearest advantages over short-term loans that demand quick repayment.

Benefit 4: Government Backing Makes Approval Easier

The SBA guarantees a large share of each loan, usually around 75% to 85%. This safety net makes lenders more comfortable saying yes.

For you, that means easier access to financing, even if your business is younger or you do not have a lot of collateral. Borrowers who might struggle to get a conventional bank loan can often still qualify for an SBA loan.

Benefit 5: Flexible Use of Funds

An SBA 7(a) loan is flexible about how the money is used. Beyond buying the building, you can often use SBA financing for:

- Buying or renovating commercial property

- Purchasing equipment and fixtures

- Working capital for daily operations

- Refinancing certain existing business debt

This flexibility lets you solve more than one need with a single loan.

Benefit 6: You Can Refinance and Grow

An SBA loan is not just for buying. Many owners use one to refinance an existing commercial property loan into a lower rate or a longer term, which can lower payments and improve cash flow.

As your business grows, owning your property also builds equity. Over time, that equity becomes a valuable asset you can use to expand further.

A quick and honest note on prepayment: some SBA real estate loans do carry a prepayment penalty in the early years, especially the SBA 504. It is often a step-down penalty that shrinks each year and then disappears. Always ask about the exact prepayment terms before you sign, so there are no surprises if you sell or refinance early.

Benefit 7: Expert Guidance from Commercial Lending USA

The SBA process has a lot of steps and paperwork, and that is where good guidance saves you time and stress. As a commercial mortgage broker and correspondent, Commercial Lending USA helps you:

- Understand whether a 7(a) or 504 loan fits your goals

- Prepare and organize your application and documents

- Compare offers across our network of SBA lenders

- Work toward the best possible rate and terms for your deal

- Stay supported through closing and beyond

To be clear, Commercial Lending USA is a broker and correspondent, not a direct lender. We do not approve or fund loans ourselves. We connect you with the right lender and manage the process for you. Commercial Lending USA is a member of the American Association of Private Lenders and is BBB accredited.

Can You Use an SBA Loan for an Investment or Rental Property?

This is one of the most common questions, and the answer is important. SBA loans are for owner-occupied commercial property, not passive investment property. To qualify, your own business must occupy at least 51% of the building.

That means you generally cannot use an SBA loan to buy a single-family rental, a duplex, or an apartment building that you simply rent out for investment income. The SBA program exists to help small businesses own the space they operate in, not to finance a rental portfolio.

Here is the simple test:

Situation | SBA Loan? | Better Option |

You run your business from the property (51%+) | Yes, SBA works | SBA 7(a) or 504 |

You buy a building and lease it all to tenants | No | |

You buy a rental or apartment building | No | DSCR loan or bridge loan |

Mixed: you occupy part, lease the rest | Sometimes, if you occupy 51%+ | SBA 7(a) or 504 |

So if your goal is a pure rental or investment property, a DSCR loan is usually the right tool, since it qualifies based on the property's rental income and has no owner-occupancy rule. If you plan to operate your own business from the property, an SBA loan is an excellent fit. Not sure which category you fall into? Commercial Lending USA can look at your plan and point you to the right program.

SBA 7(a) vs SBA 504: A Quick Comparison

Feature | SBA 7(a) | SBA 504 |

Best for | Property plus other business needs | Real estate and big equipment |

Rate type | Often variable | Usually fixed |

Typical 2026 rate | About 9% to 11.5% | About 6.5% to 7.5% |

Down payment | Around 10% to 20% | Around 10% to 20% |

Term (real estate) | Up to 25 years | Up to 25 years |

Flexibility | High | Focused on real estate |

If you only need to buy the building and want a stable fixed rate, the 504 is often the lower-cost choice. If you want flexibility to cover other business needs too, the 7(a) is usually the better fit.

How to Apply for an SBA Loan

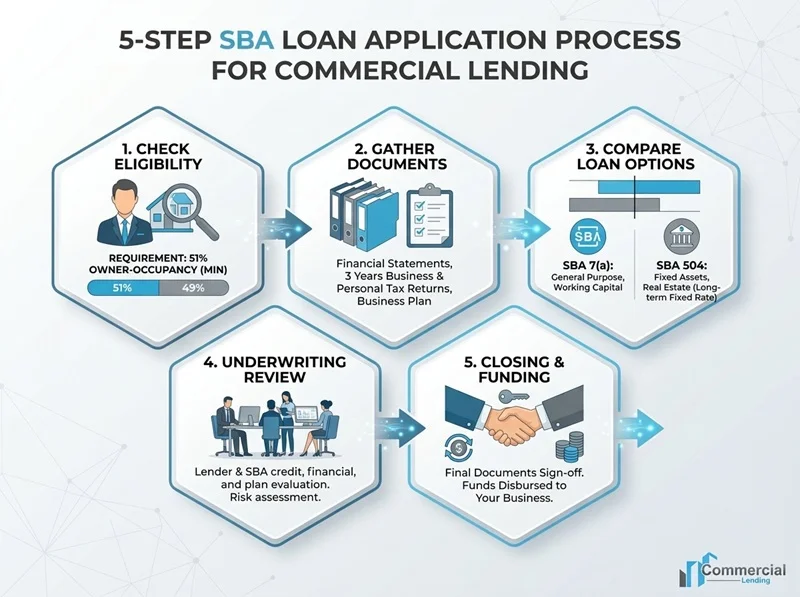

Here is the simple version of the process:

- Check eligibility. Confirm your business is for-profit and will occupy at least 51% of the property.

- Gather documents. Expect to provide tax returns, business financials, a business plan, and details on the property.

- Compare your options. Decide between a 7(a) and a 504, and compare lenders. This is where a broker helps.

- Submit and underwrite. The lender reviews your business, your finances, and the property.

- Close and fund. Once approved, you sign, bring your down payment, and get the loan funds.

SBA loans take longer than hard money, often several weeks, so it helps to start early and keep your paperwork organized.

Ready to Buy Your Commercial Property?

If you are ready to stop renting and own your space, an SBA loan could be the key. Reach out to Commercial Lending USA today for a free consultation. Call (855) 365-9200 or apply online, and we will help you compare your options and move toward approval.

Frequently Asked Questions

What is an SBA loan for commercial property?

It is a government-backed loan that helps small businesses buy or refinance commercial real estate. The SBA guarantees part of the loan so lenders can offer lower down payments and long terms. The two main options are the SBA 7(a) and the SBA 504.

What are SBA loan rates in 2026?

With the prime rate at 6.75%, SBA 7(a) rates for commercial property generally run about 9% to 11.5%, while SBA 504 loans price lower on the real estate portion, often around 6.5% to 7.5% with a fixed rate. Rates change with the market, so confirm a live quote.

How much down payment do I need for an SBA loan?

Usually 10% to 20%, which is lower than the 25% to 30% many conventional commercial loans require. Your exact amount depends on the property and your business.

What credit score do I need?

Most SBA lenders look for a credit score around 680 or higher, along with a solid business plan and the ability to repay. Requirements vary by lender.

What types of property can I buy with an SBA loan?

Owner-occupied commercial properties like office buildings, retail spaces, warehouses, industrial buildings, and mixed-use properties. You must use at least 51% of the property for your own business.

Do SBA loans have prepayment penalties?

Some do, especially the SBA 504, which often has a step-down penalty in the early years. Others may not. Always ask about the exact prepayment terms before you sign.

How long does SBA approval take?

It usually takes several weeks, longer than a hard money loan. Starting early and keeping your documents organized helps speed things up.

Can I refinance an existing commercial loan with an SBA loan?

Often yes. Many owners refinance into an SBA loan to get a lower rate, a longer term, or lower monthly payments.

Is Commercial Lending USA a direct lender?

No. Commercial Lending USA is a commercial mortgage broker and correspondent. We do not approve or fund loans ourselves. We connect you with the right SBA lender and guide you through the process.

How do I get started?

Call (855) 365-9200, email sales@commerciallendingusa.com, or apply online for a free review of your commercial property goals.

Disclaimer: Loan rates, terms, and requirements shown here are based on current programs and market conditions as of 2026 and may change at any time. Rates vary by lender and borrower. All loans are subject to lender approval and underwriting. This article is for general information only and is not financial or legal advice.

0 Comments

Leave A Comment